The Venetian Macao Hotel/Casino Resort in China is reputed to be the biggest casino in Macau.

In Part I we offered details, through text, graphs, and images, of the dynamics that led to the amazing bull market in Chinese equities between October of last year and the most recent market top on June 12th. The upward move was so steady and so powerful that anyone fully invested (and margined) during that period could very easily have felt that they were on an amazing “hot streak” during an extended stay at the Venetian Macao Hotel/Resort in Macau, China (the “Las Vegas of China”).[1]

Of course, one huge difference between Macau and the equity exchanges located at Sanghai and Shenzhen is that when you put your money in the latter, you can officially borrow state managed “margin” in order to leverage your stock ownership! In Part I, we described the official Chinese margin policy and regulations in some detail.[2]

It is clear that the easy availability of margin for Chinese investors played a significant role in accelerating the powerful upward move in Chinese equity values. So let’s combine the 9 months of stock price data I compiled for Part I with a sample (fictional) case study of how China’s margin rules impacted the Chinese markets!

In particular, remember that the Chinese Guarantee Ratio (a metric gauging margin “coverage” in an account) is expected to be 180% or higher. If it slips below 150%, a margin call was to be issued; and if it slips below 130%, the account was expected to be liquidated. (Note: for ease of math, I will use U.S. Dollar amounts; obviously, Chinese investor accounts are denominated in the Yuan)

1) Since the average Chinese margin loan is 6 months in duration… and an investor must repay a margin loan in full before opening a new one, let’s assume that on 12/30/14, Investor Hwei-ru[3] placed $4,450 in a margin account and added $5,550 of margin – for a total account size of $10,000.

2) Based upon price movement of ASHR, Hwei-ru’s portfolio would be worth $14,798 on June 12th!

3) Assuming Hwei-ru chose not to increase her margin balance between January 1st and June 12th, she would have been well “covered” (margin-wise) at a “Guarantee Ratio” of 267%!!

a) After the portfolio tumbles to $9,090.67 on July 8th… her ratio would still be above the “margin call level” (150%) – sitting at 164%!!

4) However, if Hwei-ru took advantage of account appreciation to increase her margin balance (as of 6/12) to $9,550…. her Guarantee Ratio on 6/12 would only be 155% — perilously close to an initial margin call.

a) Alas, by July 8th, her most recent positions would have been liquidated to restore her Guarantee Ratio above 150%!!

b) The reason for this is that her $9,090 balance (at the middle of that second week of July) would move her Guarantee Ratio below 100% … to just 95.2%!!!

As you have likely seen by now, the margin regulations created by Beijing were destined from the start to become quite troublesome to these Chinese investors … for at least these reasons:

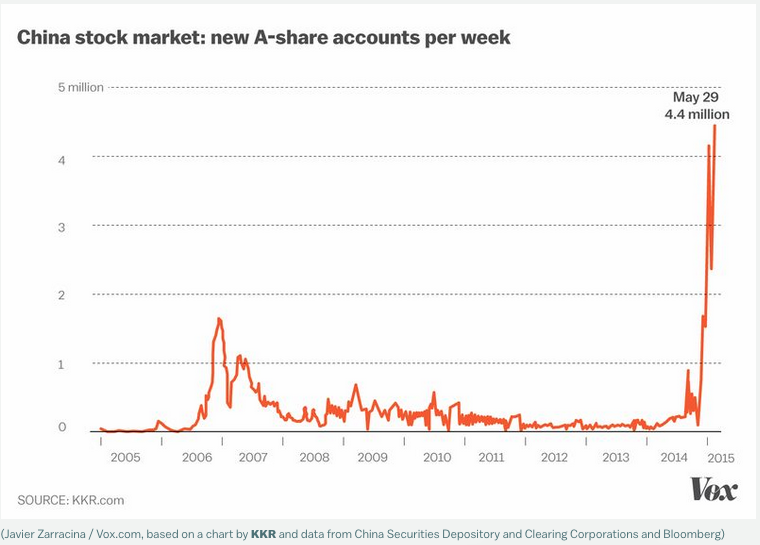

1) The vast surge in new accounts and margin loans skewed the market upward;

Note the parabolic increase in the creation of A-Share accounts during the last months of 2014 and into the first five months of 2015!

