Is the Market Over-Valued, Fairly-Valued, or Under-Valued. Many are indecisive about the answer!

I was thinking the other day about the wonders of our advanced scientific/technological world. Just think about the amazing things we have achieved:

1) Landed humans on the Moon, and brought them back to earth;

2) Through “Nano Technology”, developed little machines that can move within the human body to do such things as assist in medical diagnosis and deliver medical therapy;

3) Developed Artificial Intelligence capable of independent thought;

Artificial Intelligence... computers developing the capacity for independent thought

4) Developed Aerial Surveillance Technology so sophisticated that it can capture incredibly detailed close-up human images (eg. drone images) or a much broader, more comprehensive image over a wide territory (through Wide Area Airborne Surveillance (WAAS);

In fact, we experienced these amazing new developments just last year:

1) It was revealed that a pioneering surgical procedure restored functioning of a severed spinal cord (Doctors repaired the spinal tear that left a man paralyzed from the chest down with nerve tissues from his ankle; within five months, feeling was restored; within two years, the man could walk.)

2) A human space probe (size of a refrigerator) was successfully drilled into the surface of a 4.5 billion year old comet that was 311 million miles away from Earth! (The probe belonged to the European Space Agency).

Here is an image of the Philae Lander (transported by the Rosetta Spacecraft) on an ancient, far-away comet!

3) Doctors at St. Vincent's Hospital in Sydney revived a human heart that had stopped beating – thereby preventing muscle deterioration and allowing the heart to be used in a transplant (Accomplished by bathing the heart in warm, oxygenated blood and other nutrients. Similar methods have been used to treat livers, lungs, and kidneys before transplantation.

Given all of this human progress… wouldn’t one reasonably expect that within this mega scientific world of ours, someone could conclusively determine if the U.S. stock market is over-valued, fairly-valued, or under-valued??!!

Therefore, I embarked on a journey of discovery to find the definitive, authoritative answer regarding this burning question.

Of course, being the type of analyst who expects that the best answer will emerge from the most informed, best educated, most experienced authority… I turned to a veteran economic analyst who not only has a PhD, but also has access to the most extensive, most comprehensive, most current range of economic data on the face of the Earth: U.S. Federal Reserve Chair, Dr. Janet Yellen. [It doesn’t hurt that (figuratively speaking) she “has her finger on the monetary button”!

U.S. Federal Reserve Chair, Janet Yellen

In early May, Yellen engaged in a dialogue with IMF Managing Director, Christine Lagarde, while speaking at the Institute for New Economic ThinkingConference (in Washington, D.C.).

IMF Managing Director, Christine Lagarde

Responding to a question from Lagarde about “Bubbles”[1] that might result from Quantitative Easing, Yellen said:

“I would highlight that equity-market valuations at this point generally are quite high…Not so high when you compare returns on equity to returns on safe assets like bonds, which are also very low, but there are potential dangers there.”

So there we have it!! That must be our answer. After all, who is in a position to question the most powerful woman on earth… with her impeccable credentials and her reputation as a Monetary Dove??[2]

What a minute… wait a minute! I can’t believe it. Someone is telling me that “Yellen is wrong”!! Take a look at this:

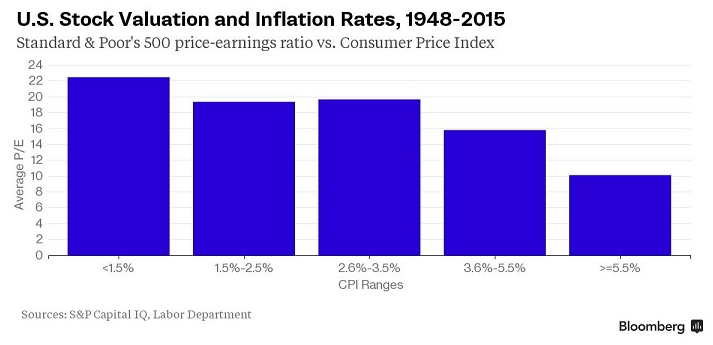

This chart was a key component in Stovall's analysis regarding Market Valuation.

