The Boston-based consulting firm, DALBAR, has just released the 21st (annual) edition of its coveted Qualitative Analysis of Investor Behavior (QAIB). Alas, the study confirms that the “average investor”[1] continues to shoot herself (himself) in the foot on a regular basis!

![]()

Specifically, while the S&P 500 Index offered a return during 2014 of 13.69%, the average equity mutual fund investor garnered a return of just 5.5%. You could drive a Mack Truck between those respective return figures – a massive gap of 8.19%!! Expressed differently, the Index returned almost 2.5 times the performance of the average investor.

In the same vein, “Joe Investor” did even worse managing a bond portfolio! For the 2014 year, the Barclay’s Aggregate Bond Index returned 5.97% (almost a half percent better than “Sally Investor’s” equity return!) … while the average fixed income mutual fund investor finished the year with a paltry 1.16% profit.[2]

Isn’t this Dalbar study illuminating?! It should be no surprise that (on average) U.S. investors do not generate returns that would “set the world on fire”. But for Joe and Sally Investor to fall so miserably short of both the equity and fixed income indices must indicate that something inside of us pushes us toward extraordinarily counter-productive investment decisions.

It is at such revelatory moments that the following thought can easily spring to mind:

“If only I could be like Warren Buffett!!! All my problems would be over!”

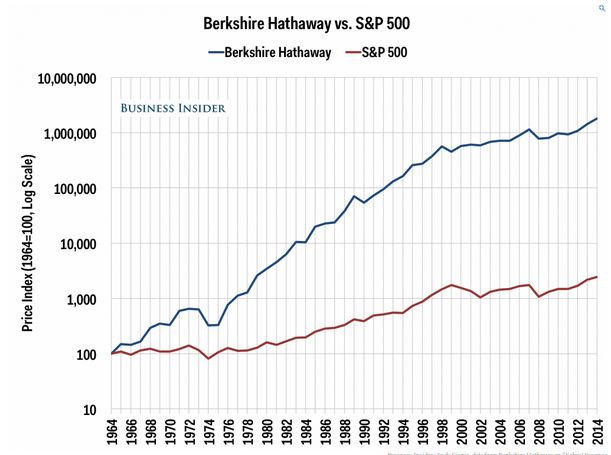

Buffett's Berkshire Hathaway (BRK.A) has out-performed the S&P Index by such a huge margin that it takes a Logarithmic Graph to do justice to the scale of that out-performance!

Buffett has been universally acknowledged as such a “Master” at his craft that long-time Vanguard Group icon, John Bogle[3], was quoted in February telling the Financial Times why we cannot be “like Buffett”:

“Beethoven could tell you how to write a symphony but you can't write a symphony like Beethoven does.

“You can't copy, with any hope of success, a Beethoven or Buffett. You can copy Bogle at any moment of time. Just buy the damn index fund.”

What is it that Buffett has that we don’t have?[4] We don’t have his vision, patience, or discipline (among other things)!

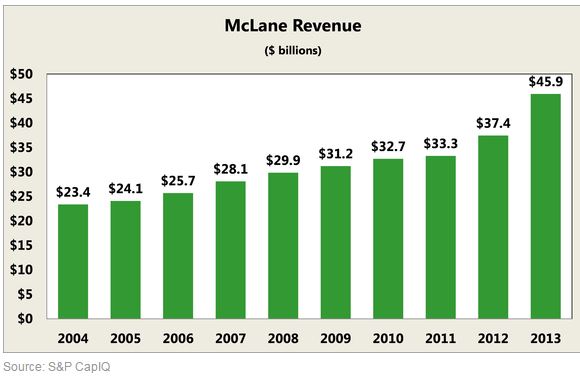

For example, back in 2003-2004, Buffett saw something promising in a company that pumped out $23.4 billion in annual revenue – but that was relatively unknown in the popular press. Its low profile was likely due to its almost invisible operating margin of 0.9%!! And yet, despite that puny margin – Buffett’s vision saw potential in the company’s future!!

Therefore Buffett purchased the McLane Company from Walmart (WMT) for just $1.5 billion![5]

Buffett then directed his lieutenants to expand McLane’s customer base and sales, cut expenses, and increase margins![6]

See what BRK.A has achieved with McLane in just ten years… almost doubling its annual revenues.