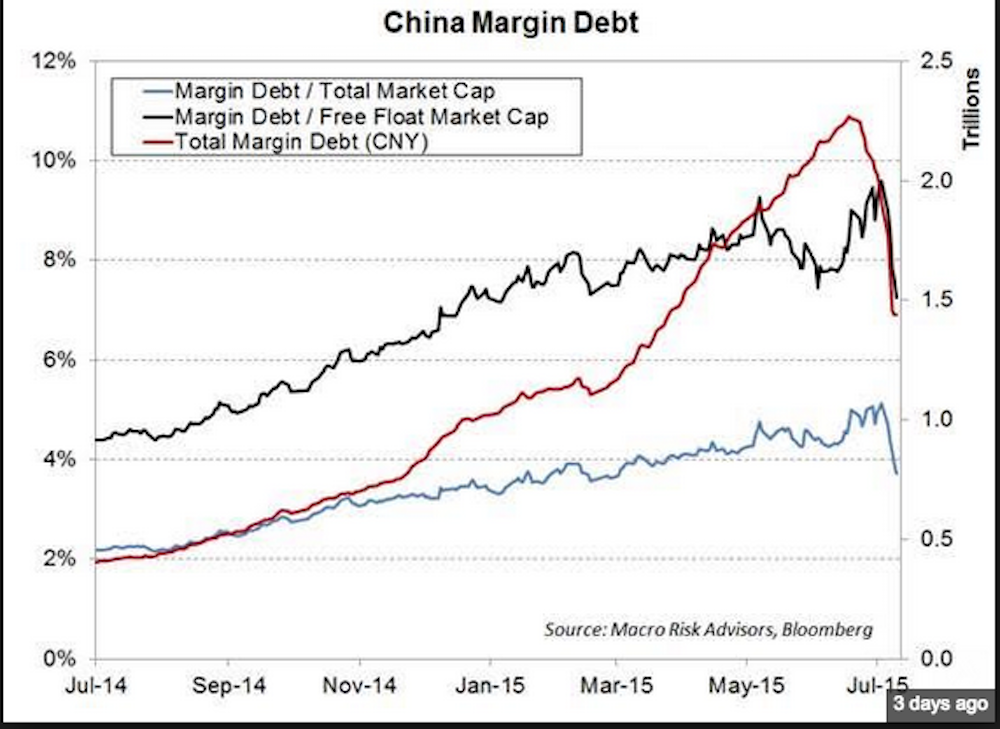

2) $200 billion yuan of margin loans were initiated at end of December 2014 (beginning of January 2015) – meaning that a huge wave of margin debt was going to “come due” toward the end of June – just as the market was tumbling downward;

As this graph illustrates, the rapid rise of Margin Debt levels (with maturity terms of just six months) complicated stock market dynamics in China as prices were declining at the same time that much debt was coming due for payment!

3) In fact, in just 4 days during late June, margin debt shrank by 85 million yuan!

4) The average Chinese investor trades frequently – leading to a very high portfolio turnover rate. The average holding period for a stock is just 15 days. Consequently, any new position purchased around the time of the June 12th market top would be in very deep trouble by the end of June.

At this point, let’s assess the situation in China as it stood in mid-June:

1) The effort by Beijing to encourage Chinese citizens to invest in equities was a stunning success (as we have witnessed through both words and graphs in Part I).

2) The government’s objective to de-lever corporations (through increased equity) and reduce municipal debt (through increased tax revenue resulting from higher taxpayer income) was a success.

3) These efforts also drew global capital to China and put China’s expanding exchanges “on the map”.

So who benefited most from this new “bull market” in China (from October through mid-June):

1) Politicians – their policies from the Third Plenum were basking in success;

2) State owned companies secured higher equity, which replaced government-guaranteed debt – a “win-win” for the government.[4]

3) “The little guy” in China was beginning to feel a part of the “wealth boom” there! Imagine what it must have felt like for Hwei-ru to watch her account move up nearly 50% in less than six months!

