It is possible that commentators and analysts have been dwelling too much on the challenges faced by TEVA due to the expiration of its patent on Copaxone!

I have recently run across an intriguing investment story – a story that entwines rough and tumble board politics, patent expiration, an extraordinarily focused management team (intent on doing whatever it takes to grow), pharmaceutical creativity, and the inevitable growth of the “Generic” drug space[1]. By way of upfront “disclosure”, I am not fully convinced that it is currently a “five star” trade or investment; however, I am convinced that, as is quite common, the financial press have largely focused (like a laser) upon one glaring issue facing the company in question, while simultaneously ignoring or discounting the numerous other quite positive developments within the business!!

Our focus today is on Teva Pharmaceutical Industries Limited (TEVA)[2] – a company with a heritage that started in1901, but whose current form took shape through a merger in 1976. It is a global pharmaceutical company that ranks as both the world's largest generic manufacturer and its largest manufacturer of active pharmaceutical ingredients. Its headquarters is located in Petah Tikva, Israel (about 7 miles east of Tel Aviv). TEVA sports a market cap in the high-40 billion dollar range, and has a current forward looking yield of approximately 2.3%. Its average daily trading volume is almost 4 million, so it offers good liquidity; and its “Beta” puts it on par with the S&P 500 Index (1.01).[3]

If your only exposure to TEVA is the standard article currently found within the financial press, you might think that TEVA’s future was staked almost entirely upon the fate of its biggest selling drug – Copaxone. However, when one supplements the information in such articles with even a brief review of the long list of pharmaceutical products that TEVA currently markets[4], it will be surprising to learn of the breadth and width of the conditions for which TEVA manufactures and sells drug therapies!

This article will focus first on the two biggest challenges TEVA faces: 1) The expiration of the Copaxone patent; and 2) Recent divisions within the TEVA Boardroom. Then we will shift to several positive developments and trends within TEVA. Finally, we will wrap up by taking a quick look at the company’s financial condition.

CHALLENGES:

COPAXONE PATENT EXPIRATION:

Copaxone has been an efficacious and widely used treatment for relapsing multiple sclerosis (MS) ever since the drug’s launch in 1997. Between 1997 and the present, the drug has been at the very heart of TEVA revenue and earnings engine!

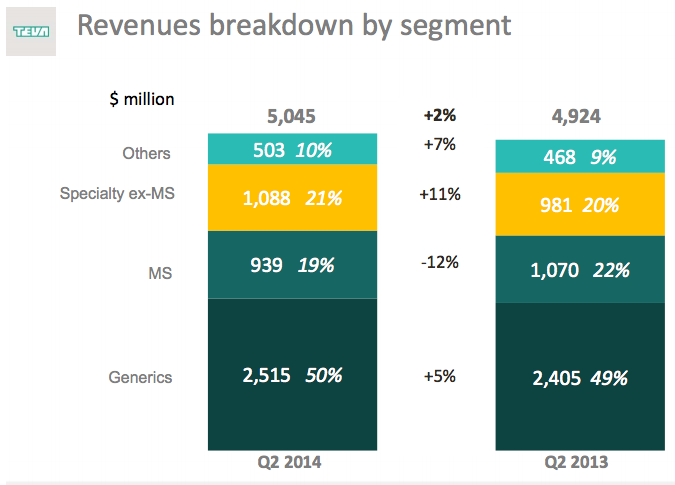

Here is a chart displaying 2Q Revenue by product line in FY 2013 and 2014. You can quickly see how large a revenue-generator Copaxone (MS segment) has been (about 1/5 of total revenue):

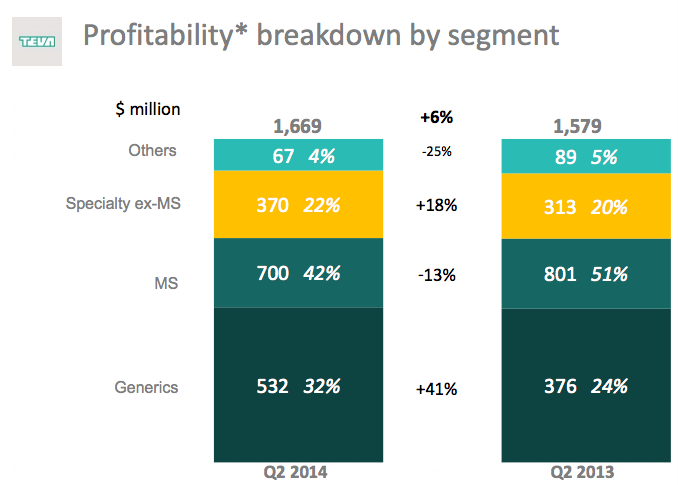

As you’d guess, the drug accounts for an even more sizable slice of profits (currently 42%):

As you’d guess, the drug accounts for an even more sizable slice of profits (currently 42%):

The patent protection on Copaxone expired 3 months ago (May 2014). So the first key insight an investor needs to know about TEVA is that this is “old news” that should already be “priced” into TEVA’s stock.

The second insight regarding the challenge posed by Copaxone’s patent expiration is that the management of TEVA is bound and determined to extend the profitability of its key drug for as long as possible. These efforts have included at least the following:

1) Improving and reformulating the original patented therapy (20 mg dose administered daily) to a 40 mg therapy administered just three times a week. This new version of the drug has patent protection until 2030.

2) Proactively working with existing patients (and their doctors) to convert them from the older therapy to the newest therapy. As you’ll see below, the company has reported a 51% conversion rate thus far, with a goal of 65%.