Just as impressively, through its own growth and an acquisition, it has expanded its product line and its customer base – adding (among others) 7-Eleven and YUM Brands (YUM)[7]. It has also increased its margins by 20%!![8]

Now take a guess regarding which BRK.A companies generate its greatest share of Operating Revenue:

GEICO?

- This insurance giant is typical of the cash flow generators in which Buffett loves to invest.

This giant railroad has been a great performer for Buffett

The Burlington Northern Sante Fe?

Berkshire Hathaway Energy?

- This company is part of Buffett's “Energy” holdings

The answer is “None of the above!!”

The fact is that the biggest Revenue Source for BRK.A is the McLane Company… and not by a slim margin at that!! Here is the share of BRK.A Operating Revenue generated from each unit:

McLane (26%)

Burlington Northern Sante Fe (12%)

GEICO (11%)

Berkshire Hathaway Energy (9%)

As an ironic addendum, $13 billion of BRK.A’s revenues come from WMT through McLane – since WMT still generates almost 30% of McLane’s sales!!

So the odds that either you or I could “become” a Warren Buffett clone are about as likely as me becoming a Beethoven clone!

However, at the risk of angering any powerful forces that might live on Mount Omaha alongside the immortal “Oracle” himself[9] … just because Buffett is exalted does not mean that he is “perfect”. Much as the infamous Greek mythological warrior, Achilles, demonstrated vulnerability… so too has Buffett (upon occasion) exhibited counter-productive decision-making!

An excellent case in point is his decision in 2011 to load up on IBM (IBM) common stock. Buffett dabbled in IBM during Q1 of 2011 (buying just 4.5 million shares)… then he became more aggressive in Q2 and Q3 (purchasing more than 82 million shares) . By November of 2011, he announced the acquisition of almost 6% of IBM’s common share float – worth (at that point) $10.7 billion. (Total BRK.A ownership of IBM later moved up to 7%).

What had Buffett seen in IBM back in 2011 to motivate such a large investment? Well, there is the obvious:

1) A well-established, iconic U.S. (and international) brand;

2) A steady dividend;

3) Growing EPS.

But based upon quotes from that period, it appears as though Buffett was “wowed” by management. In Berkshire’s 2011 Annual “Letter”, Buffett lauded IBM CEOs (Lou Gerstner, followed by Sam Palmisano) for continuing a steady stream of capable executive leadership that lifted IBM from the specter of bankruptcy in 1993 to become an international corporate force once again.

In that light, Buffett cited:

1) “Extraordinary” operational accomplishments

2) “Their financial management was equally brilliant”

3) Demonstrable financial flexibility

“I can think of no major company that has had better financial management, a skill that has materially increased the gains enjoyed by IBM shareholders.”

It became clear that Buffett’s attention was riveted by the IBM “2010 Roadmap” that was rolled out in 2007. What captured Buffett’s eye was the early 2011report that demonstrated the achievement by IBM of all of the benchmarks laid out in the Roadmap! He even expressed regret that he hadn’t recognized much earlier IBM’s appeal as an investment and jumped in sooner!

As a result, it might have been “regret” because of a perceived missed opportunity that persuaded Buffett to buy into the “2015 Road Map”… in full view by the start of 2011! Buffett started accumulating (rather fatefully) his huge position in IBM. And of course, everyone who remembers October of 2014 remembers IBM’s CEO abandoning the “2015 Roadmap” as she announced one of the most dismal major corporate financial reports (relative to IBM goals and analyst projections) in recent memory.

This pose of IBM CEO Virginia Romnetty could be captioned: "What Roadmap?? We don't have a Roadmap any longer!"

At this point, it would be entirely fair to say: “OK, Petty, so what if Buffett couldn’t foresee the magnitude of IBM’s near term challenges in 2011? Could you have done any better?”

The obvious answer is that I am no “Oracle”. Prescience is not my forte!!

However, this is what I could have seen:

1) A great deal of IBM’s financial success from 2007 through 2010 was based upon “Financial Engineering” – massive stock buyback programs that reduced the number of outstanding common shares … thereby increasing EPS!! In a corporation that has significant organic growth, that is not an issue. But in a very mature, slow growth corporation operating in a competitive, rapidly evolving industry… such “engineering” runs the risk of making metrics look better than they really are;

2) An extremely insightful and successful investor was interviewed by Bloomberg back in 1998. Remember, if you will, that those were the heady days when “Technology” was the ultimate solution to all of our issues… tech startups were popping up nearly every day… and the now famous investment term “Dot.com” came into vogue. Those were also the days when demand for tech stocks was ramping up … starting to push prices upward. By March of 2000 the price of the PowerShares QQQ Trust (QQQ reached such a “Crescendo” level that it proved to be an all-time high from which it tumbled and could not fully recover until just recently (a decade and a half later)!