This graph springs from the work of a second, often-quoted authority: Mr. Sam Stovall, who serves as the U.S. Equity Strategist at S&P Capital IQ!![3] Stovall’s response to Yellen’s comment was (paraphrasing in my words):

When one adjusts any market valuation for both low interest rates and low inflation rates, U.S. stocks are less costly than implied by Char Yellen.

Stovall’s chart visualizes the S&P 500 Index Price-Earnings Ratios (P/E)[4] since 1948. The data behind the graph matches up the P/E from each of those years with the Consumer Price Index (CPI) metric from that year. Then the P/E’s are grouped along a continuum of CPI metrics – from “under 1.5% CPI” up through “over 5% CPI”.

Referencing this chart, Stovall points out that when inflation has been less than 1.5% (recall that March 2015 CPI slid by 0.1% compared with March 2014!) the average P/E has been 22.5. (Note that when Stovall offered this rebuttal, the P/E stood at 21.3.)

So… the S&P 500 is not overvalued, correct?

Boy, that’s a relief!!!

But wait a minute now! I sense something rotten on Wall Street!! Just a couple of weeks ago, I remember seeing a piece about Stovall’s analysis of GAAP (Generally Accepted Accounting Principles) versus non-GAAP earnings! Let me see if I can find that!

Yes, I did find it… and that article came just 7 days before the above article (related to inflation)! Here is a summary of this contrasting analysis:

Stovall opined that stocks are highly valued … and then examined stock values from two vantage points:

1) Utilizing companies’ “Operating Earnings” (the favorite metric of those who prefer to “talk up” stocks on CNBC[5]) the S&P 500 is priced around 18 times trailing 12-month earnings. Compare that metric to the median P/E ratio of the S&P since 1988 (17.4) and you find only a slight “premium” of 3.4%.

2) Here is the “But”. If instead of “Operating Earnings” you use GAAP earnings to calculate the market’s P/E, you find that the S&P now stands at a 21.3 P/E!!

Even worse, the historical median (GAAP) P/E of the market is just (approximately) 16!! Therefore, the GAAP-based P/E metric now stands at a 33% premium!! [That’s what I call a real “gap”!]

Let me offer a quick observation about Mr. Stovall based on these seemingly conflicting “takes” on the “Market”. It would appear that he resembles the economists who surrounded President Harry Truman when he famously requested a one-armed economist because

[Truman] was very frustrated by the economists who regularly said: “On the one hand, this… [and] On the other hand, that”!

Let me pause here to explain to anyone reading this who lived (formerly) under the illusion (delusion) that “Earnings are Earnings are Earnings”. Alas, my friend, when it comes to Wall Street, nothing could be further from the truth!

“Back in the day”[6], “earnings” was a term much more narrowly defined than it is today. Back then, it was in everyone’s best interest to be able to count on certain “basics” as axiomatic. However, as the investment world evolved and Wall Street began to “innovate” within the financial space – a lot of axioms got questioned. And (to put it bluntly) many of the “axioms” that got in the way of higher Wall Street profits were “re-formed”[7].

Consider this case-in point – the Leveraged Buyouts (LBO) strategy that rose to prominence in the late 1980’s. Those LBO’s depended upon the acquiring company establishing that it had sufficient earnings to afford to “service” the debt it would assume through the financial structure of the buyout. Well, as you can imagine, using the traditional definition of “earnings” severely limited the number of companies that could “qualify” to enter into a juicy LBO![8] Far too many companies could not demonstrate adequate “earnings” to justify entering into a LBO.

Wall Street was not happy with that! This barrier to their profits was intolerable! But what could it do about it? Well, Wall Street decided to create a new category of “earnings”!!!! [9]

Earnings before Interest, Taxes, Depreciation and Amortization (EBITDA)

It was truly amazing how many companies suddenly “qualified” to engineer a LBO under this amazing new definition of “earnings”!! And that, my friend, is just one simple example of how Wall Street works its “magic”!

