Could this man be the "Next Buffett"??

Here is a thought for you:

When was the last time you purchased $160,000 worth of equity Calls on a U.S. stock because it was rumored as a potential “Warren Buffett Acquisition”?

Oh, you’ve never done that?

Well, there’s one more thing you and I have in common!! If I tried to place an order for $160,000 of any option, my friendly broker would fall all over herself in hysterical laughter – wondering when and how I had lost my senses … and knowing that my “portfolio margin” account wouldn’t even support a $16,000 purchase!!).

However, on March 10, one trader who obviously has little in common with you and I purchased 4,000 $62.50 Call options due to expire on March 20. The purchase came with the underlying stock sitting just a bit over $61/share… so the buyer needed the stock to move up over 2.5% in just 11 days to break even! That sounds pretty gutsy to me given that the market had been bumping up against resistance!

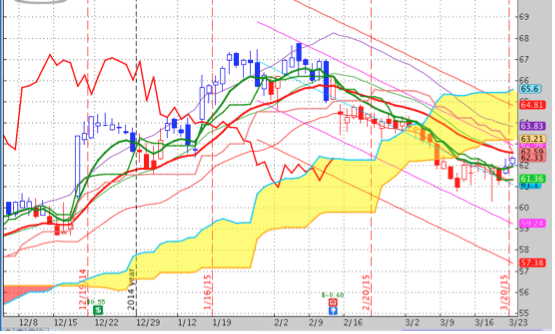

Here is our "mystery company's" graph from the end of 2014 through the first three weeks of March. Note it had been in a pronounced downtrend.

Seemingly much less risky… but involving five times more capital, a second investor purchased 10,000 June 67.5 Calls on the same stock at $0.70/each (ie. $700,000 total). In that case, the trader was counting on an 11% price lift before expiration – but he would enjoy three months of time value for that move to play out.

Let’s see what drew the attention of these traders… and presumably of Buffett… to this company:

If we analyze the company based on its reported $1.75/share net income…

When it stood at $55/share… that means it was valued at 31 times income.

During 2014, the company’s revenue was essentially flat, while net profit slipped by 62% due to higher commodity prices and special post-employment benefit plan charge-offs.

Worse, in March of this year, the company suffered a huge blow to its quality image when it had to recall 6.5 million boxes of one of its signature food product due to contamination by metal!

In 2012, its stock was summarily dropped from the Dow Jones Industrial Index. Also in 2012, the company was part of a corporate split that separated its overseas operations/brands (Mondelez International (MDLZ)) from its domestic-oriented businesses. Very significantly, the company granted a $7.2 billion “goodbye” dividend to MDLZ as they split!! And continuing in that “giveaway” spirit, the company has distributed $3.2 billion to shareholders (through share repurchases and dividends) since then! [Note that its “Free Cash Flow” (FCF) during the timespan that incorporated these “giveaways” was merely $3 billion. Add up all of that cash “out the door” and you get $10.4 billion – versus the mere $3 billion FCF it generated during that time span. Is that how to run a business? But more on that later.]

Meanwhile, the company has found it very challenging to keep up with changing consumer food ingredient preferences (consumers continue moving toward “organic” and “natural”) and the company’s margins have been squeezed by recent rises in the pricing of the commodities used across its product mix.

Compounding matters further, the CEO was (per rumor) pushed out last December due to weak performance, and in February, both it’s CFO and CMO exited.

Finally, perhaps most shocking of all, Buffett dumped a significant pile of the billions he owned in this stock back in 2010 because of a public and strident difference of opinion with the then CEO regarding her sale of an existing strong (pizza) brand to purchase Cadbury PLC. Not mincing words, Buffett described the CEO’s decisions at that time in no uncertain terms: “Both deals were dumb!”

So I ask you: Does a slow growth (actually “no growth”) company in a mature market (over 98% of its sales come within the U.S. and Canada) that has recently (as described earlier) dumped so much of its cash (relative to its “FCF”) sound like a “great company at a bargain price”??[1]

The obvious answer is “No”!

