In October of this year, the U.S. Securities and Exchange Commission adopted what it refers to as the “final rules” under which companies are enabled to buy and sell securities via “Crowdfunding”. Accompanying the adoption of those rules, the SEC approved key amendments to current SEC rules – amendments which are intended to facilitate the offering of securities on an intrastate and regional basis.

Here is a street level view of the SEC office in downtown Chicago, IL.

The initial impetus for these SEC actions came in 2012 – with the passage of the “Jumpstart Our Business Startups Act” (the “JOBS Act”). The first part (Title II) of JOBS took effect in September of 2013. But the second part (Title III) involved more complex issues, requiring much more time for the SEC to develop a consensus regarding how to fashion appropriate regulations.

SEC Chair, Mary Jo White

At the time of the unveiling of these “Crowdfunding” rules, SEC Chair Mary Jo White observed:

“There is a great deal of enthusiasm in the marketplace for crowdfunding, and I believe these rules and proposed amendments provide smaller companies with innovative ways to raise capital and give investors the protections they need. With these rules, the Commission has completed all of the major rulemaking mandated under the JOBS Act.”

“Regulation Crowdfunding” (the term used by the SEC to refer to these rules) permits individuals to invest in securities-based Crowdfunding transactions, subject to certain investment limits. The rules also do the following:

1) limits the amount of money an issuer can raise using a Crowdfunding exemption;

2) requires certain disclosures by issuers (regarding the details related to its business and the securities offering)

3) creates a regulatory framework for any broker-dealer or funding portal that facilitates Crowdfunding transactions.

Because we so closely associate “Crowdfunding” with the Internet, and more particularly, with Social Media applications, it is easy to forget that the basic concept behind “Crowdfunding” is relatively timeless.

For example, consider these facts surrounding the iconic Statue of Liberty:

- Conceived of in 1865 by Edouard de Laboulaye

- Authorities commissioned sculptor Frederic Augusta Bartholdi in the mid-1870’s to design the statue, with a goal of completion by 1876 (100th Anniversary of the U.S.);

- It was agreed that this would be a joint venture between France and the U.S.

- France would provide the Statue and its assembly in the U.S.

- The U.S. would construct the foundation base (pedestal) for the statue (originally called “Liberty Enlightening the World”)

- However, U.S. funding fell into jeopardy when government sources proved to be insufficient[1].

- A U.S. newspaper led the campaign that ultimately funded the project, motivating 160,000 individuals to contribute the money that “saved the day.”

- Surely that qualifies as “Crowdfunding”… without the Internet or Facebook!

Similar pre-Internet efforts were used during the 17th century to help fund as yet unpublished works, as well as cooperative movements in the 18th and 19th centuries which helped developed particular projects within rural areas of the United States and Western Europe.

British Rock Group: Marillion

More recently, avid fans of the British rock group, Marillion, managed to collectively raise over $60,000 in 1997 to fund a U.S. tour for the group. And other early “Crowdfunding” efforts were used to fund such projects as films or software.

Naturally, “Crowdfunding” falls into the “Alternative Finance” space, and (to oversimplify) is currently based upon a model which (generally) involves three categories of participants:

1) Project Initiator: the party that proposes the project or idea to be funded;

2) Individuals and/or groups which step up to support that project with funding;

3) Moderating Organization (“the Platform”): the entity which facilitates the gathering, recording, and accounting for the project’s fundraising efforts.

According to the “Crowdfunding” experts at massolution, which gathered data regarding 1,250 Crowdfunding Platforms (CFPs) around the world: ![]()

* CFPs raised $16.2 billion in 2014

* That amounts to an astounding 167% increase vis-à-vis the $6.1 billion raised in 2013.

CAUTION:

At this point I must tell you that, with regard to “Crowdfunding” as an avenue through which investors can dependably expect to earn a reasonable return on their investable dollars, I am an avowed skeptic.

As readers have seen me warn repeatedly through the years, the ranks of vendors and providers within the investment space quite unfortunately include far too many who profit by taking advantage of the innocent and/or uninformed.

Although earlier, I referenced several “Crowdfunding” efforts from centuries ago, you’ll notice that none of those efforts were an “investment” in the usual sense of the term![2] Those funding efforts from centuries past were (largely) to facilitate some project that those who contributed deemed sufficiently worthwhile to merit their own personal funds, without the expectation of any direct, tangible benefit.