So, now we know there are “multiple” types of earnings. Let’s just focus (for now) on two of them:

GAAP Earnings: this calculation of earnings resembles the type of earnings that iconic Wall Street securities analysts such as Benjamin Graham and Warren Buffett have focused upon! Earnings calculated the “old-fashioned way.”

This is Dr. Benjamin Graham (The Intelligent Investor) -- best known as the mentor of Warren Buffett.

Non-GAAP Earnings or Operating Earnings: the best definition I have seen of this type of earnings is—

“Profits without all the bad stuff!”

This calculation of earnings excludes the subtraction (from Revenue) of “one-time charges” and “non-recurring” expenses. The effect is to add those numbers back into GAAP earnings. Obviously, this increases earnings and decreases a stock’s P/E!!

So now, since this topic has cropped up, let’s address whether the non-GAAP earnings metric (in and of itself) is deceptive, improper, or unethical. I took a long look at this issue and found that the most convincing position presented came from Marc Siegel, (ironically) a member of the Financial Accounting Standards Board (FASB), in an article titled “For the Investor: “The Use of Non-GAAP Metrics”.[10] In this very interesting piece, Siegel acknowledges:

“McKinsey & Company states that ‘many companies – including all of the 25 largest US-based non-financial companies—are increasingly reporting some form of non-GAAP earnings.’”

Then Siegel asks (on behalf of you and I):

“Does the prevalence of non-GAAP metrics necessarily dilute financial statement information?”

Here is the essence of Siegel’s answer:

“In my experience, the combination of non-GAAP data outside the financial statements with information residing within the audited financial statements is more impactful than either dataset on its own. The non-GAAP information in a company’s communications with investors often provides insights into how management views their performance.

“For public companies, this information is usually presented in an earnings release and is often coupled with a PowerPoint presentation and conference call to provide financial statement users with a picture of the organization’s financial position and performance.”

Therefore, non-GAAP metrics are not deceptive in and of themself. The real issue of deception arises whenever an analyst or expert (or broker or financial adviser) utilizes non-GAAP metrics during a presentation or interview without sufficient disclosure and transparency.

Now that you know that there are significant differences with regard to equity valuations (depending upon which definition of “earnings” is used in any given valuation) you should be better prepared to “hear” equity commentary with more clarity and real understanding!

Now let’s get back to our basic analysis regarding current Equity Valuation.

Since we have laid bare Wall Street’s ability to make you think about the “Market” in whatever terms it chooses at any given moment… let’s engage in some “Devil’s Advocacy”. Specifically, assume your name is “Sally” and I want to convince you that now is the time for you to start investing in my mutual fund, stock, or ETF.

“Now, Sally, I know that Petty has told you that the market is overvalued. But c’mon. What does he know?! He just writes about this stuff; but I am on the “front lines” of investing. I live and breathe it. Here is why Petty is wrong:

1) “When Petty talks “valuation”, he is referring to P/E ratios based on “past earnings”, and comparing those P/E’s to “historical” averages. That is misleading!

“The Market doesn’t “look backward”, Sally! Instead, it “looks forward”!!

2) Also, Sally… we live in a whole new and different world with a whole new kind of economy and with unprecedentedly low interest rates… and low inflation!”

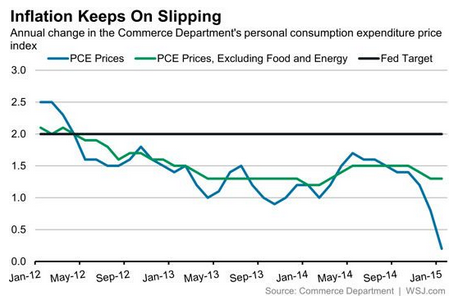

As just one demonstration of this, look at this graph of inflation metrics:

3) In addition, Petty neglected to inform you that the long-term “trend” in the P/E metric has changed. For example, since the year 1936, the S&P 500’s average P/E is 15.9. But consider the salient fact that, since 1988, the average P/E has been 22.1!!

