In our previous article (see: https://www.markettamer.com/blog/sharpen-your-analysis-of-ibb-xbi-and-fbt) we took a look at the Year-to-Date (YTD) performance record of three unnamed ETFs and discussed which of those investment choices had been the “best” one for that period. It soon became apparent that performance data alone is totally inadequate as a comparative measure among ETFs, funds, or portfolios[1]with regard to anything except the single dimension revealed by that metric – return performance! It would be naïve (and foolish) to attach any adjective (“best”, “most appropriate”, etc.) to any ETF without having a larger range of information available through which to more thoroughly analyze and compare any given ETF with other available investment choices.

As we discussed what types of information would be helpful in any such investment analysis – the concept of “Relative Risk” emerged.

There are numerous metrics available that enable investors to assess Relative Risk.

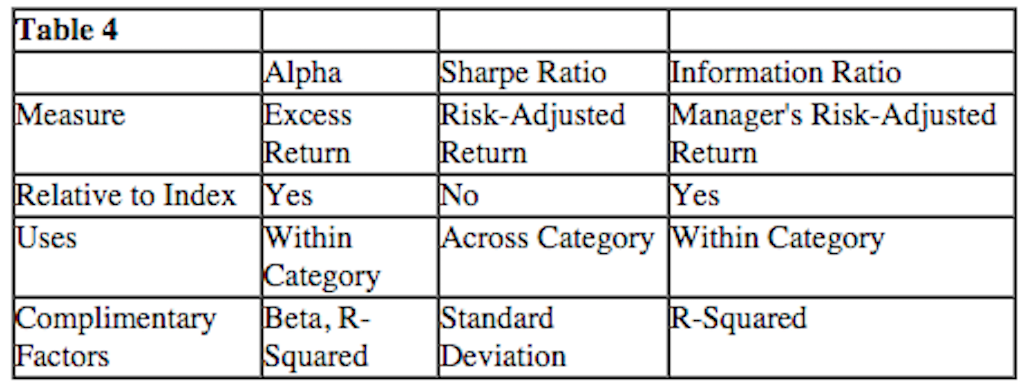

Therefore, we explored at some length the first performance metric that isolates excess return per unit of total risk assumed through any given investment. The developer of this metric was William Sharpe; he introduced the formula in 1966[2]. It soon became popularly referred to as the “Sharpe Ratio”, and It has become the “industry standard” for measuring risk-adjusted return. Among the many things we gleaned from our review of the Sharpe Ratio were the following:

1) The ratio compares actual investment performance (“Return”) vis-à-vis a “Risk-Free Rate” (Rf) … and then divides that numerator by the Standard Deviation of the investment return of the ETF being analyzed;

2) The higher the Sharpe Ratio is [with some exceptions as indicated] for any given ETF, the better the “Risk-Adjusted Return” (RAR) is for that ETF vis-à-vis other ETFs with a lower Sharpe Ratio.

3) If two ETFs have garnered exactly the same return for any given period… but one ETF has a higher Standard Deviation (StdDev) than the other… the ETF with the lower StdDev will have a higher Sharpe Ratio – and therefore offer a better RAR!

It would be difficult to argue that Sharpe’s formula has not greatly enhanced the ability of the average investor to objectively analyze and evaluate different ETFs. However, the most astute among you will properly point out that the Sharpe Ratio only measures the return of the ETF vis-à-vis a Risk-Free Rate (Rf). It would seem intuitively obvious that an even more helpful metric would be one that compares ETFs vis-à-vis the benchmark used within the asset category that reflects the ETFs stated investment strategy and style, such as any of the following (this list is suggestive, not exhaustive):

U.S. Large Cap Growth

U.S. Large Cap Value

U.S. Large Cap Blend

U.S. Mid-Cap Growth

U.S. Small-Cap Growth

U.S. HealthCare Sector

Global HealthCare Sector

Commodities Index

International Large Cap Growth

Emerging Markets Growth

Therefore, we are going to focus here upon how we can arrive at a formula that measures performance and risk relative to any given investment strategy/style (most commonly by referencing the performance of a particular “Index”).