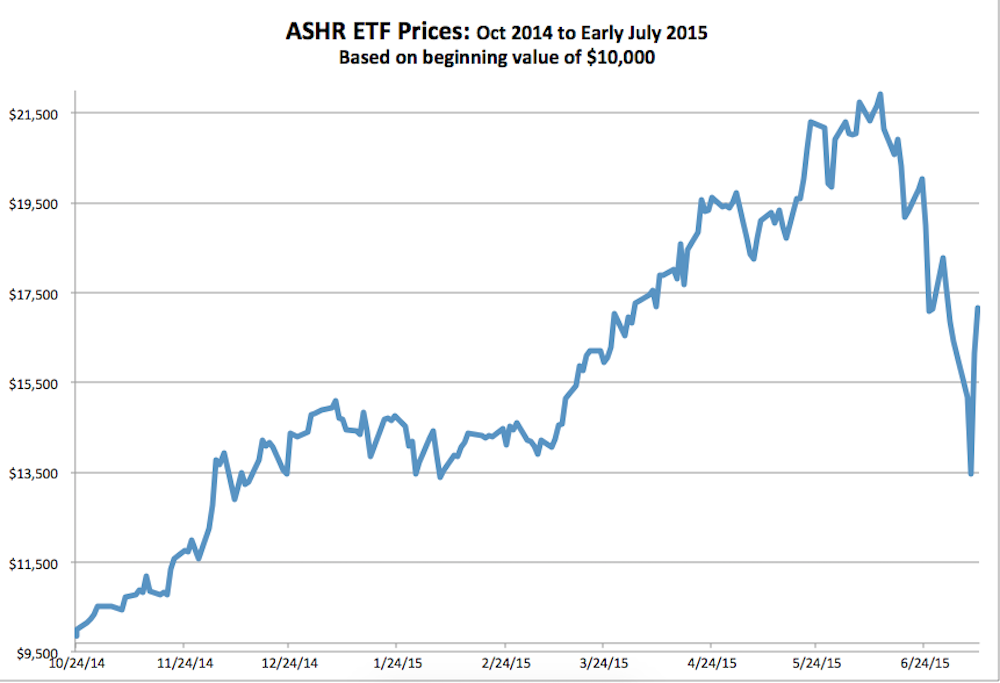

However, if Beijing leaders were basking in their glory on June 12th – they found themselves scurrying for their politic lives from then on. Look at this graph of ASHR from June 10th to July 8th, during which it tanked 39% from the June 12th high:

This graph of ASHR between June 10 and July 8th does not adequately demonstrate just how scary the stock price collapse really was.

Perhaps this graph from my ASHR ETF daily price worksheet offers a more compelling view:

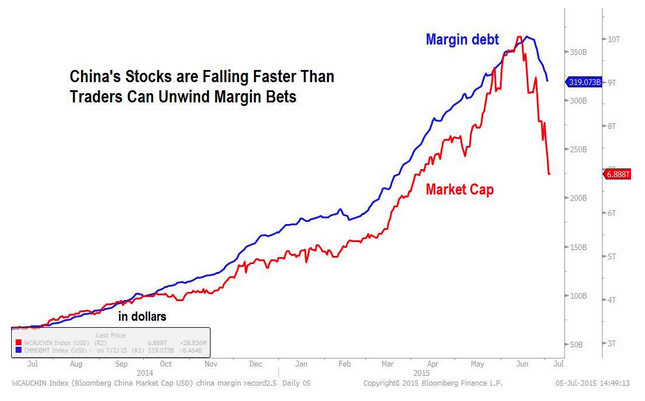

Severely compounding matters, Chinese stock prices were accelerating to the downside faster than investors could offload margin debt — a pattern that sharply steepened downward pressure on prices:

Understandably, the panic that was spreading within the investing public became very much a panic shared by Xi Jinping and his Party colleagues in Beijing. In their panic they began initiating a steady stream of government-imposed actions … until a clear pause (and hopeful halt) in the panic could be objectively verified! Those actions included at least the following:

1) The Peoples Bank of China (PBC) initiated a surprise cut in interest rates at the end of June;

2) Margin rules were “relaxed” – with the government indicating that margin loans did not really need to be paid in full before securing a new margin loan;

a) Margined traders were even given permission to respond to a broker’s margin call by pledging any/all of their ownership in the countless empty apartment buildings scattered throughout the newly built urban areas we described in Part I (aka “ghost cities”).

This is a photo of largely empty apartment buildings in the "Ghost City" of Ordos.

b) Ultimately, before the end of the month, Beijing instructed brokerage firms that they were not obligated to liquidate margin accounts that dropped below the 130% “Guarantee Ratio”.

c) Of course, Chinese regulators regularly announced during market hours that margin financing was “safe”.