Not withstanding the above, a huge multi-party acquisition was announced on March 25th– engineered by the fascinating partnership that has grown between 3G Capital Partners[2] (led by Brazilian billionaire, Jorge Paulo Lemann) and Buffett’s Berkshire-Hathaway Corporation (BRK.A). The acquisition target was the company described above: The Kraft Foods Group, Inc. (KRFT). And the orchestrators of this offer made sure the terms were compelling for KRFT shareholders:

1) KRFT shareholders will receive a $16.50/share “special” cash dividend – a dividend that is 27% of the closing price of KRFT the day prior to the announcement! The dividend will be funded by 3G Capital and BRK.A so as not to burden the combined company with a higher debt load (ie. leverage).

2) KRFT business operations will be merged with those of the H.J. Heinz Company (acquired by 3G Capital and BRK.A in 2013) to form The Kraft Heinz Company.

3) KRFT shareholders will receive 49% of the stock in the new company, while Heinz shareholders will hold 51%;

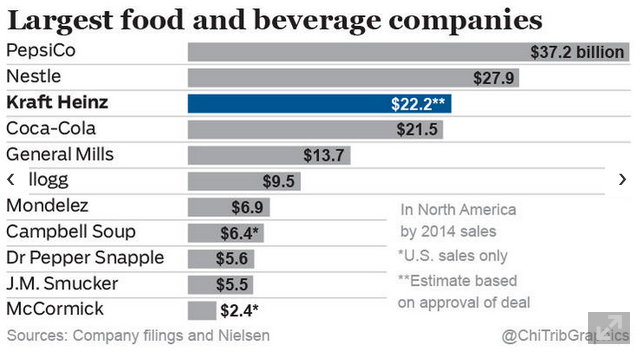

4) The resulting combination will rank as the 3rd largest food corporation in North America and the 5th largest in the world.

In addition, the new company will have annual revenues of approximately $28 billion and will control eight brands that generate over $1 billion in revenue annually… with another five brands that bring in between $500 million and $1 billion annually!

The stated rationale for this merger can be oversimplified as follows:

1) Heinz is an international powerhouse (62% of sales are generated beyond North America) – therefore the plan will be to leverage KRFT brand sales beyond North America via the Heinz marketing/distribution network and leverage increased domestic sales for Heinz brands through the KRFT network.

2) As 3G Capital has definitively established via its prior takeovers (Anheuser-Busch InBev (ABI)[3], Heinz, Burger King, etc. it is a masterful manager of large consumer brand companies – able to cut costs, increase margin, and build a stronger company.

a) As an example, it has increased the gross operating margins at Heinz by 8% since taking over its operation.

3) Therefore, as expressed by the soon to be Board Chair of the merged company, Alex Behring[4]:

“By bringing together these two iconic companies through this transaction, we are creating a strong platform for both U.S. and international growth. Our combined brands and businesses mean increased scale and relevance both in the U.S. and internationally. We have the utmost respect for the Kraft business and its employees, and greatly look forward to working together as we integrate the two companies.”

4) Building on those thoughts, John Cahill (current KRFT CEO and soon to be Vice Chair of the merged company, offered these thoughts:

“Together we will have some of the most respected, recognized and storied brands in the global food industry, and together we will create an even brighter future. This combination offers significant cash value to our shareholders and the opportunity to be investors in a company very well positioned for growth, especially outside the United States, as we bring Kraft's iconic brands to international markets. We look forward to uniting with Heinz in what will be an exciting new chapter ahead.”

[Note: Bernardo Hees, currently CEO at Heinz, will become the CEO of the merged entity.]

5) And not to be forgotten, the Oracle of Omaha himself had this to say:

“I am delighted to play a part in bringing these two winning companies and their iconic brands together. This is my kind of transaction, uniting two world-class organizations and delivering shareholder value. I'm excited by the opportunities for what this new combined organization will achieve.”

