Our loyal Market Tamer readers know that occasionally I enjoy putting them in the chair of a corporate CEO. So I hereby officially designated you as the CEO of pharmaceutical company “A”. I am your just-hired[1] shrewd, insightful, industry consultant; and you’ve asked me to offer you a SWOT analysis[2] of your company, with emphasis upon weaknesses and opportunities.

Given our limited column space, below I will offer you a greatly condensed version of my analysis, and let you then begin to discern what course you feel that you and your team should follow looking forward.

STRENGTHS:

1) Exceptional Performance: kudos to you and your team!

1) During your first 18 months as an independent company, you have managed the business with great skill!

This firm has outperformed all competitors except one during the past 18 months!

2) Here are highlights among your metrics thus far:

Your 1st Quarter Adjusted Gross Margin was 78.40%

Return on Equity (ROE) exceeds 100%

You expect total Sales this year of $19 B (up 3.2% YoY[3])

Your Operational Cash Flow is $5.7 B

You have accumulated $9.6 B of Cash (and Equivalents)

Your stock price has moved upward by almost 60% (vs. 30% for the S&P 500).

During the past 18 months, this company's stock has appreciated by about twice as much as the S&P 500 Index (in red).

Not surprisingly, your Market Cap has grown from about $55 B to (at a recent high) over $92 B (a 67% increase)

67% of your stock float is held by institutions.

Your stock sports a 3.2% yield

S&P has granted you an “A” credit rating.

3. You have two very promising new drugs in the final stages of trial prior to approval

Drug #1 will address a global market for a condition that the World Health Organization reports afflicts 130-150 million people globally

- There are 3-4 million new cases each year

- Your drug has a 99% cure rate

- You’ve received “accelerated approval” status in Europe, with the possibility that sales can commence during the 2nd Q of 2015.

Drug #2 will treat patients suffering from locally advanced breast cancer[4]

- The current trial is a randomized, double-blind study enrolling 270 breast cancer patients….

- The drug is also being evaluated for several other oncology indications — Including non-small cell lung cancer.

WEAKNESSES:

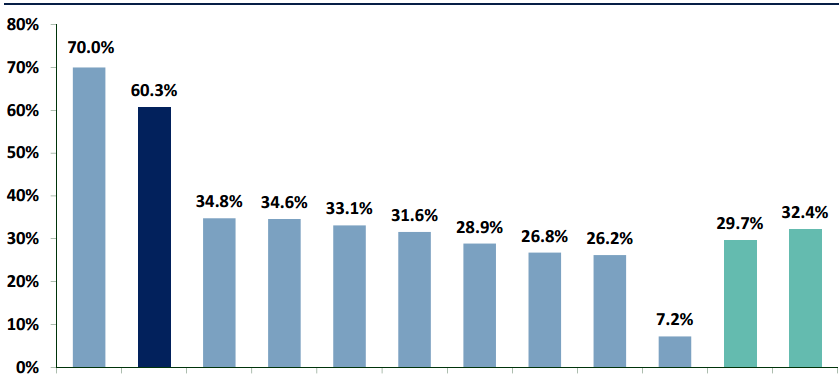

1) One single product accounts for 57% of your total sales

- That product grew sales YoY at 15%

- That is superb performance

- However, its patent exclusivity (in the US) runs out in December 2016

- Even though it is a biologic drug, the ACA-related legislated act titled “Biologics Price Competition and Innovation Act” makes it much easier for a Generic Drug manufacturer to create and receive approval for a generic version of your drug – which (by the way) happens to be the top selling global drug!

2) The next two best-sellers accounted for only 5.5% and 4.4% of sales

- Neither of those products showed growth YoY in 2013!

- Because of your heavy reliance upon one product for Revenue, your company stock quite likely trades at a lower P/E multiple than it would otherwise.

This company's top drug product accounts for almost 60% of total sales!

3) Your promising new drug (point C under Strengths) is coming on the market over one year after Gilead Sciences (GILD) commenced sales of its competing drug; therefore, GILD has momentum:

- It is expected that your treatment (all oral) will be less expensive – a significant advantage

4) Of your accumulated cash totaling almost $10 billion, most of it is overseas, limiting your access to employing that cash without exposing it to a second layer of income tax – with that added layer coming at the world’s very highest rate[5];

5) Your company carries $14.7 B of total debt, resulting in a Debt-to-Asset Ratio of 50.