3) IPO’s were put on hold;

Here is a beleaguered spokesman from the China Securities Regulatory Commission announcing the "hold" placed on upcoming IPO's.

4) The Chinese version of U.S. stock exchange “circuit-breakers” went into effect – a 10% limit on the movement of stock prices.

5) Although (to my knowledge) not initiated by Beijing, on July 6th and 7th a stampede developed of companies requesting a halt to trading in their shares. Approximately one-fourth of Shanghai and Shenzhen-listed companies made that request on the 6th, and (reportedly) another 200 companies on the 7th! (You can’t sell down the price of stocks if they aren’t trading.) This graphic shows the status on the 8th.

6) Beijing forbade “short-selling”! By July, Beijing politicians had become extremely perturbed by this crisis – a cascade of selling pressure that removed (by some reports) as much as $4 trillion from the aggregate market cap of Chinese-listed stocks. A report by the (state-run) Xinhau News Agency revealed that Chinese police had actually visited the China Securities Regulatory Commission to more closely scrutinize “malicious short selling”.

Here is a photo from the press relations room of the China Securities Regulatory Commission. That agency has been a stressful one to work within during the past couple of months!

One other report indicated that company executives who had sold company shares within the prior 6 months were actually ordered to buy them back.

7) Beijing directed state-run institutions to maintain or add to domestic equity positions:

a) It was reported that the Chinese sovereign fund, Huijin, was buying A-share exchange-traded funds to prop up the market.

b) The Ministry of Finance reported that China’s $500 billion pension fund would start investing in the Chinese stock market;

8) Beijing exercised its influence to secure the support of 21 brokerage firms to purchase at least $19 billion in Chinese stocks – backed up (of course) by a state operated margin finance company that was given direct access to central bank funding!

a) Ironically (or tragically) Beijing found at one point that even these herculean efforts weren’t entirely effective. One embattled, embittered Chinese investor from Hangzhou (who only offered his first name) was quoted in the media as having bluntly observed:

“Where is the promised 120 billion yuan? It's all going to blue chips. Don't they know that retail investors are all trapped in the small caps? My stocks opened up 10 percent but closed down the (10 percent) limit!”

9) One might assume that, in direct response to that very on target criticism from the Hangzhou investor, Beijing announced on July 8 that the China Securities Finance Corp. (a margin financing unit within the China Securities Regulatory Commission) would step into the small-cap space and start buying shares!

10) Big insurance companies also “stepped up”:

a) China Life Insurance Co. Ltd. purchased index funds worth 10 billion yuan.

b) China Pacific Insurance Group and a few other firms invested 1 billion yuan.

11) In my opinion, the “crème de la crème” of this multi-faceted government effort to halt the “Stock Crash” in its tracks came not long after the government announced it was buying small cap shares! Beijing actually tried its hand in shaping the national “Attitude” by directing all state media outlets across the nation to announce:

“Rainbows always appear after it rains!”[5]

Of course, all of these headline-grabbing developments have placed great emotional and financial stress upon literally millions of Chinese citizens. There is no doubt that it has done significant harm to the economy. As just one small example, here is an uncharacteristically blunt observation from the secretary-general of the China Passenger Car Association, Cui Dongshu:

“The plunging stock market is essentially a meat grinder, shredding money meant for buying cars.”

With billions of China’s financial resources being consumed to prop up the market, with investor confidence shaken (if not demoralized), with consumer demand that had been building during the first six months of the year now re-directed (at least for the moment)… what is likely to come from all of this?

Well, to be blunt – there is literally no one who can assure us that she/he really knows how the Chinese stock markets and the Chinese economy will perform during the next several years!!

However, I regret to inform you (and warn you) that the utter impossibility of actually “knowing” what will transpire during the next few years will in no way curb the efforts of countless self-declared “experts” who will surely purport to set you straight with regard to “what is”… and “what will be” in China!

A case in point is the chief China equity strategist for the internationally renowned financial behemoth, Goldman Sachs (GS) – Kinger Lau[6].

This is Kinger Lau, the chief China equity strategist for Goldman Sachs.