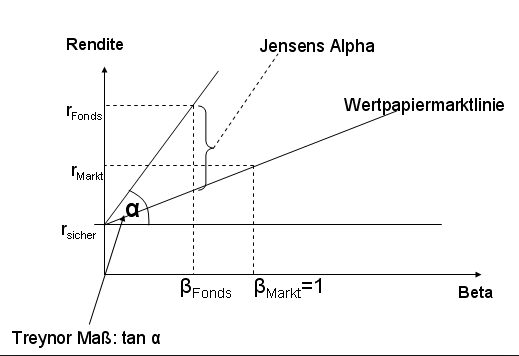

Since we are focusing upon “Risk” as well as “Return”, let’s focus on Risk first. One especially popular (and basic) metric within investment analysis is “Beta” – the quantification of the volatility of a security or portfolio relative to “the market as a whole”. Think of Beta as an ETF’s tendency to move up or down in tandem with “the Market”. If an ETF benchmarked against the S&P 500 Index has been 20% more volatile than that index during any given period – it has a Beta of 1.20! If on the other hand, the price action of that ETF has been 20% less volatile than the index, it will have a Beta of 0.80. Note that the mathematical consequence of this definition is that one should expect an investment with a Beta above 1.0 to outperform its index during bull market moves[3]!

With regard to the “Return” dimension of any given ETF that is benchmarked to an index, we can intuitively presume that, for any given time period, the ETF manager will have either matched the return of the index, outperformed the index, or underperformed the index. The difference between an ETF’s performance and the return of the corresponding index is referred to as “Alpha”. Positive “Alpha” is good; however, the opposite is not an encouraging sign when reviewing an ETF. If you watch (or listen to) CNBC, Fox Business, or Bloomberg TV a good deal, you’ll hear guests quite frequently refer to “Alpha”[4]. Simply put, when any given portfolio manager generates an Alpha above zero, she/he has “created value”; if that manager has generated an Alpha below zero, “value has been eliminated”.

For any given period, Alpha can be considered a reflection of a manager’s portfolio management skill – including the ability to pick great securities; the ability to assess the most promising sector allocations; the ability to allocate optimally among countries (for international, global, and emerging market funds); and/or the ability to sense swings in the market. Over short periods of time, of course, Alpha may merely reflect good fortune. However, over longer periods of time, Alpha can be (generally) counted upon as a helpful measure of a manager’s investment acumen and discipline.

Of course, the matching of any particular ETF with the appropriate benchmark index is crucial! Let me illustrate by referencing a simple analysis from the Advisors Perspectiveswebsite:

(http://www.advisorperspectives.com/newsletters07/newsltr25-1.html ):

Assume you want to analyze the 3-year performance of a particular growth fund.

If you rush into that analysis by plugging in benchmark data from the S&P 500 Index, you end up with an Alpha calculation that shows the following:

Fund Beta: 1.53 (more volatile than index)

Fund Alpha: -2.86 (under performs)

However, if you first ensure that you draw data from the appropriate index, you discover that this growth fund is a small-cap growth fund. Therefore, the S&P 500 is not the proper index to use in calculating metrics for this fund. Instead, one must use the Russell 2000 Growth Index… from which you end up with a totally different view:

Fund Beta: 0.80 (less volatile than index)

Fund Alpha: 2.36 (outperforms)

In other words, Alpha is a relative measure, largely dependent upon the index that is utilized as the “Benchmark”. Therefore, it is essential that the most appropriate index be selected for comparison purposes.

Now we have two additional measures through which to analyze an ETF – Beta (risk; volatility) and Alpha (manager performance relative to an appropriate benchmark). When we add in the Sharpe Ratio, we now have a helpful group of Return/Risk parameters.