6) Your dividend Payout Ratio is higher than ideal at 62%.

7) You must have used extremely gifted accountants last year, since your effective income tax rate was 22% (13% lower than the statutory U.S. rate).

THREATS:

1) Even though you have increased your Research and Development budget by a significant amount in order to quickly diversify your product portfolio, you are running out of time and there is never any guarantee that drugs currently moving through the standard (three) phases of FDA trials will receive approval and become successful.

2) As competitors continue to buy out smaller, more rapidly growing biotech and drug companies, there are fewer good candidates for your company to choose as a strategic acquisition.

3) The U.S. government is very likely (after the November 2014 Election, of course) to “close the door” on the ability of U.S. global companies to legally change their tax domicile in order to avoid double taxation on global income (and cash).

OPPORTUNITIES:

1) In today’s market, the most common strategy employed by major Pharma companies that need new products to replace “run outs” on patent expirations is to acquire smaller firms with a drug portfolio that can provide a “good fit” (either supplementary or complimentary);

2) We have found you a prospective acquisition!

- This firm has been growing through acquisition

It purchased four firms in 2013;

It has purchased one firm thus far in 2014.

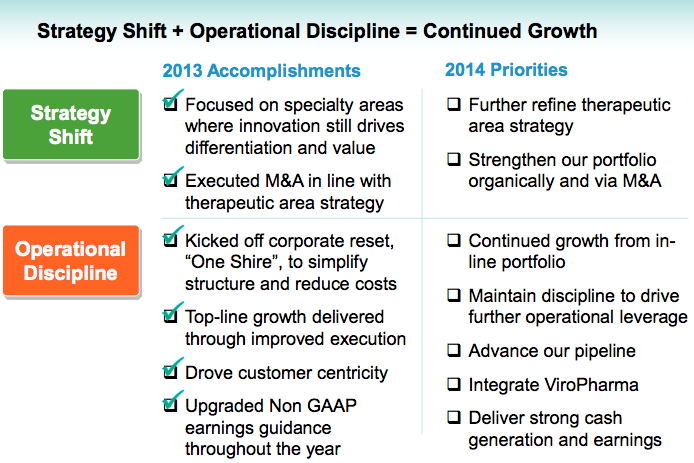

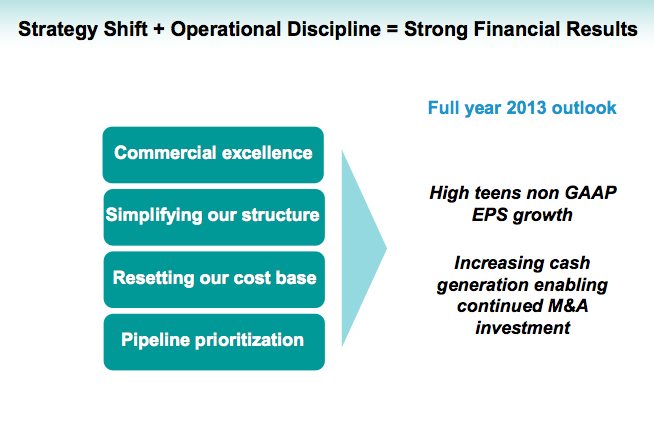

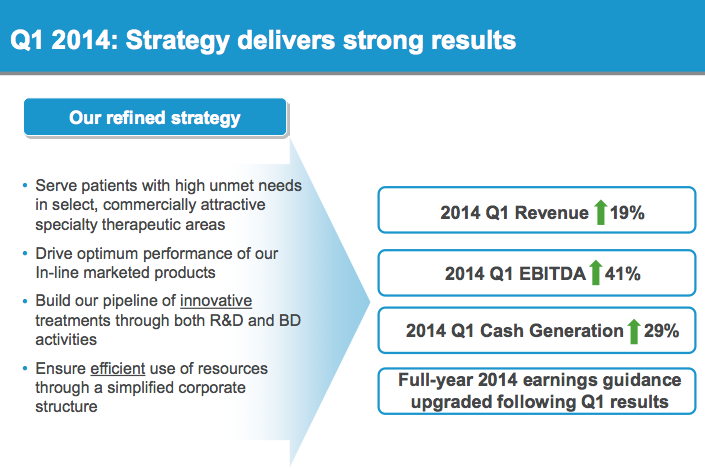

Our "Target" company has shifted corporate strategy toward growth and operational efficiency!