Building on our references above regarding how leadership in the new, merged company will be divided[5], here is what we know:

- The new board will consist of 16 folks – five chosen by the KRFT board, five by the Heinz board, and three each from 3G Capital and BRK.A;

- It will co-headquartered in Pittsburgh and Chicago (to preserve the unique heritage and “local presence” of each component company.[6]

The announcement included some bold projections (not promises):

- “The significant synergy potential includes an estimated $1.5 billion in annual cost savings implemented by the end of 2017.”

- “The transaction is expected to be EPS accretive by 2017.”

- “The Kraft Heinz Company plans to maintain Kraft’s current dividend per share… Kraft has no plans to change its dividend prior to closing.”

- “The Company is fully committed to deleveraging in a timely manner and to maintaining an investment grade rating going forward.”[7]

Here are some fascinating sidelights regarding the merger story:

- This is the third time Buffett has been drawn to Kraftbrands:

- Long ago, Kraft brands were a part of General Foods, a stock owned by BRK.A.

- BRK.A bought Kraft stock in 2008…. had his difference with management (referred to earlier) and largely divested after Mondelez was spun off.

- So this big deal is Buffett’s third approach to owning a share of the iconic brands within the Kraft product catalogue!

* Buffett is quoted as having said (in a CNBC interview) that the deal took just four weeks to complete.[8]

* Once the merger is consummated, former Kraft and Heinz stockholders will share ownership of about 50% of the merged company, while 3G Capital and BRK.A will hold about 25% each!

* The “Oracle of Omaha” is not often a target of big-time, credible criticism. However, on this deal he has been labeled as a hypocrite by a number of his bolder critics… for the following reasons:

- Buffett has often criticized Private Equity companies and the “PE industry” for their use of leverage and their short-term hold times[9];

- There is no way that anyone can deny that 3G Capital is a major player in the PE space:

- 3G has used leverage in the Burger King, Tim Hortons, and Heinz transactions;

- 3G grew Anheuser-Busch InBev(ABI) into a global power across three continents through leverage – with the company’s debt growing from $5 billion in 2005 to the current $50 billion.

- The cost structure for holders of 3G (annual fees and incentive awards for management) is typical of the PE space – 2/20%.

- And in the lexicon of the PE industry, the term “synergies” almost always means the (significant) reduction of head count (ie. job-cutting).

- All of that being said, this is the third big deal Buffett has entered into with 3G.

- In these deals, Buffett provides a huge pot of cash for the transaction and gains an equity stake in the new entity…

- While 3G Capital provides the acquisition acumen, more capital (an/or stock), loans, and the executives who will complete the deal and provide ongoing operational leadership.

* It is my opinion that these joint BRK.A/3G deals have been driven by the following factors:

- Buffett has created such an incredibly effective cash flow machine in the form of BRK.A that he cannot find enough attractive ways to put that growing pile of cash to work on his own!

- He has grown to respect and (more importantly) trust Jorge Paulo Lemann as a worthy and valued business partner.

- Buffett and Lemann share an affinity toward iconic consumer brands.

- And I believe that Buffett has extracted assurances from Lemann that 3G is not a corporate “flipper”… but is in these acquisitions for the “long haul” (albeit not likely quite as long as Buffett’s definition of the term, which he has suggested means “forever”).

- You’ll notice that Buffett has been placing less importance on his stock portfolio and more emphasis on ongoing companies with a strong brand… this deal continues in that vein.

- But likely the biggest factor driving these deals has been the Bernanke/Yellen “free money” policy[10]!

- As we reported above, KRFT incurred a huge debt load in its divestiture of Mondelez. That debt is about $9 billion – but on an after tax basis only costs KRFT about 3% annually!!

- 3G Capital loaded Heinz up with lots of debt as it did with ABI.

- And even conservative Mr. Buffett has allowed his corporate empire to increase its debt load over the past ten years from $14 billion to $80 billion.

- After all, “dirt cheap money” is hard to resist!!

Let’s wrap up our story by a quick review of the option trades I described at the very beginning.

Recall that the first trader put up $160,000 on March 10th, counting on KRFT to climb up to at least $62.90 by March 20th … just to break even on the trade! If you scan the prices of KRFT between March 10th and March 20th, you can see that the “Daily High” never reached or exceeded $62.90.