However, these alone will not get us to where we need to be with regard to a more comprehensive analytical system! For example, although Alpha does measure performance relative to a given benchmark… it absolutely does not take into consideration the particular risk associated with the asset group reflected by that benchmark.

Let me illustrate as simply as I can, drawing upon the example of the Deutsche X-Trackers Harvest CSI 500 China ETF (ASHS) which was extensively reviewed in our previous article. No matter how much Alpha ASHS may have generated between January and August, that metric alone should never be used as a tool through which to compare (for example) ASHS with the iShares China Large-Cap ETF (FXI) or with any U.S.-based ETF. As we saw up close in the prior article, the risks involved with ASHS are substantial – much higher than the risk involved in large cap China shares traded through the Hong Kong Exchange. ASHS invests in small-cap “A-Shares” traded in Mainland China – where so much turmoil has made huge headlines—while FXI trades large-cap stocks tied to the Hong Kong exchange not traded on the Chinese mainland. Almost all experts concur that small-cap A-Shares have been the most over valued equities in China over the past year. And neither segment of the Chinese market can be helpfully compared with any U.S. focused ETF stock without adjusting adequately for the highly divergent risks involved in each market!

The Sharpe Ratio, for its part, does an exceptional job of calculating an “overall” risk-adjusted return…. but does not offer any distinction between the “source” of any two (or more) particular ETF’s risk. The Sharpe Ratio utilizes only the Risk Free Rate to calculate “excess return” – and therefore does not separate related risk into both an “Alpha” component and a “Beta” component. If your eyes just glazed over, let me offer a simple example. Assume the following about Fund 1 and Fund 2:

Fund 1 Return: 8.13

Fund 1 Std Deviation: 11.60

Fund 2 Return: 14.13

Fund 2 Std Deviation: 24.30

For the period under review, the Risk Free Rate for the Sharpe Ratio calculation is 2.5%.

Therefore, the Sharpe Ratio calculation results in these metrics:

Fund 1 Sharpe Ratio: 0.4853

Fund 2 Sharpe Ratio: 0.5066

On the surface, you can see that Fund 2 offers a bit better “Risk-Adjusted Return” (RAR) than Fund 1. But in this case the Sharpe Ratio could potentially be quite misleading! Can you see why?

Yes, the risk associated with the extra 6.68% return generated by Fund 2 is significantly higher than the risk associated with Fund 1!! The truth is that most of the investors I know would prefer the slightly lower RAR of Fund 1 in order to sidestep the much higher volatility of Fund 2.

If we tear apart the Sharpe Ratio equation, we will see that the above example can be explained by virtue of the fact that, although the denominator in the Sharpe Ratio does incorporate Standard Deviation (volatility/risk), it makes absolutely no distinction between upside risk and downside risk!

How can we create a helpful measure that can offer us additional information — information offering a distinction between upside and downside risk? A solution can be found in the Information Ratio. The “Information Ratio” is a variation and enhancement of the Sharpe Ratio. It also measures “excess return per unit of risk”; however, the enhancement over and above Sharpe is that the Information Ratio measures excess return and risk relative to a particular index benchmark! Viewing the Information Ratio mathematically, it is:

[Annualized Asset Return] – [Annualized Benchmark Index Return]

[Annualized Standard Deviation of the Excess Return]

Put narratively, the Information Ratio compares any given manager’s excess return over the designated benchmark … with the additional (non-market) risk that was required to earn that extra return. Note that (as with the Sharpe Ratio) a higher Information Ratio indicates a better risk-adjusted return.

To illustrate, let’s assume that Manager A and Manager B each run an active (rather than passive) portfolio that is benchmarked to the S&P 500 Index. For the past two years, Manager A has outperformed the index by 15%, while Manager B has also outperformed – but only by 9%. However, in the process of outperforming the index over those two years, Manager A was invested in some securities that were significantly more volatile than either the index or the portfolio run by Manager B. Therefore, while the Sharpe Ratio for Manager A during that period could be higher than that of Manager B, the Information Ratio for each fund during that period is likely to reveal that Manager B outperformed Manager A vis-à-vis the lower risk that Manager B incurred to outperform the index!

