Did you experience the huge tectonic shift that occurred at the end of the fourth week of September? No, the famed San Andreas Fault did not give way, and the standard Richter Scale failed to register any meaningful reading. However, huge aftershocks were experienced in places as far apart as Denver, Chicago, New York, London (U.K.), and Munich (Germany).

“That can not be possible!” you think to yourself. “Petty is making this up!”

Sorry, my friends. I am not making this up. I am only taking the liberty of using a very familiar natural upheaval (an earthquake) as a metaphor for a sudden, powerful, reality-shifting event within the “Bond/Investment Management World” – the September 26th bombshell revealed through the press that the “Bond King”, William Hunter Gross, was jumping ship from the $2 trillion Assets Under Management (AUM) firm he founded 44 years ago to manage a relatively new bond fund for a company in Denver that almost no one associates with “Bonds”!

Under ordinary circumstances, this type of announcement would barely draw a 3rd page news story in the Wall Street Journal. Virtually every week, somewhere around the globe, one or more fund managers change investment firms. But this story was unique and earthshaking on so many levels that even I can’t possibly catch them all (and I’ve searched far and wide for “takes” on this story).

Let me lay out some essential facts for you:

1) In 1971, Bill Gross was a graduate of Duke University (Psychology) with a MBA from the UCLA Anderson School of Management. He had served in the U.S. Navy and was an investment analyst for Pacific Mutual Life. While at Pacific Mutual, he earned his credential as a Chartered Financial Analyst (CFA).

2) In 1971, with $12 million provided by Pacific Mutual, Gross co-founded the Pacific Investment Management Company, LLC (commonly referred to as PIMCO). It was created as a unit within Pacific Mutual for the management of separate accounts for the clients of Pacific Mutual.

3) Through the personal knowledge, skill, and drive of Bill Gross, in addition to some fortuitous connections and parallel developments, PIMCO started on its trajectory toward growth that (at least up through September 25th) helped it rise to become one of the best known investment managers in the world – concentrating in particular on fixed-income securities. PIMCO currently manages nearly $2 trillion in assets for individuals and institutions around the world.

4) A “parallel development” during PIMCO’s earliest years that played at least some role in the rise of Gross’ to become a “star” within the investment world was the 1972 advent of the weekly PBS TV show: “Wall Street Week with Luis Rukeyser”. Gross became a relatively frequent guest of Rukeyser, and that show was my own personal introduction to Bill Gross – soft-spoken, engaged, insightful, interesting.

a) He obviously honed his PR skills through that show, since the passing decades have found him quoted more and more often within the financial press;

b) Because of his fame and sterling long-term record, Gross has become a “fixture” on financial news shows – particularly whenever there is an important “Federal Reserve Day” on tap or some major movement has occurred within bonds.[1]

5) One sidelight about Gross that is not well-known is that, prior to beginning at Pacific Mutual and co-founding PIMCO, he was a professional Blackjack player in Las Vegas – a training ground through which he learned at least a few disciplines and insights that he later put to work trading bonds.

6) On May 11th of 1987, Gross initiated the Pimco Total Return Fund (PTTAX), a mutual fund which grew to become a behemoth – at one point laying claim to the title: “the largest mutual fund”.

a) Even following recently outsized redemptions, it is still the “largest bond mutual fund” – with well over $220 billion AUM leading up to September 26th.

b) Since inception through 8/31/14, PTTAX out-performed the Barclays Aggregate Total Bond Market Index by an average of 1.06% per year.

c) According to Morningstar, during a recent ten year stretch, PTTAX returned 6%, once again beating that Barclays Index… but by a much more impressive margin – since the Index only gained 1.4%. That placed the huge PTTAX in the top 5% within its category, quite a feat given the challenges of running a fund that huge.

Here is a photo of Bill Gross in much happier, more carefree days (1999) before the Financial Crisis, Quantitative Easing, Fed Tapering, and Allianz SE came into his life!

![]()

7) In 2000, Allianz SE (AZSEY)[2] purchased PIMCO and placed it as an autonomous operation within its “Investment Management” arm: Allianz Asset Management.