3) It is relatively rare among growing, mid-sized drug firms because it does not have any controlling shareholder(s).

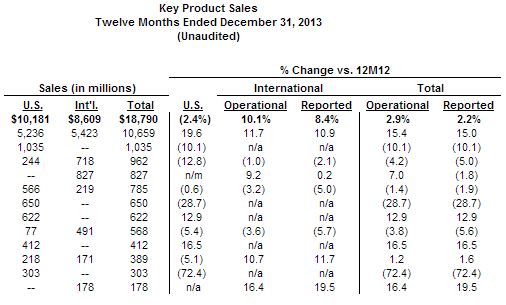

- It reported almost $5 B in Revenue for 2013 (up 9% YoY)

- Not including “discontinued operations”, it reported $1.42 B in Earnings (up 75% YoY)

The strategy shift applies to both existing and developing products.

4) It has two major drug product

A. One reported over $1 B in Sales

B. The other reported Sales of $0.5 B

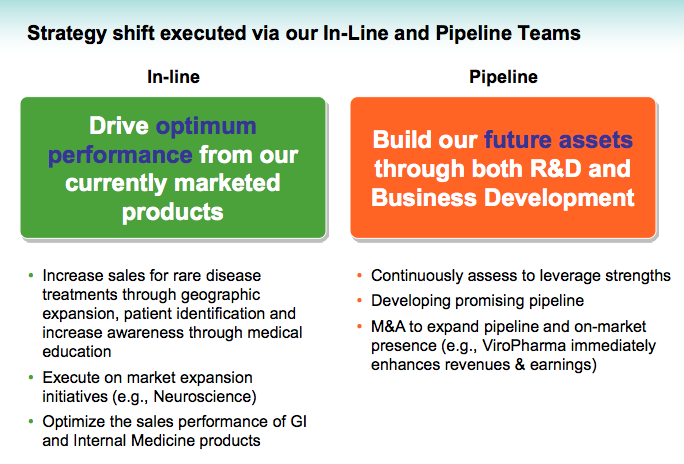

5) It has numerous products closing in on Phase 3 of FDA trials… and the portfolio would broaden your product line significantly… including products that address several of the highest growing pharma sectors, including: rare diseases, neuroscience, metabolic diseases, T-cell antagonists, neonatal treatment and multiple emerging oncology programs.

A. As you and your Board know, both Europe and the U.S. FDA offer incentives to drug companies that develop drugs to serve the medical needs of patient diagnostic groups under 200,000 persons.

B. They provide tax credits and an accelerated approval process.

6) During 2013, the current CEO repositioned and realigned its business… including a strategic focus on rare diseases and greater operational discipline.

Our Target has been seeing improving financial results through this strategy shift.

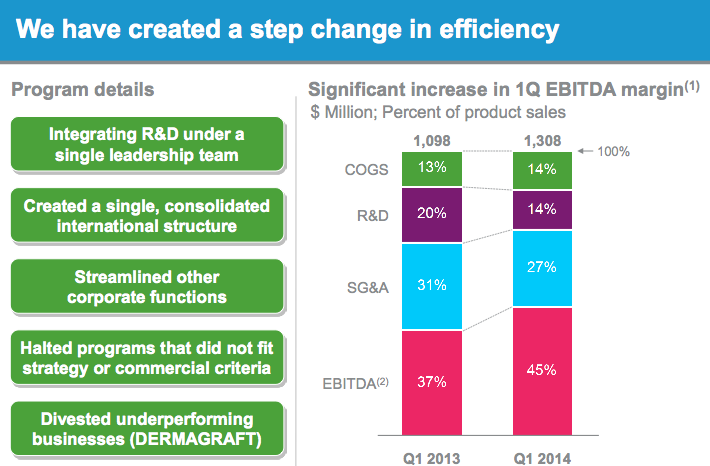

A. For example, it combined three separate R&D units into one, consolidated unit

i) That move will produce both interdisciplinary synergies (in research) and

ii) Cost savings (R&D cost as a percent of Revenue moved from 20% to 14%.).