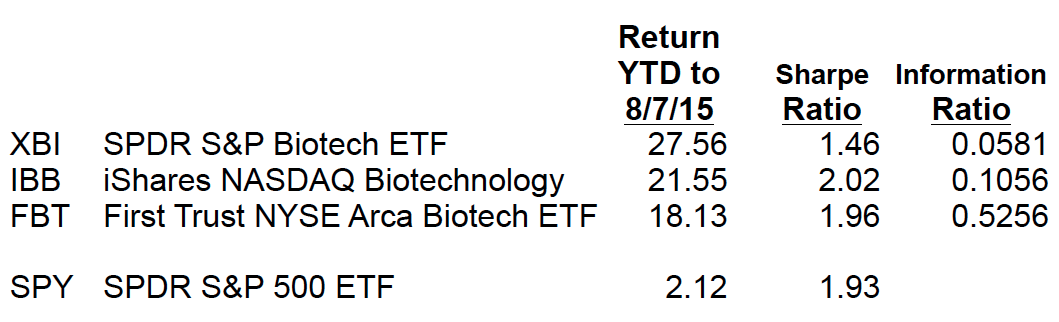

Borrowing once again from the website referred to earlier[5], here is a helpful illustration of key dimensions related to concepts we have been highlighting for you:  Let’s put more “flesh” to this Information Ratio metric. Based on data available through http://www.macroaxis.com/ , I have added Information Ratio metrics to the table in which we reported (in the prior article) key metrics for three Biotech ETFs:

Let’s put more “flesh” to this Information Ratio metric. Based on data available through http://www.macroaxis.com/ , I have added Information Ratio metrics to the table in which we reported (in the prior article) key metrics for three Biotech ETFs:  This table is interesting. It certainly illustrates the importance of making sure we understand the key dimensions and distinctions related to the Sharpe Ratio, Information Ratio, and Alpha as presented in the table above (from Advisor Perspectives).

This table is interesting. It certainly illustrates the importance of making sure we understand the key dimensions and distinctions related to the Sharpe Ratio, Information Ratio, and Alpha as presented in the table above (from Advisor Perspectives).

Recall that we tentatively concluded earlier that IBB demonstrated a better Risk-Adjusted Return (RAR) than XBI or FBT – but that was based only on the Sharpe Ratio. Here we can see that, relative to their given benchmark, FBT demonstrates the best RAR during the YTD period. For many investors, this will be key information that will impact their investment choice going forward.

Before we wrap up this discussion of the Information Ratio, Alpha, and Beta, I must point out that one especially interesting application of the Information Ratio is to help any given investor or analyst get a handle on the relative virtues of “Active” versus “Passive” investing. Those who regularly peruse publications within the investment analysis, financial advisor, financial professional spaces (including such popular publications as Money, Smart Investing, Personal Finance, etc.) are very familiar with how frequently articles are published that variously assert that “Active Management” of portfolios is superior or that “Passive Management” of portfolios is the best choice. Frequently, the advocates of “Passive” tout the many times Warren Buffett has spoken quite approvingly of John Bogle and the Vanguard Group’s index investing approach (which is “Passive”). And inevitably, those who tout “Active” focus on the Alpha of key “star managers”, as well as the fact that there is still a higher amount of investor dollars committed to Active than Passive funds.

The point here is that if a portfolio manager cannot generate a return equal to or greater than her/his related benchmark index – then there is absolutely no point in paying that manager to manage the assets in that fund. It would be more effective to merely invest in the index itself! In fact, if net of all related annual expenses, an active manager cannot outperform the related index (relative to a comparable index fund’s performance after fees) then “Marginal Utility” itself should drive investors to choose the index fund!![6]

Let’s take a look at two huge “Large Cap Growth” funds:

American Funds Growth Fund of America (RGAAX) $147.5 billion

Fidelity Contrafund (FCNTX) $113.3 billion

I refer to these two funds only because they are among the biggest actively managed funds in the United States. They also reflect two entirely different streams of “Active Management”.