3) TEVA has initiated a number of legal suits to squash, or at least challenge and delay, efforts by drug firms such as Mylan (MYL), and a partnership between Momenta Pharmaceuticals Inc. (MNTA) and Novartis AG (NVS), to gain approval of and start the marketing of a generic version of Copaxone[5].

a) The most recent news story about these filings (August 28th) prompted investors to sell down TEVA stock by 2%

b) Thus far, two suits by TEVA have received adverse judicial rulings, as did a citizen petition filed with the FDA (on the basis that the existing Copaxone’s efficacy depends heavily upon a proprietary knowledge/formula and treating CNS (Central Nervous System) disorders is too complicated for any FDA approval to proceed without full-fledged clinical trials).

i) In response to the FDA declining the petition, TEVA sued the agency! (It lost the suit.)

c) It is fully expected that TEVA will now sue MYL and the NVS/MNTA combine for patent infringement, which should lead to a 30-month stay of any such generic therapy sales.

i) That would mean that the generic competitors could be put off as long as the beginning of 2017.

ii) Meanwhile, if any generic versions are sold and TEVA ultimately prevails, the producers of said generics would be forced to forfeit profits, and pay up to treble damages. That might (itself) lead to restraint on the part of those competitors, in an attempt to avoid costly risk.

4) TEVA also faces competition from drug companies that will produce oral therapies for the treatment of MS, but there is reason to believe that the injected therapy is more effective.

As one looks ahead to the dramatically more intense challenges now faced by TEVA in selling its MS therapy, it is natural to wonder why a MS patient would not just immediately jump to a less expensive generic drug product as such became available. The answer comes rather easily if one considers what he/she would think if a loved one has been thriving under months or years of the existing Copaxone treatment, and has come to truly appreciate the much more palatable 3-times a week reformulated version of the drug. How likely would you be to want to switch medication?

Here is the applicable slide from a recent TEVA presentation (note especially that even following patent expiry, Capoxone still outsells the 2nd leading therapy by a 2-1 margin):

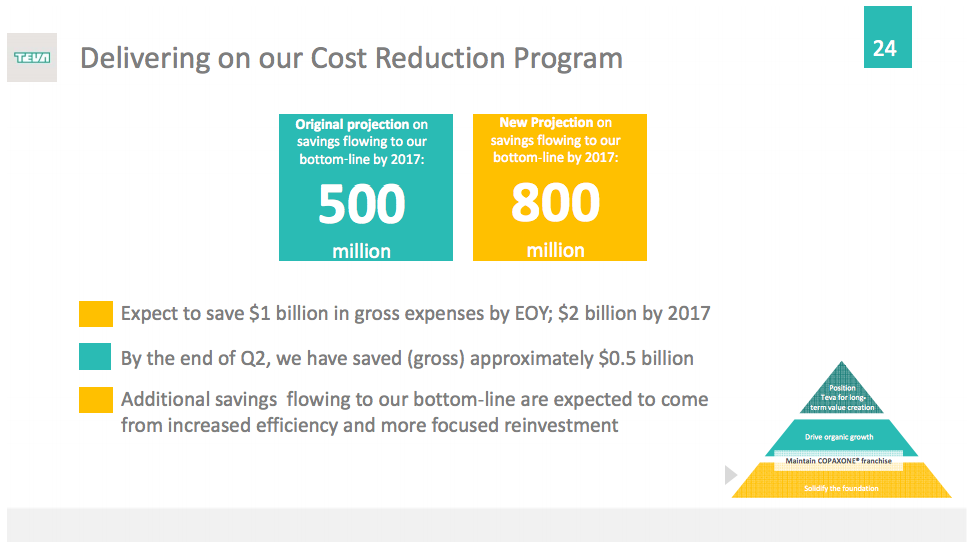

Finally, as TEVA works hard to ensure the maximization of future sales of its Copraxone therapy, it has also announced an effort to reduce costs ($2 billion by 2017):

Let’s move on to the second challenge:

Let’s move on to the second challenge:

BOARDROOM DIVISION:

As has often been the case in corporate history, the recent divisions faced by TEVA were prompted by a death. Famous Israeli industrialist, Eli Hurvitz, who at one point served TEVA as its CEO, was presiding over its board as Chairman when he died in November of 2011. Upon Hurvitz’s death, then vice chair, Dr. Philip Frost, ascended to become the board’s Chair.

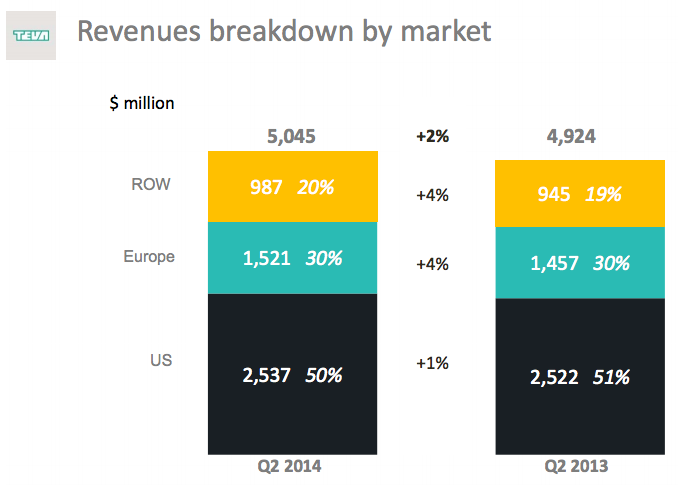

Dr. Frost recognized what any astute observer could not help but realize – namely, that TEVA had matured to the point where it needed to expand its vision and the breadth of its marketing and operations far beyond the existing customer base. Here is a telling slide to that very point… revealing the source of TEVA’s current revenue stream:

A company with the intellectual and brand assets of TEVA holds great potential as a global powerhouse – especially since most current analysts see generic drugs as having a particularly bright future within the so-called Emerging Market countries! In the above slide, “ROW” refers to “Rest of the World”. The reality that only 20% of sales come from beyond Europe and the United States is a metric that one can interpret in one of two ways:

1) The existing management/board has unduly neglected the vast opportunity for sales beyond those two regions; or

2) TEVA has nearly unlimited room for revenue and sales growth if it commits to scaling up and extending its reach to Asia, Central and South America, Australia, and Africa!

With that perspective in mind, Dr. Frost was the leader in bringing pharmaceutical veteran, Jeremy Levin, to TEVA in May of 2012 as CEO.[6] Among other things, Levin thereby brought a global perspective to the management team.

This could be categorized as a corporate decision that was made for the right reasons, but (perhaps) did not have precisely the right persons in place to carry out the vision. What do I mean by that?

A major dimension within TEVA’s path to success has been the ingenuity, discipline, creativity, and indefatigable determination of the Israeli people! Their resourcefulness through the decades has been the most essential element in building TEVA into a $50 billion company! Going hand-in-hand with that heritage have been elements that ensured the company’s historical focus, including: a requirement within the corporate bylaws that the TEVA CEO, its headquarters, and a majority of the directors must reside in Israel.[7]

Into that heritage and setting stepped a Miami, Florida billionaire (Dr. Frost) and a South African (Mr. Levin). Focused on the goal of expanding the vision and horizons of TEVA, Levin unwittingly did such seemingly natural things as hiring foreign executives and terminating partnerships with certain Israeli companies. As one might have expected, a number of board members did not receive such moves enthusiastically!

In defense of both TEVA and Israel, the problem they experienced has been common in other parts of the world. Perhaps a more successful plan would have been to have a long-lived Israeli Chair work with an operational team of two persons (perhaps a CEO and COO) within which one was Israeli and one was an experienced global drug executive.[8]

Following the resignation of Levin, Eyal Desheh was appointed as acting president and CEO. This past January, Erez Vigodman (who is acclaimed as a “turn around specialist”) replaced Mr. Desheh as president and CEO. In addition, it has been announced that Dr. Frost will be stepping down by the end of 2014 as Chair (before his complete term was due to expire). Assuming that the chairman to be elected at that point will be one who is attuned with and supportive of Mr. Vgodman, it is a reasonable assumption that the TEVA board will be able to move ahead with a more single-minded focus (and has hopefully learned a lesson that will prove fruitful for the future!).

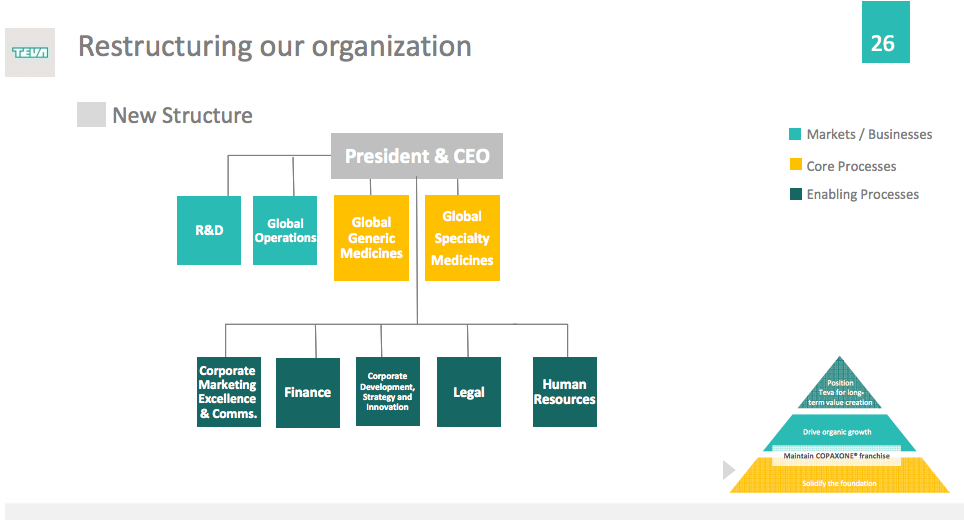

A quite positive indicator that the board is seizing the opportunity to focus upon creating a better, more productive and profitable future, is its recent agreement upon a corporate re-organization, moving from this structure:

- This is the old organizational structure

to a much more streamlined (and likely more efficient and responsive) structure:

- Here is the NEW organizational structure

Now let’s move on to positive trends and opportunities.

POSITIVE TRENDS/OPPORTUNITIES

GENERIC THERAPIES:

Generic drugs do not grab the attention and the headlines that break-through “branded” drugs command. However, the generic business model is more enduring (with less drama). In addition, you may not know that within the U.S., generic manufacturers who are the first to successfully challenge existing drug patents (“first to file”) are granted a 180-day period of “exclusivity” – during which they can market the new generic without coping with the complications of cut throat competition, competitive pricing, etc. In regard to this aspect of the generic drug space, it is germane to highlight the fact that TEVA has more than sixty first-to-file positions within the U.S. – more than any other generic manufacturer!