The Target firm's Margins have been growing.

7) That CEO has projected that the firm will double Revenue (to $10 B) by 2020 – with a 70% increase in Sales from existing products and 30% from drugs newly approved between now and 2020.

A. For perspective, analysts are projecting $8.5 B in Sales by 2020.

8) This firm has no debt and $2.2 B in Cash

7) In 2013, its effective tax rate was 16.4% (almost 4% higher than the official rate in its domicile).

1st Q 2014 results were particularly strong!

8) This company fits the profile of a Tax Inversion acquisition[6]

You could lower your income tax rate to as low as 13%, but not until 2016.

One analyst projects the first year savings to be $325 M.

9) Cautions

A. This firm’s sales are heavily concentrated in ADHD (Attention Deficit Hyperactivity Disorder) – at 37% of firm Sales!.

Since ADHD treatment is controversial in the eyes of many doctors, many potential acquirers have been put off by that concentration in years past.

However, this firm’s product line would serve to reduce your blockbuster drug’s share of total sales (within a combined company) to just 45%.

The combined companies would also serve to reduce dependence upon ADHD drugs!

Another major U.S. Pharmaceutical company has already been in talks to acquire this company… but negotiations have not moved (yet) toward a concrete offer.

If you are interested in pursuing the acquisition of this promising company, we can provide our expertise throughout the impending negotiation process, which will most likely meet with significant resistance … because this firm is clearly on an ascendant path of sales growth and industry recognition, as well as investor interest. Because of that reason, this firm’s CEO and Board are almost certain to be reluctant to lose the firm’s independence.

Therefore, the key to these negotiations will be making an extremely enticing (and credible) presentation that makes a compelling case regarding mutual synergies and opportunities that will inevitably result from the combination of:

1) Your company’s strong global infrastructure – (including) a marketing network throughout 170 nations, a depth of experience within the regulatory approval area, a global network of physician and provider networks, and especially your wide access to key emerging country markets;

2) The existing products and promising string of “final stage trial products” that are the strengths of this impressively growing firm we have targeted for your next acquisition!

This firm’s products will broaden and diversify your current product portfolio (and likely lead to a higher P/E Multiple) and your global marketing and regulatory infrastructure can and will expand market demand (and availability) and significantly accelerate sales for their products! This will, without doubt, be the fastest and most efficient way for our “Target” to “scale up” – perhaps even to a level beyond what any of them have yet envisioned!! In our eyes, this is quite clearly a “Win Win” for both companies!

The most challenging decision with which you, your management team, and your board will be faced as we proceed … is to discern and agree upon the maximum price that you are willing to pay for this promising acquisition! You and your colleagues are well versed in the dangers of “overpaying” – whether one refers to Warren Buffett’s lessons and quotes regarding the art of Valuation or one prefers to think in terms of GARP (“Growth at a Reasonable Price”).

The company we have profiled for you is currently valued at approximately $38.58 B. We recommend that you start your bidding at a level just above value – perhaps $39.705 B – fully understanding that this first offer will be rejected.

After the initial offer, we can hope for direct or indirect feedback (from the target’s CEO or Board, or from industry analysts, experts, or big fund managers) regarding the price level at which a successful offer will need to be set.

During this process, our firm can provide you with a feedback loop, with financial models based on your preferred assumptions, and with the benefit of a depth of real market experience (provided by our top consultants) that few (if any) other firms can match. However, our firm can never presume to tell you what you should do… since it is you and your Board who are responsible (legally) to fulfill your fiduciary responsibility to your shareholders. In this instance, that fiduciary obligation is to perform due diligence through a cost/benefit analysis of any acquisition – to ensure that you can demonstrate that any given acquisition will be accretive enough to future Revenue and Earnings to justify the actual purchase price agreed upon. We will consider it a privilege to assist you and your team in performing this due diligence, but we will always depend upon you to make the “final call” on any offer!