With regard to “Active Management”, it is germane to highlight one of the “Legends” of Wall Street whose record of active portfolio management is so astounding that it has grown to nearly mythic proportions in the years since his 1990 retirement.

The legendary Peter Lynch -- a prototype of the "Star Active Manager".

I am speaking of course of Peter Lynch, who assumed portfolio management in 1977 of a little known, unheralded mutual fund named Fidelity Magellan, which consisted of just $18 million under management. Between then and his retirement, Lynch grew Magellan at a compounded annual average return rate of 29.2%! A thousand dollar initial investment in Magellan in 1977 would have been worth over $28,000 when he handed on the reins of Magellan to his successor. When Lynch left, the fund had $19 billion in assets under management (a small sum by today’s standards… but a giant amount back in his day!).

Lynch generated so much attention, so many headlines, and so much media coverage that his aura lent credibility to the notion that someone with special insights and skill could “beat the Market” – and do so consistently.

As we all know, a number of other managers carried on that tradition after Lynch retired – including names such as William Miller:

William Miller was once a shining star with an amazing record

(Legg Mason Value Trust outperformed the S&P 500 Index during every year between 1991 and 2005… a feat unmatched by anyone else; he was named “Mutual Fund Manager of the Decade” in 1999). Of course, we also have William Gross (co-founder of Pimco, who grew the organization from nothing into a $2 trillion money management behemoth; Morningstar named him “Fixed-Income Manager of the Decade” in January of 2010, after he posted an annual average return of 7.7% versus his benchmark of 5.5%.

Bond icon Willliam Gross.

Gross became so unparalleled in bond management that he was most often referred to as the “Bond King”; for years he managed the world’s biggest fund, Pimco Total Return Fund, with $292.9 billion in assets under management at its zenith in April of 2013).

Anyone listing “Star Managers” would be criminally remiss if Warren Buffett's name was omitted.

The ultra-legendary Warren Buffett.

Buffett is the legendary genius behind the conglomerate we know as Berkshire Hathaway (BRK.A); the Oracle of Omaha; the Wizard of Wall Street. So iconic is Buffett that his name is included within the title of hundreds of thousands of published financial articles and email messages — because the author wants to grab “eyeballs”[7]).

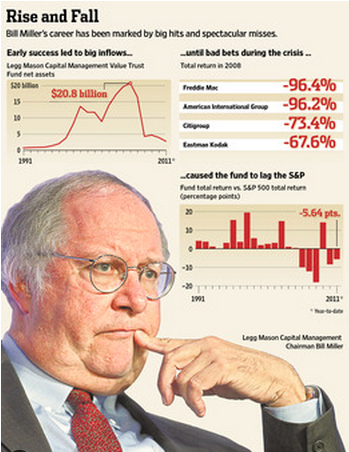

The sad fact is that being a “Super Manager” is an extremely challenging feat to pull off over long periods of time. Most “managers of the year” reflect all too fleeting success. And two out of the four “Stars” mentioned above (from Lynch through Buffett) have (tragically) crashed and burned. Bill Miller crashed and burned during the Financial Crisis[8];

This 2011 illustration comes from the Wall Street Journal.

and Bill Gross crashed at PIMCO (but moved over to Janus Unconstrained Bond Fund) in October of 2014.[9] [For more details on Gross, see https://www.markettamer.com/blog/bond-king-gross-jumps-ship-to-janus).

As an aside, the analytical literature on the persistency of outstanding Information Ratio metrics is still evolving … but it appears more and more likely that only extraordinary managers can average an Information Ratio over 0.50 over long periods of time.