3) In addition, Petty neglected to inform you that the long-term “trend” in the P/E metric has changed. For example, since the year 1936, the S&P 500’s average P/E is 15.9. But consider the salient fact that, since 1988, the average P/E has been 22.1!!

So in light of the above, Sally, what do you think? If you combine this “New Normal” with Forward-Looking Earnings on the S&P 500 Index– we have a P/E of just 17… with every reason to keep on expecting equity appreciation!! Why?

1) Because since 1988, the average P/E has been 22.1.

2) And also because there is nowhere else to put your money that is safer, more liquid, or more secure than U.S. Equities – especially in comparison with U.S. Treasury Securities that remain near historically low interest rates!! [END OF THIS IMAGINED PRESENTATION TO SALLY.]

The problem with which “Sally” has to wrestle is the fact that much of what the Wall Street representative said above is true. But it creates a narrative that is extremely misleading unless accompanied by proper disclaimers and counterpoints!! Proper disclaimers would include (but not be limited to):

1) No one can assure that any “Forward-Looking Earnings” estimate will be accurate. Consider “Forward-Looking” estimates that were surely made in mid-2008 (before Lehman Brothers went belly-up in mid-September). Talk about “bad” earnings estimates!!

2) Any term similar to “New Normal” holds the potential to mislead investors. Historically, “Bubble Periods” have occurred after commentators and experts have claimed that “this time is different” from any preceding period.

So “Sally” – don’t fall for that pitch!

I will be remiss if I don’t include the investment analysis framework of Yale Professor Robert Shiller in this article! So let’s take a look at Dr. Shiller.

Dr. Robert Shiller of Yale University

In the valuation metrics we have already described above, I am sure you have caught on to the trend changes and data discontinuity within the underlying data that makes adjusting for context appear to be both sensible and helpful. Even conservative analysts such as Benjamin Graham[11] recognized data discontinuities that cried out for adjustment – discontinuities which Graham attributed to the “boom/bust” business cycle.

This is the cover of Graham's classic investment tome in which he "adjusted" company metrics because of distortions resulting from the business cycle (ie. "boom" and "bust").

Therefore, Noble Economics Laureate Shiller developed an analytic framework within which the P/E Ratio fluctuations generated by big spikes in profit margins (up or down) would be smoothed out (eliminating distortion).

Not surprisingly, Shiller named his framework: the Cyclically Adjusted Price-Earnings (CAPE) Ratio. When commentators refer to this metric, they most commonly refer to it as the CAPE Ratio. However, some folks prefer to refer to it as the “Shiller P/E”[12]

The calculation of the CAPE Ratio is simple (assuming you have the component data available):

1) Gather the past 10 years of annual earnings from S&P 500 Index companies;

2) Adjust each year’s earnings for inflation (using CPI) – adjusting them to today’s dollars.

3) Calculate the average of these 10 years of inflation-adjusted earnings.

4) Divide the current S&P 500 Index by the number you calculated in 3) above.

Few experts dispute that the CAPE Ratio does a helpful job in smoothing out the data, reducing distortions, and adding clarity to “Valuation”. Here is just one simple example of how the CAPE Ratio can add clarity:

The highest peak in regular P/E came in the first quarter of 2009, by which time S&P earnings had collapsed by over 50% from 2007. Therefore, the P/E was an astronomical 123. If a 2009 investor compared 123 with the then historical mean P/E Ratio of 15, she/he would naturally be reluctant to invest in the S&P at all!

In contrast, Shiller’s CAPE Ratio stood at a modest 13.3 at that very time… its lowest level in decades. If one was a follower of CAPE, he/she could have grasped that opportunity to (in Cramer’s terms) “buy, buy, buy.