I confess to not knowing if this trader sold at $62.50… or “rolled” his position out before expiration… or just “ate” his loss. However, we can see that his time/price expectation missed by some 5 days!!

On the other hand, the second trader who bought June $67.50 Calls (laying out $700,000 for those options) was more than handsomely rewarded… since KRFT reached as high as $91.32 on April 2nd!! Perhaps that trader celebrated by breaking out a special bottle of some Brazilian wine (in honor of Lemann and 3G).

Of course, it is not impossible that either or both of those traders had gotten “wind” of the whirlwind talks between 3G and KRFT (that evidently began at the end of February). In that event, the first trader was just a bit too optimistic regarding the timing of an actual announcement of the merger!

When you buy an option, being "right" on direction but "wrong" on TIME is certain to cause you Excedrin Headache #107!

INVESTOR TAKEAWAY

What do I think an investor can “take away” from this story? These are the points that strike me as most salient:

1) Consider this irony:

a) On the one hand, we have the sage, proven, tested, conservative, professor-like Warren Buffett … a grandfatherly figure who regularly touts the timeless dependability of the American economy, American ingenuity, and American entrepreneurial energy… and who applauds the importance of hard work and dedication …

In addition, Buffett has roundly criticized the Private Equity space for its use of leverage and its short-term orientation (“rollups”… or what I call “flipping”)… in sharp contrast to Buffett’s understanding of “long-term” (ie. “forever”).

b) On the other hand we have the flashy, athletic, international billionaire, Jorge Paulo Lemann,

Jorge Paulo Lemann -- of Swiss/Brazilian descent... and the 26th richest man in the world.

a founder of 3G Capital (with offices in Brazil and New York) … practically the very definition of the current day Private Equity kingpin – transforming the long-time U.S. iconic brand of Anheuser-Busch (Budweiser, Michelob, the famous Clydesdale horses, etc.) into an international beer/spirits powerhouse

The famous Budweiser Clydesdale Horses!

… taking the H.J. Heinz Company private with tons of debt…. etc.

c) Now we see that a powerful partnership has formed between Buffett and Lemann… they obviously trust one another as much as any two billionaire entrepreneurs can trust anyone!!

At least one observer has suggested this intriguing notion –

What if Buffett has made quiet arrangements with Lemann to have a role within BRK.A following Buffett’s death? After all, what BRK.A will lack upon Buffett’s death is an experienced, proven leader with international credentials and credibility as well as a intellectual capacity and personal vision broad enough to encompass and manage a corporate empire as expansive as BRK.A.

It is worth noting that another Private Equity icon (and egotist) Bill Ackman, has joined with 3G Capital by owning a part of the Burger King/Tim Horton’s entity (QSR Brands International). Ackman has taken other steps to become more like 3G … in the sense that his strategy has shifted toward taking over companies through management (rather than just focusing upon stock ownership).

And for his part, Buffett has defended 3G Capital (and his partnership) by saying this in a recent interview:

“they’re not buying things to sell. I don’t think it’s even proper to call them a private equity firm exactly because they’re buying to keep just like we’re buying to keep.”

2) Buying options is a tricky endeavor! As we saw above, two traders came up with a correct trading “thesis”… that is, something was about to occur that would drive KRFT stock higher! However, only one of those traders got the “timing” correct – that trader went out to the June expiration in order to give his thesis enough time to come to fruition! The other trader fell five days short of the correct timing!! Ooops!! So when you buy options, be sure you are clear that you can live with the risk of being wrong on either “Price” or “Time”! And of course, never ever (never, ever) put more money at risk than you can afford to lose!!!

3) Will this merger of KRFT and Heinz work out? Only time will tell. But I can offer some basic facts that might help you take an educated guess:

CHALLENGES:

1) Since 1980, KRFT has been through seven mergers or divestitures…. Including being owned by tobacco company Philip Morris between 1988 and 2007!