It is interesting to see how, especially since the 2007-2009 Financial Crisis, funds and ETFs have appeared to de-emphasize “Star Managers” in their marketing strategy. In fact, that has been particularly true since the implosion of both Miller and Gross from the heights of active portfolio management!

Jeffrey Gundlach

As one reviews current marketing material, although there are still a number of “mini-stars” out there within the investing world [Jeffrey Gundlach (the new “bond king”) of Doubleline Capital being one of them] most funds are marketing today without trying to transform the fund manager into some super human being. Of course, no manager at Fidelity Funds has come close to unseating (much less matching) the record of Peter Lynch as a master equity portfolio manager[10]. However, if the measure of one’s management success is brought closer to an achievable, “real-world” standard, then the manager of Fidelity’s Contrafund (FCNTX), Will Danoff, could be considered an exceptional success.

Will Danoff strikes me as the type of manager I'd really like as a person. First, he has a sense of humor (unusual for a manager to be pictured laughing). Second, if you compare the earliest photos of Will with current photos, it is obvious that he hates ties (like I do). And thirdly, he works extremely hard for someone as accomplished as he is.

In September of this year, Danoff will celebrate his 25th years as manager of the Contrafund – a seniority (or longevity) record that is becoming rarer each year. During his “watch”, Contrafund has generated a average annualized gain of 13.3% (through 6/30/15)—beating the S&P 500 Index (10.1%) and the Morningstar Large-Growth Category average (9.6%).

Danoff focuses on finding stocks based on good business models and improving earnings potential… with particular emphasis upon quality management. Little wonder then that among his long-standing portfolio positions are BRK.A and Google (GOOG)[11]. More than 25% of his portfolio assets are committed to the technology space, and interestingly, he holds small positions in some privately held tech concerns such as Uber, Pinterest, and Airbnb.

Particularly relevant with the S&P 500 at its current, historically lofty levels, Danoff’s 25 years at the helm have taught him the vagaries of bull markets. He has outperformed his fund peers (and the Russell 1000 Growth Index) during two major bear markets (aka “crashes”) – including the Dot.com Crash and the Financial Crisis.

Finally, Contrafund has a fund expense formula that is shareholder-friendly because it lowers annual fund expense whenever Contrafund’s average three-year return underperforms its benchmark and increases fund expense only when and if that three-year average outperforms its benchmark!!

In sharp contrast to Fidelity’s heritage from Peter Lynch (of the “Star” manager), the American Funds group has focused upon multi-manager portfolio management. There are no “single Stars” within the American Funds’ system. American Funds Growth Fund of America (RGAAX) is a behemoth among equity funds, and is spread out across 461 different securities – with 80% of its holdings consisting of U.S. stocks[12]. The fund’s top sectors are consumer cyclical, technology, and healthcare. Amazon (AMZN), Gilead Sciences (GILD), and Comcast (CMCSA) are its top three holdings. The fund has averaged an annual return of 16.49% over the past five years … and 8.38% during the past decade.

Given that these two giant funds are certainly time-tested, well-managed, and charge similar annual expenses, how might one choose the fund that best fits his/her financial and investment needs?

As we have learned above, we could review the Information Ratio for each fund. That will give us a measure regarding the amount of excess return garnered by each fund, adjusted for the risk taken by their respective fund manages (in order to garner that return).  As you can see, Contrafund reports a higher Information Ratio than the Growth Fund of America. For many investors, that comparative metric might prove sufficient to lead one to choose Contrafund is a better choice fund choice for them at this point. In this fashion, the Information Ratio provides investors with a solid analytical tool that is objective and adjusts the return actually received by ETFs/funds for the risk that was taken to earn the return!

As you can see, Contrafund reports a higher Information Ratio than the Growth Fund of America. For many investors, that comparative metric might prove sufficient to lead one to choose Contrafund is a better choice fund choice for them at this point. In this fashion, the Information Ratio provides investors with a solid analytical tool that is objective and adjusts the return actually received by ETFs/funds for the risk that was taken to earn the return!