So now we have an accepted, time-tested “Valuation Indicator” from a Nobel Laureate!! Pretty cool, don’t you agree?

I think I have finally found the modern “holy grail” for which I asked at the start of this article! What does the esteemed Dr. Shiller think about the U.S. Equity Market right now?

At an appearance in New York on May 6th, Shiller commented on the U.S. economy by suggesting that while this country has looked like one of the strongest developed world economies:

“… but I’m distrustful.”

Shiller went on to admit that he perceives pockets of “animal spirits” within the U.S. economy (fracking and technology were highlighted by him) – the current economic expansion has seen fewer hot new innovations than were seen in prior economic cycles!

Moving on to the Equity Market, Shiller observed that, based on the current CAPE Ratio level, equities could be expected to return an average of 2% annually over the next decade. While that is a small return, it is a higher return than he expects from bonds! He added this commentary

“My gut feeling is this doesn’t look right…. [but] I haven’t met anyone who sold everything. People are worried, but no one knows what to make of [the markets] because interest rates are so low.”

Well, you do have to give Shiller credit for not pretending to be omniscient! And he is correct that few wise investors ever sell “everything”. But so far, Shiller and his indicator do not inspire confidence as a “holy grail”.

Let’s take a look at what Shiller’s assessment on the market was in April when he was interviewed by MarketWatch. The interviewer pointed out that the CAPE Ratio stood at 27.2, a level only exceeded during the pre-crash periods of 1929, 2000, and 2007. Then the interviewer observed that, despite CAPE metrics, the S&P 500 was (then) less than 3% from its record high. In addition, it has not suffered from a 10% correction since October of 2011.[13] At that point, Shiller observed the following:

“This stock market is an enigma. Short-run forecasts are very difficult… [but CAPE is very elevated] When CAPE is this high, 10-year returns on the S&P 500 are nearly flat, because inevitably there is a major correction…

“While history suggests current levels signal a correction, it does not mean we will have one soon,… CAPE could go higher, as it did in 2000, so until then, stocks could keep rising. The problem is, you cannot time [a correction] precisely.”

My “take away” from Shiller is as follows:

1) CAPE is very helpful… but not the “holy grail” for which I was looking;

2) If Shiller weren’t so “stiff” (as so many professors are) he’d make a great politician… or even Fed Chair. He equivocates like the best of them!

3) Despite Shiller’s tendency to equivocate, I think it is undeniable that, in regard to the U.S. Equity Market, we are much “closer to a top” than we are a “bottom”!!

Please pay particular attention, by the way, to Shiller’s use of the term “animal spirits”!! That phraseology was quite intentional!!

The book co-authored by G. Akerlof and his disciple, Robert Shiller

This book was published in 2009. Do you notice anything interesting?

Yes, Shiller was the co-author!! Referring to “animal spirits” before a crowd is a savvy way of promoting your book!!

Pop Trivia Quiz: Who is George Akerlof??

Who is Dr. George Akerlof?

Possible answers include:

a) Professor at McCourt School of Public Policy at Georgetown University

b) Noble Prize Winner in Economics

c) Former professor/mentor of Robert Shiller

d) Husband of Janet Yellen.

e) All of the above.

So keep the above in the fore front of your mind for later!!!

Have you noticed (by the way) that I haven’t yet mentioned Warren Buffett and his Oracle-like wisdom? Well it occurs to me that if I have given this much time to a Yale Professor who the majority of Americans would be unable to identify by sight, name, or valuation methodology … I should give attention as well to the country’s most-loved investment icon!

It is commonly noted that Buffett’s “favorite” market valuation metric is the “Market Cap to GDP Ratio”. Below is a July 2015 graph of that ratio published by Doug Short (I updated this graph after this article was originally published in late May):

The basic premise here is that, in the big picture over time, the growth of total market capitalization (U.S. Equities) should reflect the growth of the United States economy.

The basic premise here is that, in the big picture over time, the growth of total market capitalization (U.S. Equities) should reflect the growth of the United States economy.