This particular portfolio manager was quizzed regarding if and when he would buy shares in his own friend’s company – Microsoft (MSFT). Surely he was going to buy, wasn’t he?? His answer to the question was telling:

“The answer is no, and it’s probably unfortunate. I don’t know what that world will look like in 10 years, and I don’t want to play in a game where the other guy has an advantage over me.”

Well, that was a very on target observation… wasn’t it?!! His insight saved him and his shareholders a lot of pain when the “Dot.com Bubble” burst and crashed!!

Surely you have guessed the identity of that portfolio manager who offered the now famous quote above! It was none other than the Oracle himself! For some reason… whether it be “regret” over a perceived lost opportunity… or being snowed by a charismatic pair of CEO’s… or a felt need to deploy the huge pile of cash on hand… Buffett forgot his own insight!! That insight is trenchant within the world of technology[10]: “I don’t know what that world will look like in 10 years, and I don’t want to play in a game where the other guy has an advantage over me.”

Virginia Romnetty (the current IBM CEO) expressed this key issue very succinctly when she said:

“Our results also point to the unprecedented pace of change in our industry.”

Ruminating upon all of this in my car the other day, I suddenly heard the voice of the Qualcomm (QCOM) CEO on Bloomberg radio addressing that company’s under performance and promising to adjust his company’s “Roadmap” to more accurately reflect the competitive landscape as it exists today. I couldn’t help but think to myself:

“Could it be that any technology company today that depends upon a ‘Roadmap” might just as well follow the ‘Yellow Brick Road’?”

Let me hasten to add that I was not really serious in thinking that. Of course I realize that every company has to have a plan… an itinerary… a planned route through which to direct corporate operations going forward. But I marvel at the dual fact that Warren Buffett recognized the unpredictable (and potentially treacherous) nature of major tech investments back in 1998… and that he didn’t recognize that same danger within the (by then) financially engineered IBM in 2011.[11]

INVESTOR TAKEAWAY

We each have at least one weakness as an investor. Even the (almost) universally vaunted “Oracle of Omaha”, Warren Buffett, has demonstrated the existence of an Achilles Heel!!

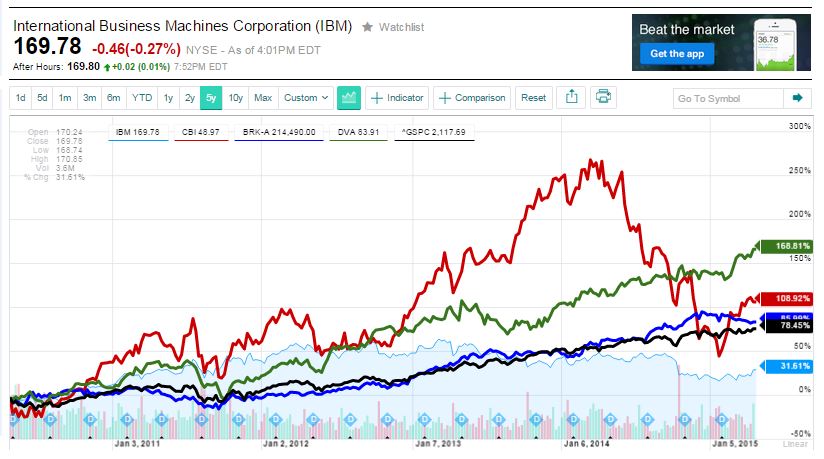

Let’s visualize what Buffett’s “Achilles Heel” with regard to his foray into IBM cost him and his shareholders. If we look at a five year chart, we see that IBM (the prices designated by the light blue “area” graph… at the bottom of the chart) under-performed the S&P 500 by about 31.5% to 78.5% (the black line)… and trailed BRK.A as a whole by even more (31.5% to 86%!). IBM also trailed two other significant Buffett holdings… the mercurial Chicago Bridge and Iron (CBI) (red line) at 109% for the period and the much steadier DaVita HealthCare Partners (DVA) (green line) at 162%!!

This graph illustrates the "drag" on the performance of BRK.A over the past several years caused by Buffett's major stake in IBM!