![]()

a) Allianz SE (phonetically: aliants) is a fascinating European firm based in Munich, Germany. We’ll delve more into AZSEY in a bit.

b) Its Allianz Asset Management division (based in Munich) is the holding company that oversees investment management operations:

i) Allianz Global Investors, headquartered in Frankfurt, Germany[3]; it operates out of four offices in the U.S.

ii) PIMCO, headquartered in Newport Beach, California.

![]()

8) Through the fourth week of this past September, PIMCO proved to be a fortuitous acquisition for AZSEY.

a) PIMCO continued to grow its fund offerings, an effort made easier by the growing fame of Gross and the record of PTTAX.

b) PIMCO became the first to “clone” an existing actively managed fund (PTTAX) into an ETF[4], PIMCO Total Return ETF (BOND).

c) PIMCO now runs three of the largest actively managed ETFs: BOND, PIMCO Enhanced Short Maturity Short Term Fund ETF (MINT), and PIMCO 0-5 Year High Yield Corporate Bond Index ETF (HYS).

d) Between 1998 and 2013, PIMCO saw a 16-fold increase in its AUM.

e) As a result of that growth, it became (through August, 2014) the fifth largest fund group vis-à-vis AUM.

f) Through its funds, ETFs, and management of institutional “third party” assets (endowments, pension funds, insurance companies), PIMCO has become one of the world’s premier investment management firms.[5]

In the context of our increasingly globalized economy, it is not at all a surprise that a European firm would acquire PIMCO. However, I venture that most U.S. investors, if polled before September, would not have been able to offer much detail about Allianz SE. From the name, some might even guess that the firm is French; listen to the pronunciation yourself and imagine any Frenchman you choose speaking it: http://upload.wikimedia.org/wikipedia/commons/9/9e/De-Allianz.ogg.

It is not my purpose here to offer you a broad history of Allianz. However, its story is fascinating enough to share in summary form:

1) AZSEY is a global financial services company with a particular focus in the insurance space.

![]()

2) Its size and significance is suggested by the following statistics:

a) AZSEY is the world’s largest insurance company;

b) It is the world’s 11th largest financial services company;

![]()

c) Its Allianz Asset Management division ranks within the top five global investment managers, reporting over 1.8 trillion (EURO) AUM;

i) In 2010, third party assets constituted almost 80% of its AUM.[6]

ii) Because Gross served as a manager within several funds, and because of his international fame (used as a marketing tool by investment consultants for endowments and institutions), it has been estimated that Gross held direct influence over about 25% of those third party assets.

c) Based on Forbes’ composite measure, AZSEY is the 25th largest global corporation.

d) Its “global” nature is reflected in its earnings split – with only about 50% of earnings being attributed to Europe!

3) Therefore, in the world of finance, AZSEY is a “big deal”, even if not widely familiar within the U.S.

4) During the past two years, PIMCO has accounted for approximately 28% of the operating profits for its parent company, AZSEY.

a) Therefore, even though Allianz S.E. is a huge global financial services company, PIMCO has been a vital part of its growth and success in recent years!

b) So Gross and PIMCO have been a “big deal” within the sprawling global giant that is AZSEY! (Keep that at the forefront of your mind.)

The journey that brought AZSEY to its current prominence is interesting. It was founded in 1890 in Munich as a marine and accident insurance company. It expanded to London three years later. The next 97 years reflect AZSEY’s amazing resilience, as it grew in scope and reach despite the adversity of two World Wars (its Munich HQ was destroyed in World War II).

The decade of the 1990’s witnessed AZSEY in an “expansion” phase… including the acquisition of the familiar U.S. insurance brand, Fireman’s Fund, followed by PIMCO.

As company growth continued, AZSEY decided to secure 100% control of an Italian subsidiary. Since it needed to make an organizational change and members within the European Union community were growing more tightly entwined, AZSEY management and board chose to transform itself for the future by becoming one of the first entities to become a “European Company” (Societas Europaea). The process of moving from a German holding company to a “SE” was commenced in September of 2005 and became official 13 months later. AZSEY now does business in over 70 countries.

This is the flag of the European Union.