Quite soon, TEVA will begin production of Detrol[9] (for the treatment of bladder conditions). And by 2017, TEVA has FDA approval to begin production of a generic version of the venerable Viagra. Currently, Pfizer (PFE) owns the expiring patents on both of those drugs.

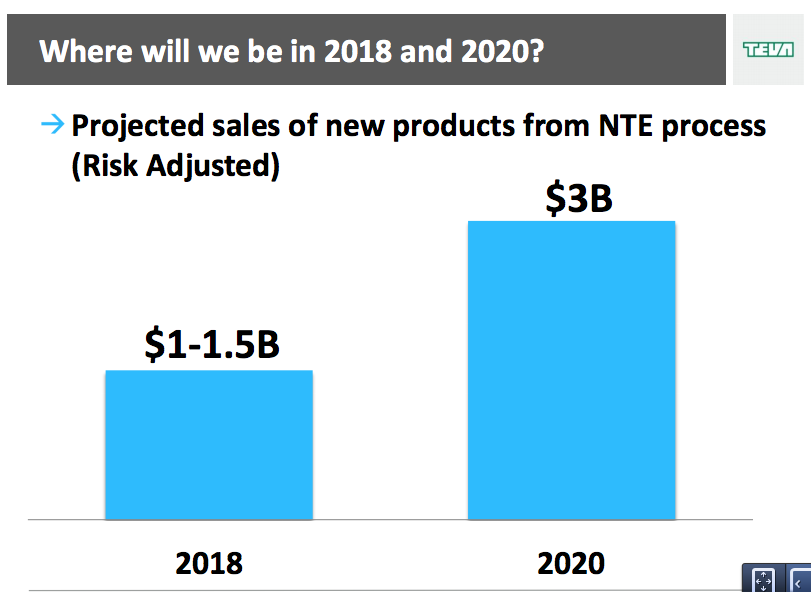

NEW THERAPEUTIC ENTITIES (NTE):

The NTE field involves the development of new formulations… or a combination of older drugs.[10] TEVA’s long history and deep experience with generic drugs, combined with its expertise in developing branded drugs to treat a number of conditions (such as Copaxone) make TEVA an exceptionally promising player within the NTE area! A number of experts project the company’s NTE efforts to become a multi-billion business for TEVA!

As one small example of an NTE, TEVA is quite close to receiving European approval (EC) for DuoRespSpiromax, an inhalable powder designed to treat the bronchoconstriction condition that results from both asthma and COPD (Chronic Obstructive Pulmonary Disease). Existing treatments are considered relatively ineffective and result in “under treatment” of affected patients. Medical authorities estimate the total number of patients impacted by COPD on a yearly basis to be about 30 million suffering from asthma and 23 million dealing with COPD.

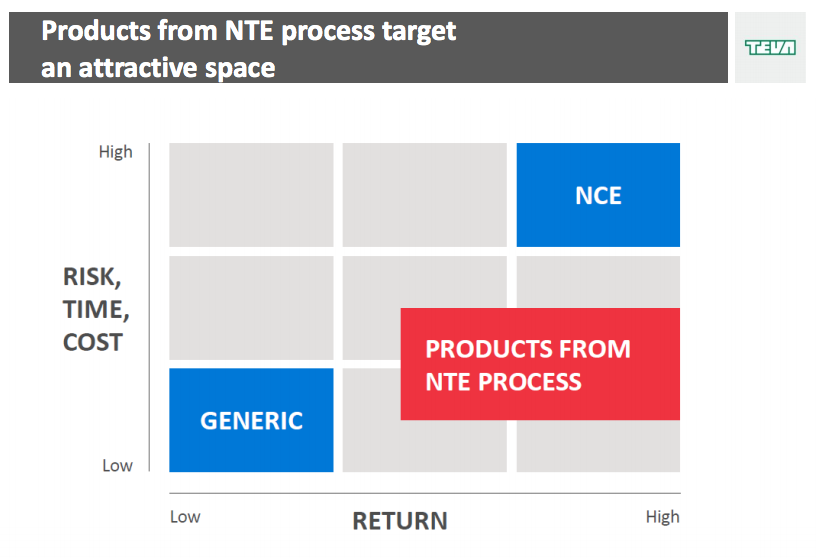

As TEVA pointed out in a recent presentation, the “Risk/Reward” profile of the NTE space is quite favorable:

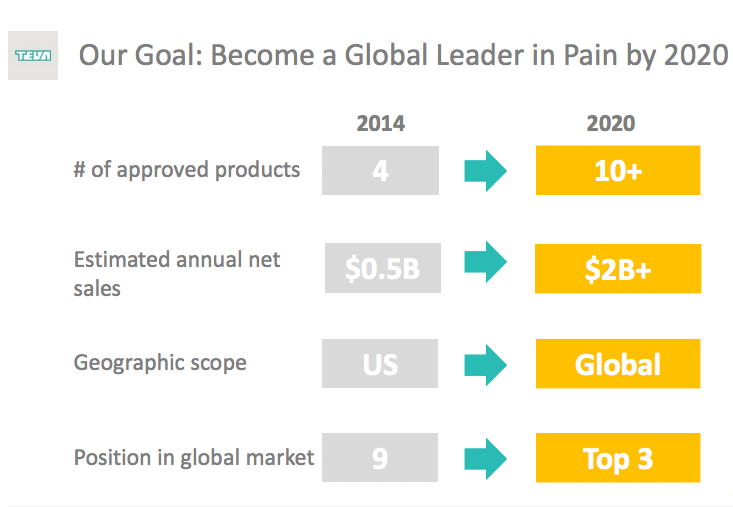

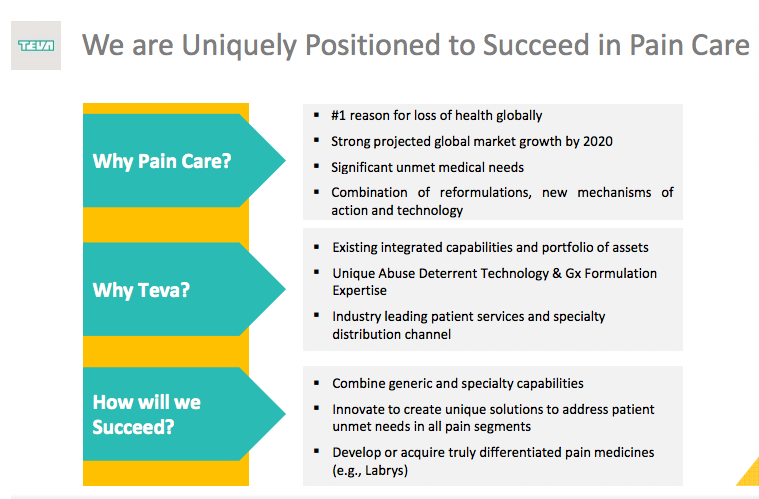

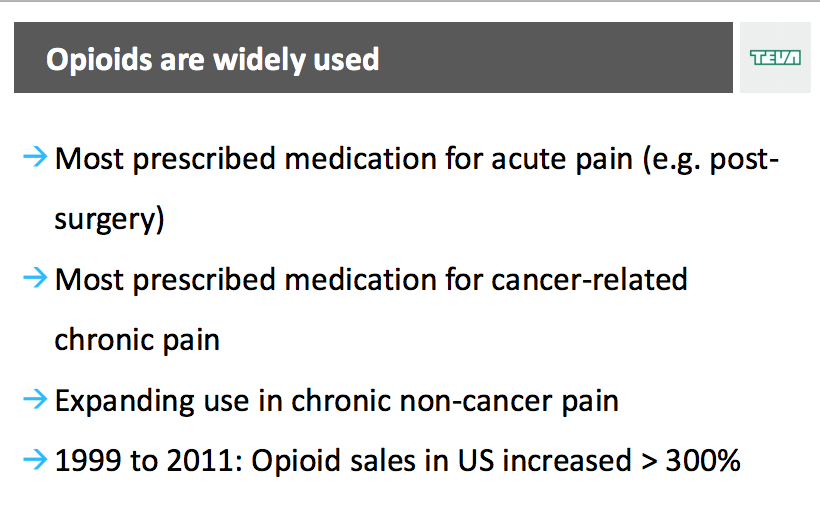

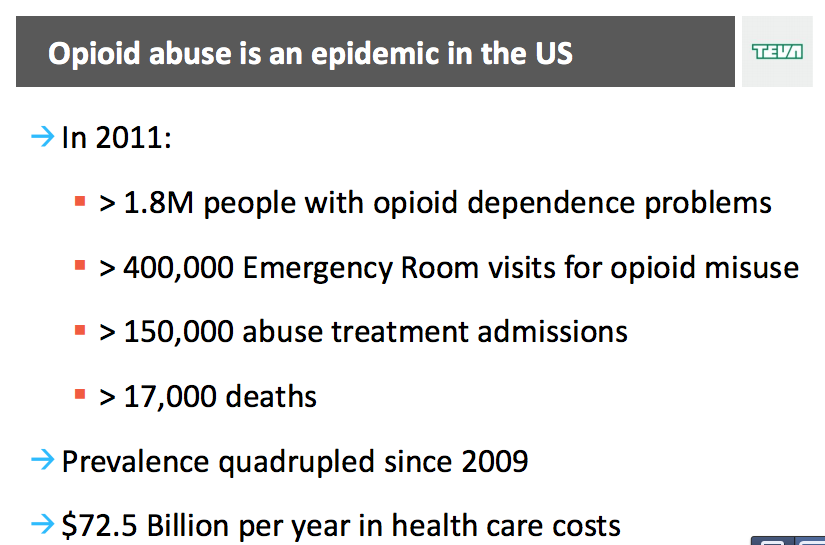

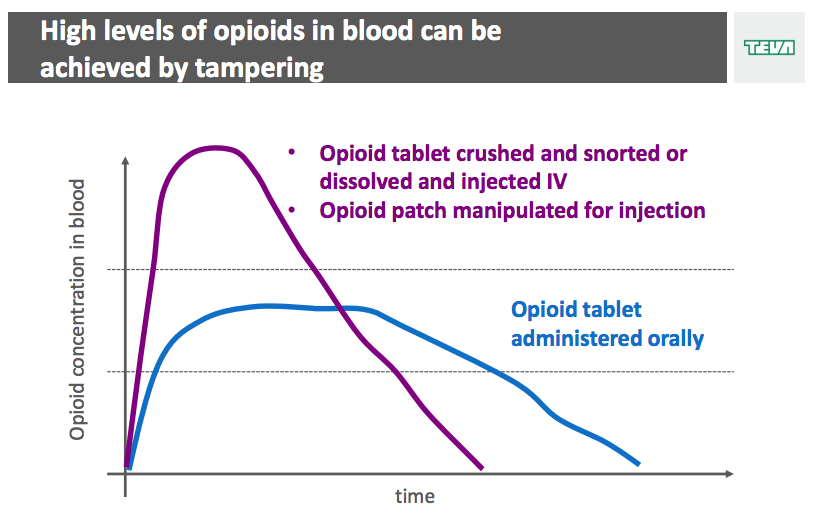

PAIN MANAGEMENT:

A growing emphasis with TEVA is the development of therapies to more effectively manage pain:

A significant part of this budding effort is the recent acquisition by TEVA of NuPathe, Inc. (PATH). TEVA was particularly intent upon securing ownership of NuPathe’s premier drug, Zecurity, which has the distinction of being the sole prescription migraine patch approved by the FDA. Zecurity is a disposable, single-use transdermal patch that delivers the migraine medication through the skin! Even just that one drug alone has now given TEVA a significant competitive advantage within the CNS (Central Nervous System) treatment space vis-à-vis competitors! As a big bonus, TEVA also now controls the proprietary transdermal delivery technology developed by NuPathe. In addition, TEVA now produces/markets the NuPathe therapies for treating Parkinson’s and schizophrenia (also delivered through patches).

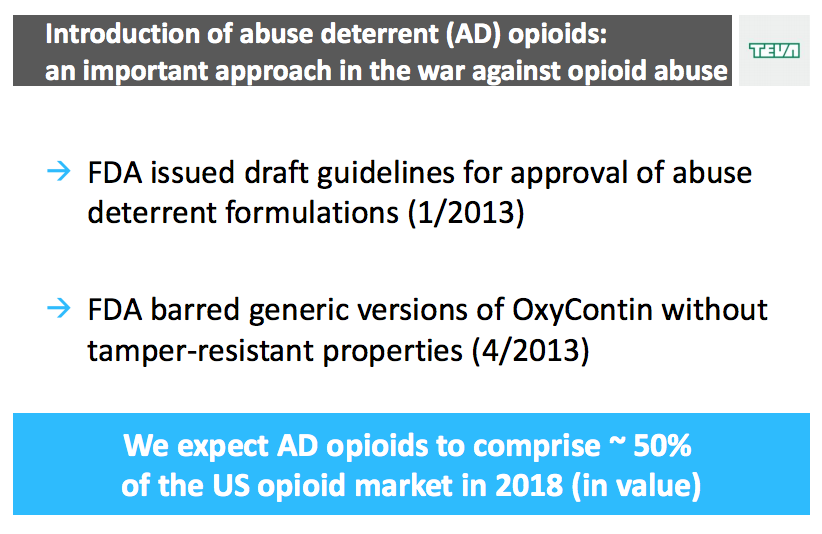

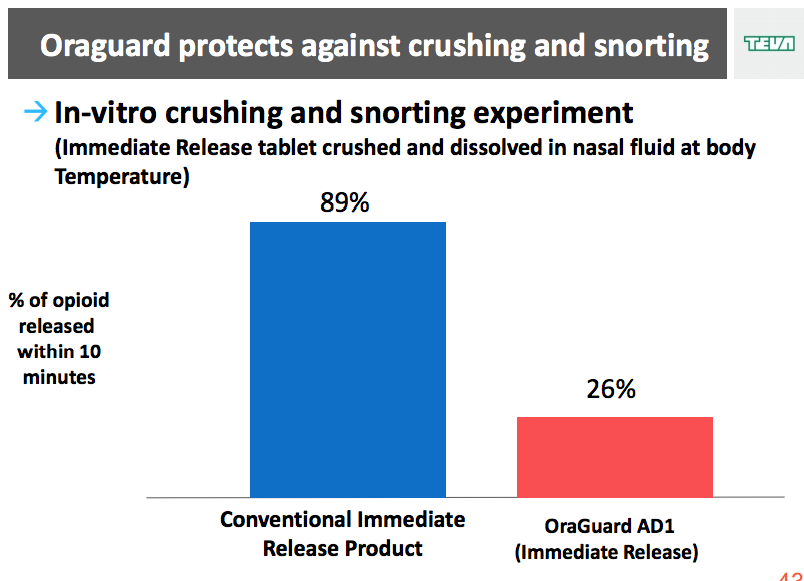

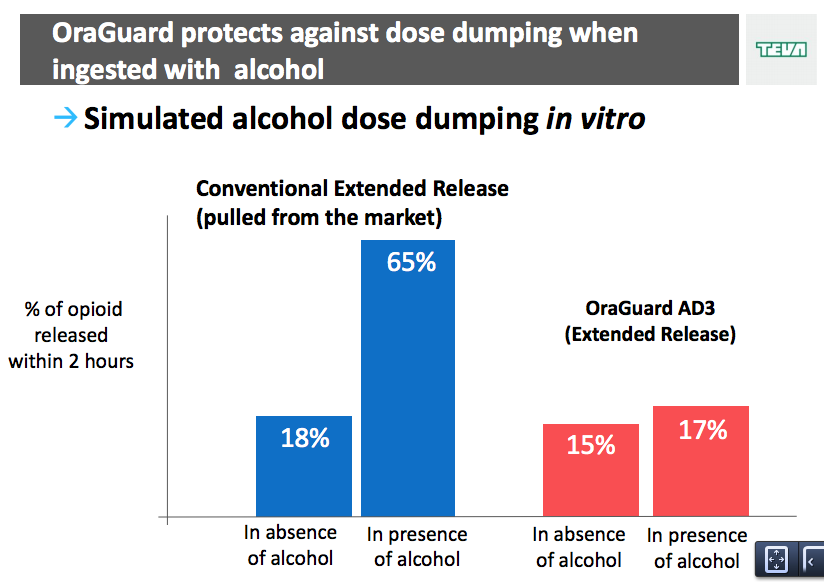

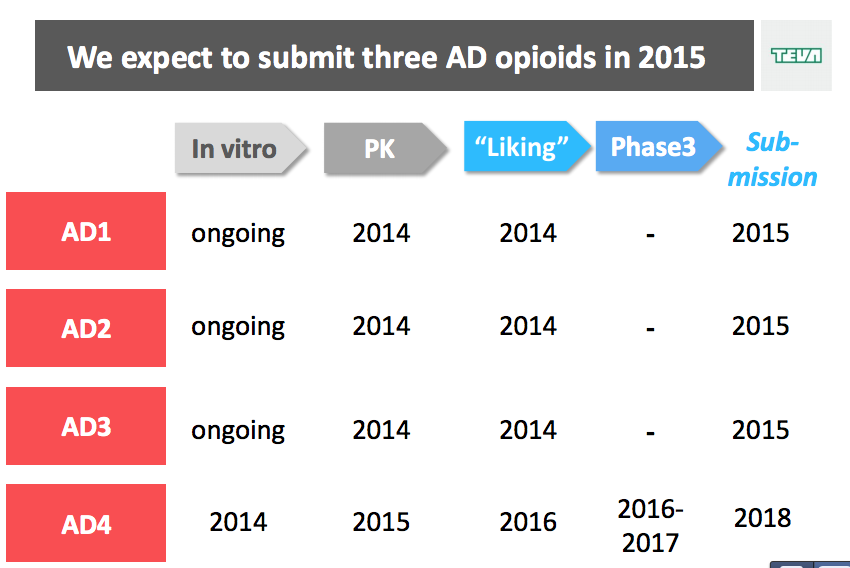

I confess that the next few slides overweight the relative importance of the drug technology involved. However, but these slides eloquently present the intriguing need for opiate based pain management therapies that significantly reduce the risks of abuse (and therefore lowers the risk of loss through theft… as well as the cost to society of the consequences of abuse). The slides also demonstrate that TEVA has the ability to create new, innovative solutions to drug-related issues!

Let’s take a quick look at TEVA’s financials (full FY figures from the 2013 Annual Report):

FINANCIALS

FROM THE INCOME STATEMENT:

Net Revenue 20,314,000

Gross Profit 10,707,000

Op Income 1,649,000

Net Income 1,269,000

FROM THE BALANCE SHEET:

Total Assets 47,508,000

Working Capital 2,493,000