What leaps out at us is that the current ratio of this indicator is higher than ever before, with the exception of the 2000 “Dot.com Bubble”. This means two things:

1) Based on this indicator alone, U.S. equity valuation is quite high

2) It also shows how incredibly out of proportion “Market Cap” was back in the year 2000 (leading up to which “experts” kept assuring us that “this time is different”!)

But I hasten to add (and emphasize) that overvaluation can continue for a long time (1998 to 2000 being a case in point).

INVESTOR TAKEAWAY:

When I started, all I really wanted was one solid, concrete, dependable answer to a simple question:

Is the U.S. stock market is over-valued, fairly-valued, or under-valued?

That is not an unreasonable question, is it?

Well, actually, I am now convinced that it is!

Why? For at least these reasons:

1) I have shown you multiple different methods by which to calculate earnings.

a) Obviously, since the market is predicted upon a stock’s ability to generate earnings, the “earnings” metric is one of the most central data points upon which we must agree before we attempt to calculate “Valuation”.

2) Although price is ascertainable on any given date, and therefore empirical (dependable), there are other factors that some experts (strongly) claim must be considered in order to calculate a valid “Valuation” metric, including at least these:

a) Interest rates (the “Risk-Free Rate”)

b) Investor “expected/needed future return” on investments

c) Average market dividend yield.

3) And perhaps most important of all, the unfortunate truth is:

“Value is in the eye of the beholder”.

a) We will easily agree that this is true with regard to “Art”.

b) But this is also true throughout all of life.

i) Without this truth, there would be no value in advertising.

ii) “Branding” would be pointless.

iii) My brother and I would both drive a BMW[14]

The fact is that methodologies similar to that developed by James Gregory Savoldi[15] — Behavioral Analysis of Markets – are garnering more and more attention and credibility! In fact, an entirely new discipline of academic study is spreading and becoming more sophisticated: Behavioral Finance.

Any attempt to briefly summarize the underlying premises of this approach is bound to be overly simplistic. But in order to offer you at least a “flavor” of these approaches, consider this (abridged from en.wikipedia.org):

“Behavioral Analysis uses clues created by today's emotional responses to market behavior in order to predict future market reversals. According to the principles of behavioral analysis, events unfolding in today's financial markets are currently creating a map of the future that will be strictly followed regardless of any attempts through human intervention to change the outcome of price movement. The logic behind this assertion can be attributed to the fact that, regardless of lessons learned by previous generations, human beings seem predisposed to repeat both positive and negative behavior exhibited by past generations..”

“Because of this assumed ‘law of nature’, market participants' reactions to future events—although dynamic in emotional extremes—will continue to elicit greed and fear, driven by the intrinsic human desire to pursue pleasure and to avoid pain, and that in turn will result in predictable repeatable reactions in financial markets.”

One simple example of “knowledge” gleaned from this emerging discipline is the power of “loss aversion”. Specifically, studies are generally in agreement that investors’ emotional response to “loss” is twice as strong as their response to “gain”. That insight can assist (for example) in explaining why markets are much quicker to fall than to climb!

At this point, I will wrap up by offering some investment advice (on principles… not “buy” or “sell” advice) and then pose a premise that you will either find amusing or absurd.

First, the “advice”:

1) Never accept as determinative any single valuation analysis you hear, see, or read.

a) No one person is omniscient about the Markets (or anything else).

b) There are no exceptions – no matter if the person is Yellen, Stovall, Shiller, Buffett, or Petty (or your Uncle Wally).

2) Always make sure your aggregate investments are well diversified.

a) Broad diversification is the best “Risk Management” tool to use in any Market condition – be it under-valued, fairly-valued, or over-valued.

b) Asset Allocation appropriate for your own Risk Tolerance is the best way to ensure adequate diversification!

3) The current “Market” can continue moving upward…. no matter what Yellen, Stovall, Shiller, or Buffett say about it!

a) That said, even if you adjust for low interest rates, low inflation, and “Forward-Looking” earnings, when measured against “Market History”, it would be fair to say that we are closer to a top than a bottom.