I was struck by management’s decision in 1993 to commission a new archive for its corporate history. That new “openness” regarding its past led (before 2000) to it joining with four other companies to create the “International Commission on the Holocaust Era” (ICHEK), which has processed insurance claims unjustly denied during and after WWII.

This is an image of one of countless artifacts found in the updated corporate archive of Allianz SE.

The marketing of the Allianz “brand” has taken many forms, perhaps most visibly through its sizable sponsorship of Formula One racing and its heavy stake in football (what the U.S. refers to as soccer).

This is a shot of the outside of Munich Stadium, a prime of example of how the company markets itself through sports.

Allianz wanted quite badly to secure the naming rights for the stadium used by the New York Giants and Jets (the New Meadowlands in New Jersey). However, its WWII heritage brought AZSEY far too much “baggage” for popular opinion in the U.S. (especially New York and New Jersey) to cope with the thought of that stadium bearing the Allianz brand; so the AZSEY bid for those rights was rejected.

Moving back to PIMCO, it threaded its way through the Financial Crisis (2007-09) in better shape than many other investment management firms. In the months following the worst of the Crisis, Gross and his (then) PIMCO colleague, the much-travelled and high profile, Mohamed El-Erian, coined a phrase that became all-too-familiar to consumers of financial news in the following years: “the New Normal”. This term was intended to convey the pairs’ expectation that global economies would grow more slowly moving forward, and investment gains would become proportionally smaller than those to which investors had grown accustomed. The frequency with which references were made to “the New Normal” in speeches, interviews, commentaries, etc. served to increase the visibility (and notoriety) of PIMCO, El-Erian, and Gross.

While working at PIMCO, El-Erian kept a grueling schedule of world travel and public speeches. He was a tireless promoter of the PIMCO brand. Here he was in Dubai!

Thus far, you have likely grasped that, through the end of 2012, PIMCO and AZSEY were prospering, and Gross enjoyed the side benefits of the growth of his “legend” as “Bond King” – earned through his over 40 years of long-term performance as a bond manager, as well as his virtually unmatched comprehension of the many dynamics that interact within the various bond asset subcategories (Treasuries; Corporates; Municipal; Asset-backed; Sovereign; Emerging Markets; High Yield; etc.). In fact, Morningstar named Gross the “Manager of the Decade” in 2010 in recognition of his outstanding performance.

Gross was sought after for interviews and speaking engagements, regularly received calls from U.S. federal officials (Geithner, Bernanke, etc.), and (as we’ve seen) was widely quoted. In fact, in a world choking on an excess of investment commentary, Gross’ monthly market commentary distinguished itself (much as do Buffett’s commentaries) by being informative, engaging, and even entertaining. The “Bond King” even had an “empire” (of sorts). He presided over an investment firm with over 700 financial professionals (including about 240 portfolio managers) and a “Trading Room” that comes close in size to a U.S. football field!

Then in 2011, Gross’ “crown” tilted a bit as he failed to catch a rally in U.S. Treasuries – pushing his record that year to the lowest 25 percentile. Things became worse in 2013, when Gross and PIMCO projected that the U.S. economy had not reached “escape velocity”, meaning that growth would continue for a couple of years at 2% or lower. That underlying outlook led to portfolio decisions that were out of step within a market spooked by Bernanke’s use of the word “Taper” in May of 2013. PTTAX lost 1.9% in 2013 – its biggest loss in almost 20 years – leaving it underperforming about two-thirds of its competitors. Needless to say, redemptions escalated – totaling over $72 billion through November of 2013. No surprisingly, therefore, in December of 2010, PIMCO’s COO, Douglas Hodge, referred to Bernanke’s infamous use of “Taper” as the “five letter word”!

As we have seen with other legends, when the press senses “vulnerability” in a “star”, they pounce. Just as the press taunted Warren Buffett in recent years when his portfolio seemed to underperform, so the press began taunting Gross. All things being equal, one might think that someone who graduated with a degree in psychology (as Gross did) could handle this change of fortune smoothly.