INVESTOR TAKEAWAY: As we have been witnessing first-hand this year, and particularly during the week I completed this article (August 10-14), the stock market itself has a significant level of inherent risk to which investors are exposed on a daily basis. Here is a graph of price action on the S&P 500 Index and Apple (AAPL) between Friday, August 7th and 2:15 PM on Wednesday, August 12th.

This graph illustrates market volatility between August 7th and 12th.

Due to the currency devaluation announced by Beijing on Tuesday (8/11), the Index went from 2104.18 at Monday’s Close (following a large rally during market hours) down to 2,084.07 (falling about 1%). During those three days, market stalwart (and/or behemoth) AAPL was up by as much as 5%… and then down by over 3.5%.[13]

That makes for a lot of movement (Volatility) during an otherwise traditionally slow August trading week. And for those with options positions, that Volatility (Risk) can rear its more ugly head by quickly moving a trader’s Daily P/L total into the red[14].

Therefore, since investors must cope with “Market Risk” as a cost of doing business in the equity space, it seems self-evident that every investor should want to minimize security-specific risk through the use of every tool available. In that light, I hope you now have a great handle on key investment analysis concepts such as Alpha, Beta, the Sharpe Ratio, and the Information Ratio.

If you begin to apply these tools on a regular basis to guide you in your security selection, you should grow increasingly adept at lowering your stock specific risk, and therefore lower your overall investment risk.

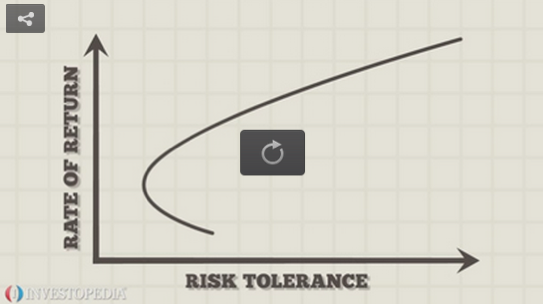

It should not be surprising that these tools can be applied in the construction of an “optimized” portfolio … a process that involves the concept of the “Efficient Frontier”. Here is a link to a brief streaming video (and narrative) from Investopedia.com explicating the “Efficient Frontier” (the video is two-thirds of the way down from the top of the screen): http://www.investopedia.com/terms/e/efficientfrontier.asp .

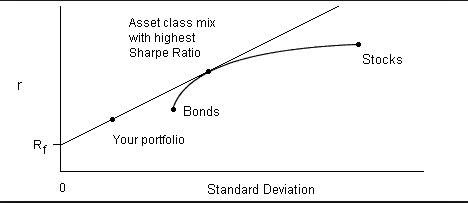

Here is an image showing how the Sharpe Ratio fits into the Efficient Frontier concept:

All of the above being said, may I suggest that (unless you are a mathematician or you really getting excited by intricate formulas) you will be much better off not letting yourself get bogged down by delving too deeply into the myriad additional analytical concepts and frameworks that have developed since the Sharpe Ratio was first introduced (here are just a few of them):[15]

For the curious reader: "Rendite" is German for "Yield". The long name to the far right is a German word related to the "Capital Asset Pricing Model".

I will hope (for you and for me) that we become so proficient at assessing the Return/Risk parameters of our trades and investments that we will (sooner than later) become weighed down by the resulting profits rolling into our account!

DISCLOSURE: The author does own VOO and owns option positions in SPY. He also owns biotechnology much funds, but not the ETFs. His wife owns Fidelity Contrafund. Nothing in this article is intended as a recommendation to buy or sell anything. Always consult with your financial advisor regarding changes in your portfolio – either subtractions or additions.

FOOTNOTES:

Related Posts

3 Space Stocks to Buy With $1,000 and Hold Forever

3 Space Stocks to Buy With $1,000 and Hold Forever

Also on Market Tamer…

Follow Us on Facebook