Today, in contrast, the promoters of some “Crowdfunding” efforts suggest the prospect of future profit for those who commit funds to that effort. However, anyone who counts on “profit” from that form of “Crowdfunding” risks future disappointment. In addition, the simple fact is that “Crowdfunding” (in its current form) is still in its nascent stages and will continue evolving as time moves ahead. I just performed a cursory web search for “Crowdfunding Abuses”, and discovered a long list of links, including a site that outlines nine of the worst types of abusive/exploitive “Crowdfunding” efforts.[3] Therefore, anyone who contemplates a “Crowdfunding” investment is well advised to perform a robust web search (and related due diligence) before actually sending money.

HOWEVER…

Surely you must be thinking: “If he is down on “Crowdfunding”, why is he writing about it?”

I am down on “Crowdfunding” as an investment idea. However, I do see “Crowdfunding” as a potentially beneficial force within the realm of human benevolence!

More specifically, we are now in what is traditionally the time of year when people are most willing to be generous and charitable – in a “giving/spending mood”, if you will! In fact, as we read economic and stock market commentary between now and January, we will hear much discussion of how “good” or “strong” the “Holiday Sales” figures are this year, since that is a major contributor to GDP and our economic health![4]

What caught my eye during this past week was the growth in websites and applications that apply the “Crowdfunding” model within the realm of “Giving”… not just “Charitable Giving”, but “Gift Giving”.

What follows is a (very) brief look at a few (representative) websites within this area… a short list that is in no way comprehensive. It is only suggestive – primarily offered as a “FYI”, since many of you are likely to find it of interest.

Four of the better-known “Crowdfunding” sites are

1) “Kickstarter”

2) “Indiegogo”

3) “Rockethub”

4) “Crowdrise”

I have read some reviews of each, and have discovered (not surprisingly) there are differing opinions regarding the merits of each one (enough difference, at least, to prompt me to avoid characterizing any single one of them in particular!). I do applaud their efforts to facilitate charitable intent; and I applaud the principle applied by those[5] which incentivize projects that actually achieve their stated objective, and add a “surcharge” (of sorts) to those that do not proceed as was promised (in addition to returning to donors any funds given toward the latter).

Users/donors need to check on the details regarding the cost of using any given platform before she/he makes a contribution. For example, Indiegogo levies a 5 percent platform fee on any money raised through its site, and in addition charges a 3% payment processing charge (and 30 cents per donation). That range of “fees” is not untypical within this space

There is a slightly different type of “Crowdfunding” referred to as “Personal Crowdfunding” – often used by campaigns to fund medical expenses, educational projects, memorials, and similar charitable efforts. The biggest of these platforms is GoFundMe. During the 12 months prior to September of this year, that platform reported that it processed a donation total of $1 billion! It charges fees of 7.9 percent and 30 cents per donation… to cover its platform and payment processing costs.[6]

But what really caught my eye was the existence and growth of platforms that focus on helping students reduce their outstanding, unpaid student loan debt!

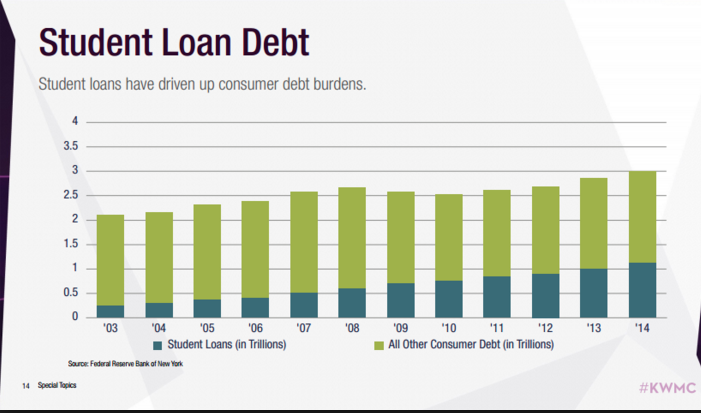

As this graph illustrates, Student Loan Debt is the fastest growing debt in the U.S.

This topic is of great interest to me because I agree with many experts that the national student loan debt situation is the “new” debt crisis for the United States. Unfortunately, all indications are that this crisis will continue to haunt the country, young adults, and our economy for decades to come. Currently, about 70% of all bachelor’s degree students graduate with unpaid student debt, and authoritative sources report that the current total of unpaid U.S. Student Loan Debt exceeds $1.3 Trillion. [See: https://www.markettamer.com/blog/innovation-as-to-tool-to-transform-lending ].