Unfortunately, that was not the case. There have been such a plethora of “reports” on Gross’ demeanor and behavior during the later half of 2013 into this year, many of which come without attribution to a specific person speaking “on the record”, that I will only summarize the most germane reports here:

1) He has always been a manager with very high expectations for his staff and employees;

a) He expected those with whom he worked to demonstrate the same drive and discipline exhibited by him;

b) Therefore, he often made his disappointment tangible when traders or managers did not make it to the office by the time of the opening of trading in New York (remember that West Coast time is three hours behind Eastern time);

c) Gross did not like to be “looked in the eye” on the trading floor;

d) Because he was so competitive (performance wise) and driven, he was reportedly abrasive, prickly, difficult (you pick your favorite adjective);

i) Based on a number of reports, he often shared his feelings, opinions, and judgments bluntly, without regard to how many other folks were listening.

e) From May of 2013 through August of 2014, PTTAX experienced 16 straight months of net outflows… moving it from a $292.9 billion fund to a $222 billion fund!

i) As the net outflows grew, antsy AZSEY investors exerted pressure on AZSEY CEO, Michael Diekmann, to remediate this obvious “problem”.

ii) Undoubtedly, Diekmann put pressure on executives at Allianz Asset Management, who put pressure on COO Hodge, who had heart-to-heart conversations with El-Erian (CEO) and Gross (CIO).

This is a photo of Hodge during an interview with "Pensions & Investments"

2) Imagine yourself a “legend” in your field, virtually universally recognized as amazing, with an unparalleled track record. However, you fall into a very difficult run (after all, you are human) and suddenly you feel beset and besieged by those “at the top” in Munich and Newport Beach. The “you” who succeeded for so many years hasn’t changed much, but you aren’t getting the same sterling (very profitable) “results” everyone has been used to.

a) How do you handle the resulting pressure?

b) Evidently, Gross could have handled those pressures better.

i) Famously, in January of 2014, El-Erian dropped the bombshell that he was leaving PIMCO and his $100 million job to “spend more time with his family” [yes folks, that works out to almost $274,000 per calendar day!]

ii) The introduction of six new “Deputy CIO’s” came soon after El-Erian’s departure. It doesn’t take a rocket scientist to presume that idea did not come from Gross.

iii) Within weeks, it is revealed that El-Erian often clashed with Gross regarding management style and how best to lead PIMCO moving forward.

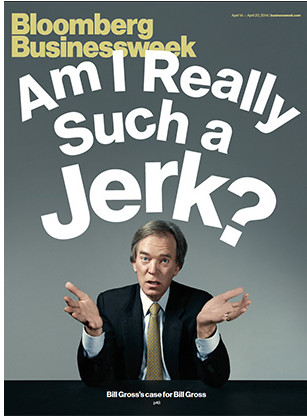

iv) By April, the newsstands are populated with this cover story from Bloomberg Business Week.

Isn't it amazing what the press will put on magazine covers these days?!

a) Stories emerge recounting “erratic behavior” by Gross, including an overheard and heated exchange between Gross and two Wall Street Journal writers working on a story about PIMCO’s challenges.

b) Reportedly, upper management reduced Gross’ interaction with clients at Newport Beach meetings.

c) Stories also emerged of at least one Deputy CIO (running one of PIMCO’s best performing funds of the past two years) threatening to resign if Gross didn’t leave.

3) In June, Gross was one of the main speakers at a Morningstar Conference in Chicago.

a) He came out wearing sunglasses.

b) His speech did not nearly conform to expectations, and countless articles about the event speculated regarding the mental state exhibited by Gross.

4) As the asset outflows continued, pressure on Diekmann and on the PIMCO board grew in frequency and magnitude.

a) At that point the board did what every board should do in any organization with a “key person” who is 70 years old – it developed a succession plan.

b) Gross got wind of that by at least the second half of September and sensed that his future at PIMCO was not secure.

c) Feeling misunderstood, far underappreciated, and unfairly mistreated, he began to talk with other firms to feel out opportunities – even spending time conferring with West Coast rival “bond guru”, Jeffrey Gundlach (founder of Doubleline Capital[7].

d) However, Gross’ “Ace in the Hole” was that one of his former colleagues at PIMCO, Richard Weil[8], now serves as the CEO at Janus Capital Group, Inc. (JNS) – a high flying fund powerhouse during the years leading up to the Dot.com Crash.

i) Janus’ equity funds thrived on tech stocks.

ii) Those funds crashed and burned when the “Bubble” burst.

iii) Janus has seen five changes at the top of management since 2002.

iv) In sharp contrast to PIMCO’s nearly $2 trillion AUM, Janus manages a mere $177.7 billion.