By the end of the first full week of July, Bloomberg published this seemingly declarative announcement:

“China’s biggest stock-market rout since 1992 has done nothing to erode the bullish outlook of Goldman Sachs Group Inc. … Kinger Lau, the bank’s China strategist in Hong Kong, predicts the large-cap CSI 300 Index will rally 27 percent from Tuesday’s close over the next 12 months as government support measures boost investor confidence and monetary easing spurs economic growth. Leveraged positions aren’t big enough to trigger a market collapse, Lau says, and valuations have room to climb.”

Perhaps not as informative, but absolutely much more revealing, is what Mr. Lau went on to declare:

[Referring to the Chinese stock market, Lau said:] “It’s not in a bubble yet.”

[If you are just now picking yourself up from the floor and you wonder why the Chinese market is not in a bubble… Lau suggested it is because:] “China’s government has a lot of tools to support the market.”

With all due respect to Mr. Lau, and with all due respect to the London School of Economics, I feel the need to quickly interject an alternative view from an assistant professor of finance at the Warwick Business School (in the U.K.), Lei Mao. Professor Mao has quite appropriately pointed out that “free markets” are not “free” when they are so massively supported (ie. distorted) by the regulations, actions, and financial resources of a central government. Because of the actions of Beijing recounted in detail above, Mr. Lao expresses strong concern that the normal mechanisms that guide the standard world-class stock exchange have been radically disrupted – thereby transforming (overriding) the normal and functional allocation of funds (and trading behavior) upon which healthy markets depend!!

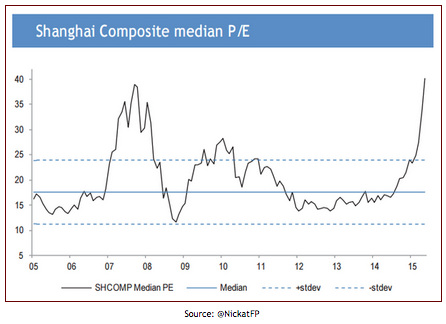

If you combine those concerns with stark charts such as this one regarding relative valuation (by the way, even Mr. Lau concedes that Chinese small-cap stocks “may be overvalued”):

Many experts suggest that Chinese stocks in June moved to "overvalued" status based on fundamental measures such as Price/Earnings Ratios.

Is it any wonder that Mr. Lao is quoted as opining:

“Even an optimistic investor should not participate in the market for now.”

Let me leave you with this worrisome thought:

We’ve already noted that the government of Xi Jinping must have felt a “rush of success” during the first five and one-half months of this year! The most exciting and visible of Jinping’s reforms from the “Third Plenum”[7] was a resounding success – already showing impressive results and bearing truly “juicy” fruit!

However, as the markets began to become “unwound” after June 12th, it seems as though the leaders in Beijing began to become “unwound” themselves! You’ve already read through the countless actions taken by Beijing to “reverse the tide”. Many of those actions conjured up images from the Cold War era governments of Mao Tse Tung and the old U.S.S.R. (especially the KGB)[8].

Why is Beijing hell bent on “solving” this market crisis? The explanation is that the very credibility of Beijing leaders (especial Jinping) is at stake. I believe that web journalist, Gwynn Guilford, expressed the political reality quite clearly:

Gwynn Gilford of Quartz...

“By urging households to buy stocks, Xi has put his credibility — as well as that of the Communist Party — on the line. The stimulus measures’ failure may incite outrage among those very mom-and-pop investors who have lost everything. Though it’s impossible to tell what might ignite it, mass social unrest in China would shake the entire world.”

No one can know what will become of Xi Jinping and his colleagues, just as no one can confidently predict what the markets will do going forward. However, the developments of the past month have surely not improved Jinping’s standing among his peers… nor have they endeared him to the millions of “little” investors in China.

Here is just one small example of what might be described as political foolishness:

Within a much-anticipated economic statement issued just before the markets opened for trading on July 7th, Xi Jinping did not even allude to the (then) three week long tumble in stock prices! Every reporter and every investor had their eyes peeled to read what he wrote… and all were shocked to find nothing about that upon which everyone was most focused and most concerned! Instead, all Jinping said was that he had confidence that China had the ability to deal with challenges faced by its economy.

That strikes me as a Chinese variation on the old fable: “The Emperor Who Had No Clothes”. I am sure that many politicians would strongly defend Jinping regarding his choice not to speak about the stock crisis directly (thereby not implying that he is at all responsible for it happening, nor that he is responsible to fix it.) However, to the average citizen/investor, it must have felt as though Jinping was very “out of touch”.