Do you have any questions?

Let’s set a date and time for a follow-up meeting.

INVESTOR TAKEAWAY:

I personally think that walking through the above “Case Study” (or “Exercise”) is a great way for the average investor[7] to grow in her/his insight regarding the challenges of corporate management. When we take a bullish position in a company, we (of course) want management to demonstrate its utter brilliance by astounding Wall Street with “Above Consensus” earnings, extremely positive forward guidance, and perhaps the “hint” of a new product just on the cusp of being formally “Rolled Out” to the market! And of course, when we enter a bearish position, we want management to act as though they are a modern-day equivalent to the “Keystone Kops” – unable to do anything right![8]

However, real life investing (as we know) is never that easy or that “cut and dried”. And the management of a company is never as “straightforward” as it may seem to us as we look on from the sidelines!!

Therefore, I hope you take this opportunity to imagine yourself as CEO very seriously and give real thought to how YOU would move Company “A” forward into an even brighter, more exciting, and more prosperous future!

What I suggest you focus upon are the following:

1) What are the top three most important issues that Company “A” needs to address in the coming year?

2) Will acquiring the “Target” described above be an effective means of addressing one or more of those needs?

a) If “yes”… then how will you know what a “maximum reasonable purchase price” should be?

b) If “no”… then what alternative strategies would you suggest?

3) If you choose to pursue (and acquire) the “Target” company, what will you need to “give up” or “sacrifice”?

a) For example, most of your current shareholders place a high priority on “returning value to shareholders” (example, a good dividend).

b) Given your Payout Ratio and Debt-to-Asset Ratio, once you become more leveraged (due to the acquisition), will you need to decrease your current level of delivering value to shareholders?

Part II will be published very soon. Within it, you will find more details about the actual business operations of Company “A” and the “Target” firm than you would be able to find in any one spot anywhere else within a publication available to the general public! And I am guessing that 75-80% of you have already identified the two companies referred to above!

DISCLOSURE: The author has carried a bullish position in Company “A” almost constantly since it became a publically traded stock. Nothing in this article is intended as a recommendation to buy or sell anything. Always consult with your financial advisor regarding changes in your portfolio – either subtractions or additions.

FOOTNOTES:

[1] I am extremely affordable, but invaluable and without peer!

[2] Strengths, Weaknesses, Opportunities, Threats: SWOT

[3] YoY: Year Over Year

[4] As you know as CEO, the technical description for this condition is “those suffering from human epidermal growth factor receptor 2 (HER2) negative metastatic”.

[5] Very important! This comes from the “Tax Foundation” [http://taxfoundation.org/blog/us-has-highest-corporate-income-tax-rate-oecd]:“In today’s globalized world, U.S. corporations are increasingly at a competitive disadvantage. They currently face the highest statutory corporate income tax rate in the world at 39.1 percent. This overall rate is a combination of our 35 percent federal rate and the average rate levied by U.S. states. Corporations headquartered in the 33 other industrialized countries that make up the Organization for Economic Cooperation and Development (OECD), however, face an average rate of 25 percent. Even corporations in high-tax European countries such as Belgium (34 percent), France (34.4 percent), and Sweden (22 percent) face much lower rates than those in the United States. Our largest trading partners—Canada, Japan, and the United Kingdom—have each cut their corporate tax rates over the past few years to become more competitive.”

[6] This means that acquiring it would enable your company to create a new, non-US, tax domicile.

[7] Of course, none of our Market Tamer investors are “average”… they are all “Above Average”!!!!

[8] Here is a short sample of the Keystone Kops in their Silent Movie Era glory… https://www.youtube.com/watch?v=a8jphxpi1ro

Related Posts

Why Redwire Stock Looks Red Hot Today, and RTX and AeroVironment Are Rising

Why Redwire Stock Looks Red Hot Today, and RTX and AeroVironment Are Rising

Also on Market Tamer…

Follow Us on Facebook