This brings us to Thursday, September 25th. After a full day trading at PIMCO (per usual) Gross called Gundlach to inform him that Gross was heading to JNS, with the announcement to be made Friday morning.[9]

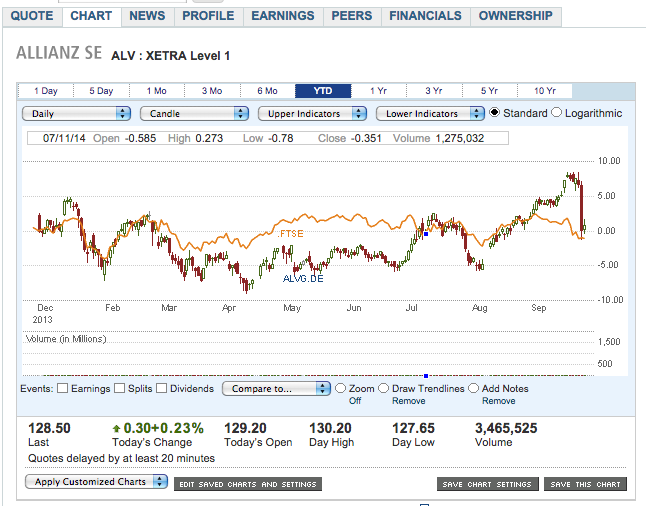

The next morning dawned in Newport Beach, appearing to be just another trading day… except that Gross was on an airplane heading to Denver, and some market shifting news was about to hit the wires. The investment landscape was taken by surprise and shocked … even experts were at a loss to project how the money management landscape would “shake out” in the months ahead! Take a look at this chart of ALV (on the Frankfurt Exchange):

And here is a chart of the U.S.-traded AZSEY (that is quite a “gap down”):

On Friday, September 26th, Allianz suffered a decline in excess of 6% (the biggest in nearly 3 years).

More illuminating regarding the impact and tenor of the issues surrounding PIMCO, COO Hodge and his superiors at Allianz Asset Management and Allianz SE were caught flatfooted and stunned.

Here is part of the account from Bloomberg regarding the 26th from the perspective of Allianz and PIMCO (bold font added by me for emphasis)

“It was 2:28 p.m. in Munich on Sept. 26, and Bill Gross, in charge of $2 trillion as chief investment officer at Pacific Investment Management Co., had just announced that he was joining Janus Capital Group, Inc. (JNS), a struggling stock fund manager. With Allianz shares starting to slump, the German insurer called its U.S. asset management arm to confirm that the most influential bond manager had just quit.

“Pimco … hadn’t known either, according to people familiar with both firms.

“Gross, 70, had left the bond giant he helped found 43 years earlier without telling its executives, a last act of defiance by a great investor whose strained relationship with his lieutenants had brought him to the verge of being ousted. As shares of Allianz fell the most in almost three years and Pimco traders worked to contain the fallout of his departure — the news sparked a selloff in markets for Treasuries, credit derivative indexes and the Mexican peso.”

That day, Gross (who through the years had oft times been credited with moving this or that market) was likely blamed for more movement in bond prices than ever before in his career. Even the relatively obscure (at least for us) iTRAXX Index in Europe went wild after the announcement, despite the reality that Gross traded very little in European high yield issues.