2) As reported above, this merger hinges on Kraft brands leveraging Heinz’s international network to significantly increase global sales. Alas, that is not a new strategy. In 2004, KRFT inaugurated a huge “One Company” initiative – with the goal of creating a huge and globally integrated firm (with a reduced cost structure). The plan was so unsuccessful that by 2011 it changed direction – opting to create a more agile domestic business.

3) Valuation.

a) Just months ago, KRFT was at $55/share. That was 31 times its then $1.75/share of Net Income.

b) Now, at $86.50, KRFT sits at over 49 times its Net Income.

c) If you divide the KRFT price by its Free Cash Flow, you find it sits at 21 times its FCF!!

d) That means that KRFT is an awfully expensive consumer discretionary stock … especially one that has been stuck in a mature, slow/no growth “rut” lately!

REASONS FOR HOPE:

1) 3G Capital leaders are proven taskmasters:

a) They are zealots regarding “Zero Based Budgeting” – ie. every dollar of expense is questioned every year – from corporate jet costs to supply closet inventory.

b) They have already jacked up the gross operating margins at Heinz by 8% since taking over.

2) Citigroup (C) estimates that Kraft Heinz will earn as much as $8 billion a year in EBITDA by 2017 (or whenever the promise “synergies” kick in). At that level, the Enterprise Value would be $100 billion. Assuming that $100 billion level, KRFT stock would be valued at $82.62/share – much higher than pre-March 25th (but lower than the current $86.50).

3) The co-portfolio manager at Westchester Capital Management Merger Fund (Roy Behren) is quoted by Forbes as seeing positives in the merger:

a) “It is a value-creating transaction for Kraft shareholders.”

b) “This is a way for 3G Capital to now have a publicly traded vehicle where it can have stock to use for future acquisitions. Kraft Heinz will have the option of doing cash or stock deals going forward.”

4) And finally, from the Oracle himself comes this heartfelt opinion:

“There will be plenty of people that want to eat other things. But there are plenty of people that want to eat the products that Kraft/Heinz turns out. And there are new products coming all the time. At Heinz, we have at least four new products that we will be hitting the shelves with this year. So it’s not a static operation at all. And we’ve got a management that I’m willing to bet a lot of money on. Matter of fact, just on the common stock, I bet 9.5 billion and then we have 8 billion of preferred.”

DISCLOSURE:

The author does not own KRFT stock or options. He is not a limited partner in 3G Capital. He does not own BRK.A. His phone number is not counted among the numbers that either Warren Buffett or Jorge Paulo Lemann have on “speed dial”. However, he has been known to be a fan of Mac and Cheese, Heinz Relish, Heinz Sweet Pickles, Heinz Ketchup, etc.

FOOTNOTES:

[1] As we know, that “great company at bargain price” is the oft-quoted rubric used to describe an ideal “Buffett buyout” candidate!

[2] 3G Capital Partners has acquired Burger King (BKW) (2010), purchased H.J. Heinz (partnering with BRK.A) (2013), and acquired Tim Hortons (partnering with BRK.A) (2014).

[3] ABI is a multinational beverage and brewing company headquartered in Leuven, Belgium. It is the world's largest brewer and has a 25 percent global market share

[4] Behring is a founding partner of 3G Capital and the current Chair at Heinz.

[5] Or as I would put it in ancient war terminology, how the “spoils” would be divided among the players.

[6] Being an innate skeptic, I wonder what the “over-under” on the number of quarters it will take before the new company consolidates into one location. The cost of two headquarters with regard to head count and leasing overhead is considerable.

[7] Obviously a reference to the fact that everyone knows KRFT and Heinz are already loaded with debt!

[8] In case you don’t know, that is astounding.

[9] To borrow from real estate terminology, PE companies often “flip” companies.

[10] OK, I admit that money is not literally “free”… but on a historical basis, it is dirt-cheap!

Related Posts

If You'd Invested $1,000 in Shopify Stock 10 Years Ago, Here's How Much You'd Have Today

If You'd Invested $1,000 in Shopify Stock 10 Years Ago, Here's How Much You'd Have Today

Also on Market Tamer…

Follow Us on Facebook