LT Debt 10,387,000

ST Debt 1,804,000

TEVA has been managing to slowly but steadily decrease its debt (and leverage). One analyst points out that, if TEVA was valued at the same Price/Sales Ratio as it was in 2006 … it would sit at a price over $20 higher than the current price. However, even the analyst acknowledges that such a metric is moot because … 8 years ago Copaxon still enjoyed 8 more years of patent protection. Since a stock’s price is a function of “future discounting” (looking forward), that alone would account for the fact that TEVA now sits at a much lower P/S ratio!

When analyzing more mature companies, experts often highlight the Free Cash Flow (FCF)[11] metric. Based on projections for 2014 and 2015 as offered by Value Line… it would appear that TEVA’s FCF could reach as high as (or exceed) $5/share.

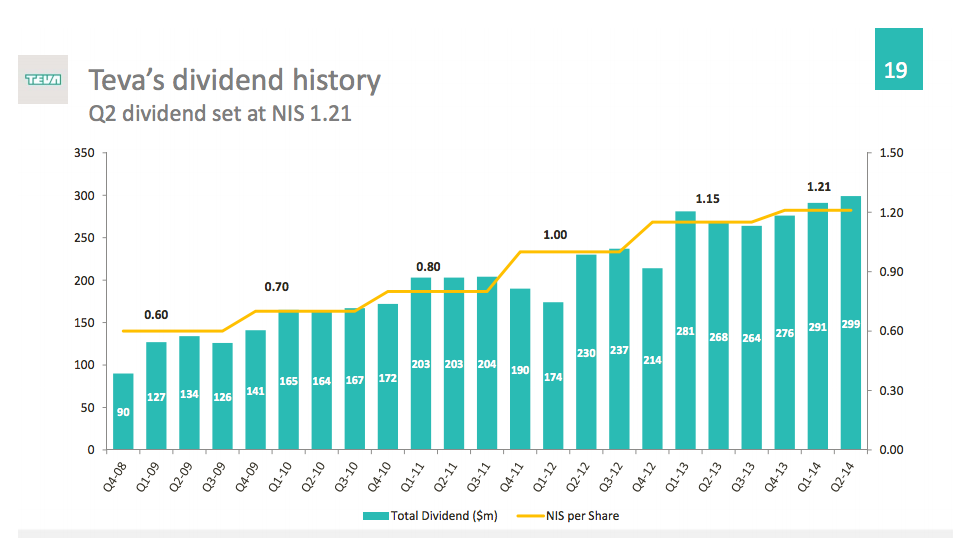

Based on that metric and the current price (at the end of August) of $52.52… TEVA trades at 9.5 times FCF (or at a 10.5% FCF yield). One insight (among many) suggested by this FCF metric is that TEVA’s current dividend can be considered relatively “safe”. In fact, a dividend has been paid since at least the year 2000:

INVESTOR TAKEAWAY:

INVESTOR TAKEAWAY:

No investment is a sure thing, for no one knows what the future brings. However, experts agree that one historically profitable trading strategy is to keep one’s eye out for investment “stories” that have “leaned too far” toward one particular consensus, while ignoring the bigger picture within any given company. An overly hackneyed example comes from the glory days of Apple, Inc. (AAPL), as it approached and exceeded $700/share. The all too common expectation in those days was that AAPL was headed (almost by some “divine right”) to move over $1,000/share. As we know, it moved over $300, but in the other direction!