There were countless peculiarities about that day’s trading. Here are just a few:

1) Money flew out the door at PTTAX, ensuring that the string of consecutive monthly net outflows would grow to 17;

2) The big Gross ETF, BOND, despite weathering the recent performance storms much better than PTTAX, took a huge hit.

a) Street One Financial VP, Paul Weisbruch, felt compelled to borrow a Will Ferrell adjective to describe trading in BOND that day: “volume … was ginormous… the fund traded 2.7 million shares before 11:30 AM EST on ADV of about 204,000 shares… The fund has not traded volume levels like this since early 2013.”

b) Later reports revealed that BOND experienced fund outflows of $446.5 million on Friday, and another $98 million the following Monday.

c) No one can say with certainty exactly where those dollars went. However, it was reported that:

i) Gundlach’s funds received hundreds of millions in new funds … the second highest net inflow of funds the firm has ever received (not far behind an exceptional day it had soon after its launch).

ii) iShares Core U.S. Aggregate Bond ETF (AGG) took in over $447 million.

Meanwhile, 1023 miles east of Newport Beach, prospects were looking (way) up. The stock of JNS was catapulted upward by over 40% (what a gap up):

A number of commentators drew parallels between the exit of Gross and the departure of Derek Jeter from the New York Yankees…

suggesting that Gross’ exit was of a similar magnitude to Jeter’s leaving IF Jeter had signed on with the hated Boston Red Sox instead of retiring. Alas, that analogy does not nearly do the Gross exit justice.

The much more accurate analogy would be if Jeter had left the lofty Yankees for the perennially beaten down Chicago Cubs[10]. The total bond AUM managed currently by Janus totals a laughable (by comparison with PIMCO at least) $31.4 billion – just 17.7% of Janus’ total AUM!!

Janus is opening an office for Gross in Newport Beach, but it will absolutely not be the size of a football field, and Gross will need to depend much more upon himself for keeping abreast of the markets, designing strategies, and finding appropriate bond issues. He will be managing the relatively young (and small) Janus Unconstrained Bond Fund (JUCAX).

The evidently long simmering tensions between Gross and his superiors at PIMCO and Allianz SE were apparent within their respective statements following the news of this big change. What is telling is not what was said, but what was left unsaid!

Here is the summary of the PIMCO statement (from WSJ’s Moneybeat): http://blogs.wsj.com/moneybeat/2014/09/26/pimcos-blunt-statement-on-bill-gross-fundamental-differences/

“PIMCO, a leading global investment management firm, announced that Co-founder and Chief Investment Officer (“CIO”) William H. Gross, has resigned and will leave the firm, effective immediately. The firm has a succession plan in place and its Management Board, comprised of its Managing Directors, will confirm shortly the election of a new Chief Investment Officer. Relevant portfolio management assignments will also be announced at that time.

Said Mr. Hodge: “While we are grateful for everything Bill contributed to building our firm and delivering value to PIMCO’s clients, over the course of this year it became increasingly clear that the firm’s leadership and Bill have fundamental differences about how to take PIMCO forward.”

Mr. Hodge continued: “As part of our responsibilities to our clients, employees and parent, PIMCO has been developing a succession plan for some time to ensure that the firm is well prepared to manage a seamless leadership transition in its Portfolio Management team. Earlier this year, the firm established a new portfolio management leadership structure that reflects our long-held belief that the best approach for PIMCO’s clients and our firm is to evolve our investment leadership structure to a team of seasoned, highly skilled investors overseeing all areas of PIMCO’s investment activities.”

Said Michael Diekmann, Chief Executive Officer of Allianz Group: “Since becoming part of the Allianz Group in 2000, PIMCO has grown enormously and contributed consistently to Allianz’s success. We join our PIMCO colleagues in recognizing Bill Gross for his work over the 43 years since PIMCO’s founding. The management and investment structure put in place in January as well as the thorough succession planning gives us complete confidence in PIMCO’s investment and executive leadership team.”

Mr. Hodge added: “We have built a deep bench of talent with extensive investment and leadership experience, including more than 240 portfolio managers globally, and our outstanding team around the world gives us the scale, talent, expertise and commitment to manage this transition. We will continue to add and promote talent at all levels to help us drive our firm forward. We are energized and fully focused on serving our clients today and into the future.”

No flowery rhetoric there … no flowing salute to the “Bond King”, the legend of Newport Beach and Wall Street! They have a “succession plan” in place and a “deep bench”!