Unfortunately, Dalbar’s annual study has made it painfully obvious that quite a number of us (Sally & Joe Investor) are beset by enough weaknesses to result in our annual investment return numbers being an utter embarrassment!

What is particularly galling is that if we could just park our ego for a year or two… put behind us the notion that “we can do so much better than any single ETF or fund”… invest our funds in an Index (or better yet, a series of indices across enough asset classes to constitute a diversified, balanced, efficient portfolio!)… and not get distracted by the cries of “Bear!” or “Crash!” or “Taper!” that eminent daily from CNBC, Fox, and Bloomberg … we would do ever so much better!!! (And sleep better, too!)

So if your return has been averaging less than half of the return of the S&P Index (as reported by Dalbar) … or much worse, less than a third of the return from the Barclay’s Aggregate Bond Index… for heaven’s sake… choose one (or any combination) of the following for your investment allocation(s):

BRK.A

SPDR S&P 500 ETF Trust (SPY)

PowerShares QQQ Trust (QQQ)

iShares Russell 2000 Index (IWM)

iShares Core U.S. Aggregate Bond (AGG)

And if you absolutely insist on something more interesting… you could scope out the Market Tamer “Covered Call Screener” on IBM and discover metrics on 74 different Covered Call possibilities… including this one (buy 100 shares of IBM and sell a June 175 Call for a net debit of $168.19):

This is a screen shot from the Market Tamer "Covered Call Screener"

holding out the prospect of a 6.28% annualized return if IBM moves up enough by June 20th that the option gets “assigned”. And if it does not get assigned, you remain eligible for the 2.7% dividend yield and you keep the $1.65 of premium you received when you sold the call!

In fact, when I reread my October 30, 2014 article on IBM, I saw the projection with which I concluded that article:

“based on its currently ravaged technicals, you’ll likely have an extended period of time during which IBM will sit in a range in the mid-160’s (or lower) before it tries to mount a sustainable up move! “

Take a look at the 6 month chart of IBM (late October through the present):

Since October 30th of last year, IBM has stayed below $170 as I predicted in my article published on that date.

So anyone who began selling Covered Calls at either $170 or $175 back in early November would have collected and retained call premium, collected the dividend, and be sitting (price-wise) right about where I anticipated we’d be now. Not a bad return!!

If you stick with strategies such as these in a disciplined fashion, you will outperform “Sally and Joe Investor”!!

DISCLOSURE:

There are moments when the author could be the “Poster Child” for the “Joe Investor” results illustrated in the Dalbar study! I have a whole catalogue of “holes in my foot” from past investment errors made and regretted. That being said, I do own a number of Index funds and ETFs… and I have owned positions in BRK.B at various points. I have even held a variety of bear call spreads and bull put spreads in IBM. Nothing in this article is intended as a recommendation to buy or sell anything. Always consult with your financial advisor regarding changes in your portfolio – either subtractions or additions.

FOOTNOTES:

[1] By definition, of course, all Market Tamer subscribers are “Above Average” investors!!!

[2] If investment returns were a track and field race, the Barclays Index “lapped” the average fixed income mutual fund investor over 5 times!!!!

[3] A contemporary of Buffett.

[4] Besides billions and billions of dollars, of course.

[5] Note that back in 2004, $7 billion of McLane’s sales were to WMT itself

[6] The McLane Company is wholesale distributor of groceries and other items to stores across America

[7] YUM includes Kentucky Fried Chicken, Taco Bell, Pizza Hut, etc.

[8] OK, OK… a jump from 0.9% to 1.09% isn’t going to get you 20 minutes on CNBC… but it is still 20%!!

[9] Obviously, I am likening the international reverence paid to Buffett to the reverence the ancients paid to Zeus on Mt. Olympus!!

[10] Ever since the dawn of the computer age, “Moore’s Law” has been a constant reminder regarding the speed with which information grows, technology evolves, and hardware/software/services risk losing competitive advantage!!

[11] In fact, in my earlier article on IBM… https://www.markettamer.com/blog/think-before-you-invest … I suggested that Mr. Palmissano saw “the writing on the wall” regarding imminent expiration of the benefits that accrued from financial engineering. Therefore he retired early… so that Ms. Romnetty (and not Palmissano) would be the one forever remembered as having the abandonment of the 2015 Roadmap be “front and center” in any account of their legacy.

Related Posts

Why Intel Stock Sank Today

Why Intel Stock Sank Today

Also on Market Tamer…

Follow Us on Facebook