Based upon TEVA’s story as I have tried to outline it above, perhaps you can see the same thing that I am seeing, namely:

1) TEVA is very intent on fighting to maintain and maximize the future earning power of its reformulated Copaxone therapy.

2) Since that patent has already expired (in May), the negatives related to that expiry should already be priced into the stock.

3) It is likely that the TEVA board has moved beyond the differences that beset it between 2011 and late 2013. Their recently unveiled reorganization plan and their rigorous cost-cutting effort both suggest as much.

4) The Generic Drug business is not glamorous or headline worthy, but it is the wave of the future (everyone reviewing current health plan coverage and exclusions, as well as prescription drug formularies will confirm that fact!). TEVA is the world-class player in the Generic Market.

5) It is quite likely that TEVA’s vast experience and its proven store of IP will enable it to be a major player in the NTE space – projected to become a multi-billion sales engine.

6) TEVA’s growing focus upon CNS therapies and pain management are both intriguing and promising efforts!

7) TEVA is financially sound, and delivers a solid, seemingly secure dividend with a (current) 2.3% yield. Even more impressively, on a FCF basis, it is yielding over 10%. That is a much higher yield than available (for example) through the U.S. Treasury or “non-junk” corporate bonds!

To summarize, assuming the observations above are correct, there is a case to be made that TEVA is worth consideration as an investment. Not incidentally, it has also proven to be an intriguing stock to “watch”! We’ll just have to see how much “fruit” TEVA’s current efforts bear in the months ahead, as well as keep an eye on the growth of TEVA sales in the burgeoning Emerging Markets!

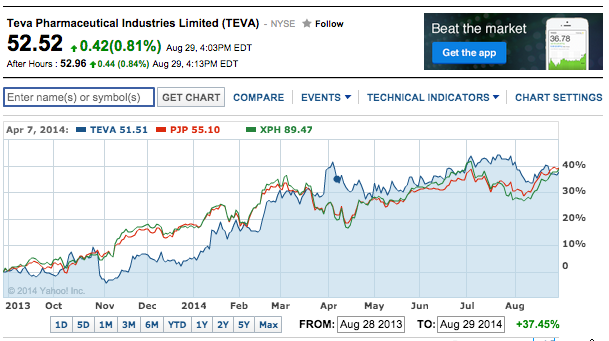

One final thought: It is noted in a number of articles on TEVA that it has been on a tear since last February (after a long period of relative dormancy). That is true. However, if you compare TEVA during the most recent 1-year period with the two largest pharmaceutical ETFs (Dynamic Pharmaceuticals (PJP) and SPDR S&P Pharmaceuticals ETF (XPH)), TEVA has not been “out-of-line” within its investment space![12]

DISCLOSURE:

The author currently shares and options in TEVA. Nothing in this article is intended as a recommendation to buy or sell anything. Always consult with your financial advisor regarding changes in your portfolio – either subtractions or additions.

FOOTNOTES

[1] Obviously, the story also incorporates a country much in the news these days (Israel) since that I where the company headquarters is located.

[2] In the Hebrew language, the word “Teva” means “nature”

[3] As is commonly disclosed, while “past performance is no assurance of future results”, during the period between the early 1990’s and today, TEVA has provided a total return between 21 and 22%. I post this metric because in recent years, the stock has been stuck in a relatively narrow range, at least until late February of this year when it moved up from $44/share to over $54/share.

[4] Easily found in the “PROFILE” section of the TEVA entry within YahooFinance.com

[5] Those firms have filed an ANAD (Abbreviated New Drug Application) for approval of said generic versions.

[6] Prior to TEVA, Levin’s resume included serving as a physician at a hospital in London and working at Bristol Myers Squibb (BMY) and Novartis (NVS).

[7] Of the current 15 directors, 11 of them live in Israel.

[8] In 2011, Deutsche Bank AG announced Anshu Jain (born in India) as CEO… but simultaneously named a German as co-CEO! In a similar vein, Takeda Pharmaceutical took a significant risk (in the context of the notoriously insular environment of corporate Japan) when it hired Cristophe Weber (a French national) as CEO.

[9] The existing patented Detrol brings in over $570 million of annual sales.

[10] Honest to goodness, folks, here is a real example I found in one TEVA article of a “combination drug” form of NTE: combining an antipsychotic with a weight-loss drug.

[11] One simple definition of FCF is: subtract just capital pending from “cash flow”, instead of subtracting both dividends and capital spending.

[12] One additional parenthetical caution, if you don’t mind. I receive a rash of emails each day from investment gurus who offer up a few paragraphs about why this or that company is a compelling “buy”. I find some of them credible. However, one gentleman recently wrote about TEVA: “patent expiration will never be an issue that weighs on its margins.” Enough said.

Related Posts

Is DocuSign an Undervalued Growth Stock to Buy?

Is DocuSign an Undervalued Growth Stock to Buy?

Also on Market Tamer…

Follow Us on Facebook