For his part, here is the initial statement from Gross:

“I look forward to returning my full focus to the fixed income markets and investing, giving up many of the complexities that go with managing a large, complicated organization. I chose Janus as my next home because of my long standing relationship with and respect for CEO Dick Weil and my desire to get back to spending the bulk of my day managing client assets. I look forward to a mutually supportive partnership with Fixed Income CIO Gibson Smith and his team; they have delivered excellent results across their strategies, which deserve more attention.”

Gross looks forward to a “mutually supportive partnership”…! And nothing is said about the company he helped found and build! Perhaps the feedback he received after that initial statement led him to feel a need for further explanation… namely:

“It was not without great thought and deliberation over quite some time that I decided to begin this next chapter. It is a time for me to reduce executive and people management responsibilities at a larger firm and focus on the pure aspects of portfolio management at a smaller one. Janus is the right fit at the right time in my career — and my life.”

The statement from Janus CEO, Richard Weil, is (by contrast) upbeat and flowery (bold font inserted by author for emphasis):

“Mr. Gross will be based in a new Janus office to be established in Newport Beach, California and will be responsible for building-out the firm’s efforts in global macro fixed income strategies. His concentration on such strategies will be separate and complementary to Janus’ existing and highly successful credit-based fixed income platform, built under the leadership of Janus’ Fixed Income Chief Investment Officer, Gibson Smith.

“Bill Gross has an exemplary track record with decades of success and he will offer an exceptional approach to navigating today’s increasingly risky markets with a focus on macro, unconstrained strategies. His involvement provides Janus a unique opportunity to offer strategies and products that are highly complementary to those already managed by our credit-based fixed income team. With Bill leading our global macro efforts and Gibson our credit-based fixed income team, I am confident Janus will be able to meet the needs of virtually any client.”

What a study in the complexities of human and corporate relationships!

INVESTOR TAKEAWAY

When a “legend” leaves the setting within which she/he built, elaborated upon, and embellished their reputation, it is (borrowing from VP Joseph Biden, with a bit of editing, of course) “a big frickin’ deal!” There are currently not many true “legends” in the investment world … certainly not any approaching the longevity and accomplishment of Warren Buffett or Bill Gross.

The affable, folksy "Oracle of Omaha" (Warren Buffett) is frequently referred to as the premier investor of his era. If that is true, then Bill Gross could be called the premier Bond investor of his era.

Once upon a time, there was Peter Lynch (the legendary master manager of the Fidelity Magellan Fund).

Peter Lynch retains his title of "legendary", despite having retired relatively young, when he was at his peak.

And William Miller held “legendary star status” for a very long time through the performance of Legg Mason Capital Management Value Trust (LMVTX). That fund outperformed the S&P 500 Index for a record 15 straight years, until 2005. Then Miller’s “Midas Touch” lost its luster, and he retired from the fund (in relative obscurity) in 2012. That is an example of how tough it is to create a “legend” these days.

William Miller was the "star" at Legg Mason for over 15 years!

Now the media blitz is on to advise individuals and institutions whether to keep their money with PIMCO or move it to Janus, Doubleline, iShares, Vanguard, or some other bond manager. Significantly complicating matters is the recently announced probe by the SEC of the valuation methods used by a few funds at PIMCO. Even assuming that PIMCO is innocent of any wrongdoing, that probe places a “red flag” of warning on PIMCO – particularly for institutional investors and advisers who must explain (and justify) any negative, below benchmark performance numbers to clients or stakeholders. In those circumstances, “cover your assets” is often “top of mind”.

Combine that with the exit of the “Bond King”, and it is anyone’s guess what the future will hold in terms of performance and fund flows at PIMCO. However, some factors have already clearly emerged, including:

1) Morningstar has lowered its forward-looking rating on PTTAX by two notches… from gold to bronze. They don’t question the ability of the persons named to follow Gross as manager; but they are uncertain about fund flows and management changes. [The landscape has shifted.]

2) Morningstar issued a report quite critical of PIMCO’s oversight, noting that the board is “short” by two independent trustees. So instead of having in place the specified five outside trustees, PIMCO only has three. As Morningstar points out, this is especially inopportune during a time of major transition, stress, and change! [Another red flag for institutions and advisers.]

3) The nation’s largest pension fund, CALPERS, announced it is keeping its funds at PIMCO for the present, as they perform due diligence on a forward-looking basis.