Of course, in addition to opinion being shaped within China regarding Jinping and his leadership … opinions have certainly been taking shape about him within the larger global setting. Among economists, financiers, and international investors, strong doubts must certainly have taken hold by now with regard to the willingness of Beijing to actually carry out true market “liberalization” – which (as we have noted) is a strategic necessity within its much larger objective of world class economic reform.

INVESTOR TAKEAWAY:

No one can or should try to detract from the economic “phenomenon” that is the People’s Republic of China (PRC). Through hard work, discipline, effective international deal making, sound stewardship of global trade surpluses accumulated through the decades, etc. the PRC has positioned itself as a global economic giant – second only to the United States. There is also no denying that China has served the global economy for many years as an economic “engine” – particularly during these years of substandard economic results within the U.S. and Europe!

However, all of that being affirmed and appreciated, I hope this article has (in helpful ways) made you quite aware of the challenges that face the people of the PRC as they move into the future.

With abject apologies for sinfully oversimplifying these challenges, allow me to highlight these:

1) China is moving through a very difficult transition … from a primarily manufacturing-based economy toward a much more highly developed consumer economy. That transition will continue to be a great challenge in the years ahead – particularly in a nation as gigantic geographically and demographically as China

2) In contrast to its nearby “sister” in sheer size, the PRC will face some “aging” issues similar to Japan and the U.S. in the years ahead:

and those demographic trends hold the potential to impact future GDP growth:

3) The regulatory and accounting environment within the PRC is not as clearly defined and consistent as it is within the U.S. Therefore, depending upon the accuracy of financial metrics, earnings reports, and audited financial statements from Chinese firms can be tricky.

4) There is no doubt that the PRC has made strides toward a more open, more market-dependent economy. However, if anyone has read this two-part article and actually still believes that the two mainland Chinese stock exchanges are free from government control – then I should be taken out back and shot for my utter failure in clearly presenting the facts as they are. Only time will tell how “free and open” (much less “transparent”) the Chinese markets and economy will become in the years ahead.

So let me affirm the suggestion from Professor Mao (from Warwick) regarding trading Chinese stocks:

“Even an optimistic investor should not participate in the market for now.”

Now to be honest, I do not really intend to tell you that you should not trade Chinese stocks. However, what I am telling you is that you should be aware of the risks inherent in the Chinese markets before you invest even one dime in it!! Review the volatility that has characterized these markets during the past 9 months! Take careful note of how heavily “margined” Chinese equities have become. Never forget how quickly the government threw out almost all the previous “rules” that guided the daily operation of these markets in order to achieve the result the government wanted (and also needed)!

In my humble opinion, the Chinese markets have functioned – from last October through today (July 16) — much more like Macau casinos (“the Las Vegas of China”) than the NYSE or the NASDAQ in this country.

However, even with all of this said, I know many traders will want to explore investment options within the PRC – so with that understanding, the next article will highlight several different ETFs that focus upon companies within the mainland.

DISCLOSURE:

The author does not currently own ASHR or FXI… or any other Chinese stock (although he has in the past). Nothing in this article is intended as a recommendation to buy or sell anything. Always consult with your financial advisor regarding changes in your portfolio – either subtractions or additions.

FOOTNOTES:

[1] There is an excellent reason that the Venetian Macao looks like Las Vegas. It is owned by the Las Vegas Sands (LVS)

[2] It is important that you be sure to have read Part – especially that section on Margin!

[3] The name means “wise, intelligent” – a great choice for an investor in China

[4] Never forget that whatever benefits state-owned companies in China also benefits the Communist Party!

[5] An amusing thought: If anyone started to call that statement into question, I wonder if Beijing might gather some key famed scientists to jointly announce that “The ‘Science’ proves that the government’s statement is correct!”

[6] Mr. Lau is a graduate of the London School of Economics, is a U.S.-certified public accountant, and is a CFA charterholder. ![]()

[7] “We must deepen economic system reform by centering on the decisive role of the market in allocating resources….”

[8] With visions of Hitler’s Gestapo not far behind, I might add.

Related Posts

Discover Financial Services: A Stock to Watch Post-Capital One Merger?

Discover Financial Services: A Stock to Watch Post-Capital One Merger?

Also on Market Tamer…

Follow Us on Facebook