Finally, here is my “premise”:

1) Since Market Value is not a scientifically ascertainable matter… but rather is driven by the growth of global economies, the profits of publicly-traded companies, monetary growth, inflation, and the collective perception of millions of investors; and

2) Behavioral Finance experts have alerted us to a whole range of emotional and psychological forces at work within us that, unless managed well, serve to sabotage investment success; and

3) Since Drs. Akerlof and Shiller recently popularized an old English schoolyard term (from the late-Victorian era) through the title and theme of their book (Animal Spirits)… a term actually first used relative to economics by none other than the iconic John Maynard Keynes (in his 1936 book[16]) to describe the instincts, proclivities, and emotions that influence and guide human behavior …

This is the cover of Keyne's 1936 book

Then my suggestion to you with regard to how to think about “Market Valuation” is the following:

Within the centuries-long development of the English language, there was an old Norse term for “nature spirit”. Think about that for a moment. Recall how often we talk about the “Market” as if it is some disembodied, unpredictable force beyond out control… such as

“The Market will make sure that it proves the largest number of traders wrong!”

Of course, we also often talk about the “Market” as though it answers to the beck and call of “Wall Street”… a few fat cats who determine what the “Market” will do next. But let’s face it folks, it has been proven that the “Market” is much bigger than “Wall Street”! Otherwise, those fat cat hedge fund managers wouldn’t so often have to struggle to produce even modest profits! And even more to the point, the CEO of Wall Street’s most prominent member firm, Jamie Dimon of J.P. Morgan Chase (JPM), would not have been utterly shamed and humiliated by the $6.2 billion “London Whale” trading loss!!

No, my friends, the “Market” does not bend to the will of Wall Street! And we know first hand that the “Market” does not bend to the will of you or me!

Instead, we are assured by no less an authority than the “father” of “Keynesian Economics… as well as by two Noble Laureates… that the “Market” is driven by “animal spirits”…. spirits of Nature… far beyond our control!!

Now the standard lore is that a “Bull” and a “Bear” drive the markets.[17] However, how often do any of us actually encounter a bull or bear that has any impact on our trading decisions?

Nope! We need a much more appropriate image… one that can resonate with us on a personal level. After all, we are told these “spirits” drive our every day choices… sometimes for good (trading profits) and sometimes for bad (losses!).

As a service to our loyal Market Tamer readers, I plumbed the depths of my imagination to conjure up the best image… and it came to me in a flash of insight:

Ladies and Gentlemen, I give you the Puca!

![]() The term “Puca”, in fact, derives from that old Norse term I referred to earlier – a term we translate as “nature spirit”! So, see, it fits our thesis perfectly!

The term “Puca”, in fact, derives from that old Norse term I referred to earlier – a term we translate as “nature spirit”! So, see, it fits our thesis perfectly!

These famous creatures from folklore can bring either good or bad fortune! For example, in Irish traditions, they were thought of as having hindered or helped those who lived in rural or coastal communities.

Pucas can change shape/form (shape shifters) – most frequently appearing (variously) as a rabbit, goat, black horse, or in some semi-human form. In my own experience, there are times when I am visited by this form of Puca (namely, when I become hesitant, uncertain, and indecisive):

Here is the "Indecisive" Puca

Then there are days when I feel that something is messing with my mind. I enter trades incorrectly, I become distracted, and I seem “off my game”.

Here is the Mischievous Puca who likes to mess with my head!

But my most dreaded days are the ones when it seems I have been beset by the dreaded “Gap Down Puca” … such as when Chinese brokers suddenly jack up margins overnight and the iShares FTSE/Xinhua China 25 Index

This Puca besets me on days when the profits accumulated from the prior several days disappear in a pool of red on my screen.

FXI ETF has fallen 4% long before the U.S. exchanges finally opens for trading… or it is announced that a big hedge fund manager has taken a sizable position in McDonalds (MCD), on which (of course) I have a Call credit spread!