4) The price drop of AZSEY was so sharp that, for financial analysts at least, it implies a loss of AUM (going forward) for AZSEY in the range of $400 billion. Some see that as a function of overblown, unjustified pessimism.

a) AZSEY has already been struggling with an underperforming Fireman’s Fund subsidiary.

b) However, if one presumes that the Fireman’s Fund woes were already discounted in AZSEY’s stock price in early September, such investors would be considering the purchase of AZSEY shares near or below the closing price on September 26th.

5) It should be much easier for Gross to “make a performance difference” at Janus than it has been to outperform within his massive portfolios of the past.

a) However, as noted, he will need to relearn how to function at a much smaller scale.

b) Time will tell how successful he will be.

c) However, even if he is massively successful, it is doubtful (objectively speaking) that whatever incremental new fund flows he brings to Janus will justify the huge initial price jump in JNS shares.

i) It is often stated that the market’s horizon is six-months into the future

ii) Assuming that axiom is correct, I’ll eat my hat if Gross pulls in enough new funds to grow the total incremental fees/earnings at Janus high enough to justify that escalation in price!

The bottom line is that Gross’ unexpected announcement on September 26th was indeed, within the landscape of investment management and Wall Street, a “Tectonic” event that was felt as far away as Munich and the Frankfurt Stock Exchange. In light of the fact that the adjective most often used for people and/or topics that relate to Germany is “Tutonic”… then this can be considered a “Tutonic” event! Of course, the “rumble and aftershocks” were also felt as close to home as New York (the NYSE), Chicago (the bond trading pit), Denver (the home of JNS) and Newport Beach!

The full depth and breadth of this “Tutonic Tectonic Shift” will only be discerned as all of the after shocks and the recovery processes run their course in the months to come!

DISCLOSURE: The author has regularly owned a number of PIMCO funds – from PTTAX and BOND to HYS and MINT. Prior to the “Dot.com Crash”, he also owned numerous Janus funds. The author confesses that he has also had the privilege of watching Gross actually become “Bond King” – remembering him well from those early appearances on Wall Street Week. The author wants Mr. Gross to know that if he can be helpful to Mr. Gross in the months ahead – even as a focus for Mr. Gross to vent his daily frustration, the author will be honored to work with Mr. Gross at just one eighth the salary that was paid to Mr. El-Erian!!! I think I could struggle along with just $34,250/day!! Mr. Gross should take note that I have a MBA in finance and am certified as a C.F.P.

Nothing in this article is intended as a recommendation to buy or sell anything. Always consult with your financial advisor regarding changes in your portfolio – either subtractions or additions.

FOOTNOTES:

[1] Gross is almost as constant a fixture on CNBC during “Fed Days” as the channel’s own Steve Liesman!

[2] AZSEY is the U.S. OTC ticker. The European ticker on the Frankfurt Exchange (XETRA) is ALV

[3] It was remarkably difficult to confirm that location (rather than Munich) on their website. The only confirmation I could find was a footnote in very small font written in German that included a Frankfurt address.

[4] A feat that many experts thought was unlikely, since the daily portfolio disclosure requirements for an ETF would expose a famed portfolio manager’s “best ideas” to becoming diluted through copycatting, among other reasons.

[5] During my time as endowment fund administrator for a post-graduate school, all members of the investment committee knew precisely what PIMCO was great at – because of Bill Gross.

[6] Most of these third party assets are managed through three distinct entities: PIMCO (bonds), RCM (equities), and DEGI (real estate).

[7] Gundlach founded Doubleline after being fired by TCW. He has built Doubleline into a well-known, well-respected fund company; and Gundlach has emerged as the second most often quoted expert on bonds.

[8] Weil served as managing director and COO

[9] That was an insightful courtesy on Gross’ part to let Gundlach know in advance.

[10] There is your analogy! The Cubs have been “World Series Free” for over 100 years!

Related Posts

Could Buying a Simple S&P 500 Index Fund Today Set You Up for Life?

Could Buying a Simple S&P 500 Index Fund Today Set You Up for Life?

Also on Market Tamer…

Follow Us on Facebook