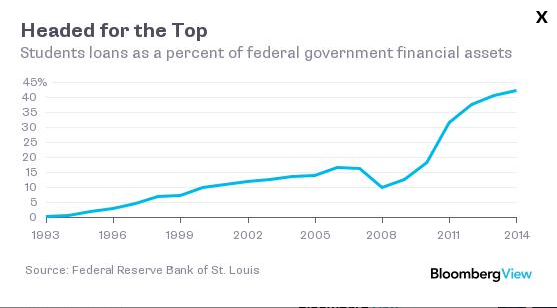

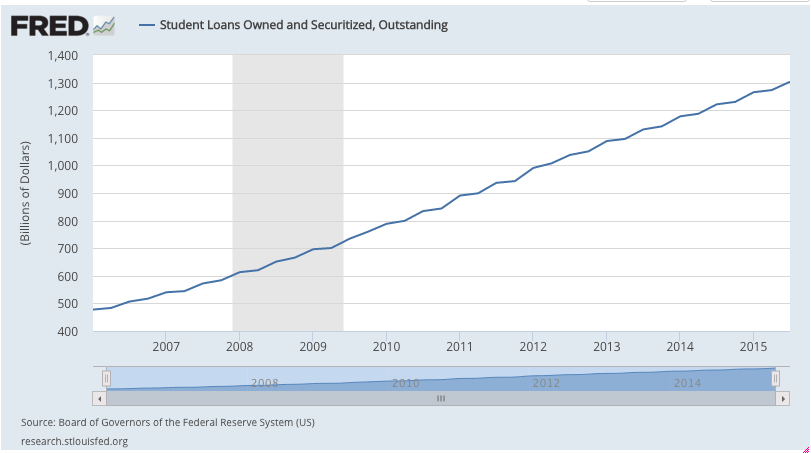

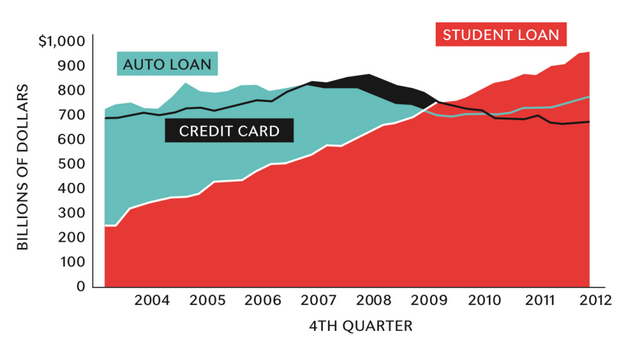

Here are three additional (easy-to-understand) graphs that suggest the magnitude of this crisis.

As a percentage of total U.S. Federal financial assets, Student Debt is at the top (approaching 50%)

This graph shows the inexorable growth of Student Loan Debt.

This graph powerfully illustrates how quickly Student Debt has swollen … and now exceeds Credit Card and Auto Loan Debt!

How can “Crowdfunding” help reduce this debt?

It’s simple:

1) If you have a child, grandchild, niece/nephew, friend, or anyone you care about who has unpaid Student Debt… and you might find it more meaningful to help pay down that debt instead of buying them a video game, a sweater, a tie, or a gift card… you can do so through one of the web platforms dedicated to this purpose.

2) If you are a student who has connections with folks you know care about you and might want to help you, you can “network” them with a website that has your loan information at hand – therefore able to quickly and painlessly pay down your debt with any donations made toward that purpose.

With the clear, upfront disclosure that I have not used any of these platforms (I became aware of them long after I had already paid off student loans taken out to pay for the college education of my three children[7]) here are the names of three platforms through which folks can engage in “Gifting” that pays down student debt:

![]()

1) Loan Gifting – is the newest of these platforms… having been launched at the end of October by RKS Design, a consulting firm. Ravi Sawhney is the CEO of RKS Design and designed the platform as a vehicle through which loved ones (grandparents, aunts/uncles, etc.) could generously gift funds to the young relative with the assurance that those funds would go directly toward paying down debt (instead of buying beer, video games, or Lord knows what). Any donations are transferred directly to the servicer of the recipient’s student loan debt.[8]

Since nothing in life is “free”, there is a cost related to this gifting – but there is no “set up” or “platform fee”. LoanGifting deducts a 3% fee from every gift (and a 2.9% fee is deducted by PayPal, or whichever payment method is used by a donor). RKS Design indicates that it is working on the development of other options that can eliminate that 2.9% fee.