What I really want is to know is this: which Investment Education professional is powerful enough to secure me the companionship of one single Puca (also spelled “Pooka”, by the way). Of course, the one I have in mind is the one that followed Jimmy Stewart around in the classic movie “Harvey”:

From the classic movie, "Harvey", starring Jimmy Stewart

I am confident that if “Harvey” followed me throughout each trading day, he could help me avoid all those pesky emotional pushes/pulls that the “Behaviorists” have warned us about. He could keep me calm and steady throughout the day, helping ensure that I become neither too confident nor too discouraged. And whenever something goes really wrong and I start berating my computer with crude four letter threats and epitaphs… Harvey could quickly help me get a grasp on myself and regain both composure and perspective.

I think Harvey and I could figure out “Market Valuation” day-by-day… and likely do it just as convincingly as we have seen “Wall Street” do it above.

[NOTE: Remember, friends, I fully disclosed at the start that you would find my “premise” to be either amusing or absurd! I imagine you will agree I was true to my disclosure.]

DISCLOSURE:

The author is not omniscient… nor is he a Noble Laureate, a CNBC commentator, a Wall Street “insider”, or one who appears within the “Contact List” of Yellen, Stovall, Shiller, or Buffett. Nor (by the way) is he in need of psychotherapy because he sees Pucas!! He is just an investor like you…. subject to all the human frailties which (per “Behavioral Finance”) regularly afflict the average investor!! Nothing in this article is intended as a recommendation to buy or sell anything. Always consult with your financial advisor regarding changes in your portfolio – either subtractions or additions.

FOOTNOTES:

[1] The “Bubble” question was almost certainly a pre-planned one, agreed upon by Lagarde and Yellen to make a point.

[2] If Benjamin Bernanke could be called the “King of Quantitative Easing”, Yellen must be the “Queen”.

[3] Stovall received an MBA in Finance at New York University and a B.A. in History/Education from Muhlenberg College (Allentown, PA). He is also a Certified Financial Planner (C.F.P.) and serves as a Trustee of the Securities Industry Institute – which is the executive development program sponsored by the globally renowned Wharton School.

[4] Stovall’s P/E calculations are based on Quarterly GAAP Earnings.

[5] Yes, and Bloomberg and Fox Business as well!

[6] 1950’s thru 1980’s.

[7] Or abolished

[8] The term “juicy” is a not too subtle allusion to the extraordinary profits that big Wall Street firms garnered by serving as the consultants and financiers behind LBO’s!!

[9] For details see http://berkshireh.blogspot.com/2007/08/origins-of-ebitda-and-its-implications.html

[10] See http://www.fasb.org/jsp/FASB/Page/SectionPage&cid=1176164442130&pf=true

[11] Graham and co-author of Securities Analysis, David Dodd, recommended using a multi-year average of earnings per share – such as 5, 7, or 10 years – when calculating P/E in order to control for cyclical distortions.

[12] It can even be referred to as “P/E 10” (because it is calculated using an average of 10 years of earnings). However, note that P/E 10 can also refer to Graham/Dodd’s analysis, as we’ve seen earlier.

[13] During the September/October 2014 period, It did get as close to such a correction as we’ve seen in recent years… but that decline fell short of 10%.

[14] To clarify… he drives a BMW, I drive a modest Honda

[16] The General Theory of Employment, Interest, and Money

[17] Many cite the first use of “bull” and “bear” within the investing context as the now obscure book by Thomas Mortimer: Everyman His Own Broker (published in the late 18th Century.

Related Posts

Warren Buffett's $334 Billion Warning to Wall Street Is a Critical Lesson for Investors. Here's What to Do If the Stock Market Crashes.

Warren Buffett's $334 Billion Warning to Wall Street Is a Critical Lesson for Investors. Here's What to Do If the Stock Market Crashes.

Also on Market Tamer…

Follow Us on Facebook