https://www.loangifting.com/support

![]() 2) GoFundMe – Through August of 2015, the GoFundMe platform helped people raise more than $20 million to put toward education funds. During 2014, the site had 140,000 education-related accounts that raised $17.5 million, a 280% increase from the year before. According to the site’s president, David Hahn, “Student Loans” is one of the site’s most popular categories:

2) GoFundMe – Through August of 2015, the GoFundMe platform helped people raise more than $20 million to put toward education funds. During 2014, the site had 140,000 education-related accounts that raised $17.5 million, a 280% increase from the year before. According to the site’s president, David Hahn, “Student Loans” is one of the site’s most popular categories:

“Paying for college is one of the most expensive chapters in someone’s life. “As it turns out, friends and family are often eager to help the students in their lives achieve their dreams.”

When donations are made through the GoFundMe platform, it deducts a 5% fee, plus the 2.9% payment provider fee (as referred to above).

![]()

3) Generosity – this site was introduced earlier this year by Indiegogo. The site is specifically dedicated to fundraising for personal needs. Understandably, “Education” is one of the site’s most often used categories. According to Slava Rubin, Indiegogo’s CEO: “This is one of those areas that is gaining momentum because of how much student debt there is out there.”

According to Rubin, Indiegogo subsidizes some of Generosity’s expenses in an effort to eliminate the platform fee from the giving equation. This is how Rubin describes the fees the site charges on any funds donated through Generosity:

“Everyone should have the best possible opportunity to raise funds for themselves, their loved ones, or their favorite causes. That’s why Generosity never charges a fee for running a fundraiser. Our goal is a community of compassion and support, and platform fees are simply not a part of that equation.

“Separate from the fundraisers, our payment processor charges 3% + 30 cents on every donation to manage the transfer of funds from the accounts of donors to the accounts of organizers.”

https://www.generosity.com/

TAKEAWAYS:

1) “Crowdfunding” may feel to us as though it is “something new under the Sun”.

2) However, the concept has been in use for centuries.

3) The (transformative) difference today is the power of the Internet and Social Media to instantly connect persons around the world with issues, needs, causes, and the ability to offer/share resources that might help alleviate some of the hardship (or suffering, or economic challenge) faced by other persons

4) Platforms such as the three I have highlighted above have facilitated the linking of persons with resources …who have therefore been able to efficiently and conveniently assist other persons who are coping with one or more needs! These platforms have managed to facilitate the transfer of literally millions of dollars from those “to whom much has been given” to those who become blessed by assistance that otherwise would not be available or possible!

Especially in this “Season”, surely that is a very positive thing.

DISCLOSURE:

The author has absolutely no connection to any “Crowdfunding” site and he receives no benefit (not even a pat on the back) for highlighting their availability. I also must emphasize that I absolutely do not recommend any “Crowdfunding” site as worthy of consideration from a strictly “investment” point of view … unless you as an investor can (somehow) be absolutely certain of all the ins and outs, risks and possible rewards, loopholes, and legal details related to any given offer.

FOOTNOTES:

[1] Evidently, we are not unique in suffering from an ineffective U.S. Congress.

[2] By this I mean that those past efforts were quite different from what occurs today when an investor uses funds to purchase a stock, a bond, a mutual fund, or an ETF.

[3] See: http://www.therobotsvoice.com/2015/04/amanda_palmer_gamergate_doublefine_kickstarter_sup.php

[4] With the caveat that, as we noted in a recent article (https://www.markettamer.com/blog/at-this-rate-analysis-of-the-impact-of-interest-rates-on-stock-prices ) “Consumer Spending” is actually closer to 50% of GDP rather than 70%.

[5] According to related website(s)

[6] Per an October article that appeared in the New York Times

[7] Now aged 33, 30, and 25.

[8] Therefore, obviously, students with debt must create a “Profile” through the LoanGifting platform, providing the details related to their student loan account. The student can then inform her/his network of caring persons that gifts to pay down debt can be facilitated through LoanGifting. You may not think that interfacing with a student loan provider is challenging… but in fact, it can be. A platform such as LoanGifting has the experience and resources to make it much easier.

Related Posts

Why Union Pacific Stock Lagged the Market Today

Why Union Pacific Stock Lagged the Market Today

Also on Market Tamer…

Follow Us on Facebook