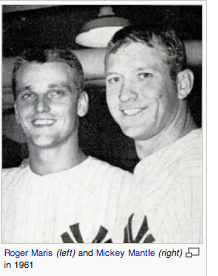

The past year and a half has witnessed a sea change within the investment world: an undeniable shift within the investment public from interest in “active portfolio managers” to “passive (index) managers”! Instrumental in this shift have been two men who share a last initial – “B”. For those few among you who remember Mickey Mantle and Roger Maris from the 1961 New York Yankees[1] (Maris hit 61 home runs; Mantle hit 54[2]). They became known as the “M&M Boys”.

The past year and a half has witnessed a sea change within the investment world: an undeniable shift within the investment public from interest in “active portfolio managers” to “passive (index) managers”! Instrumental in this shift have been two men who share a last initial – “B”. For those few among you who remember Mickey Mantle and Roger Maris from the 1961 New York Yankees[1] (Maris hit 61 home runs; Mantle hit 54[2]). They became known as the “M&M Boys”.

Mickey Mantle (foreground) and Roger Maris were the cornerstone of the powerhouse New York Yankees of 1961... often referred to as the "M&M Boys".

Today’s duo could be called the “B&B Boys”!

Let’s take a look at the data:

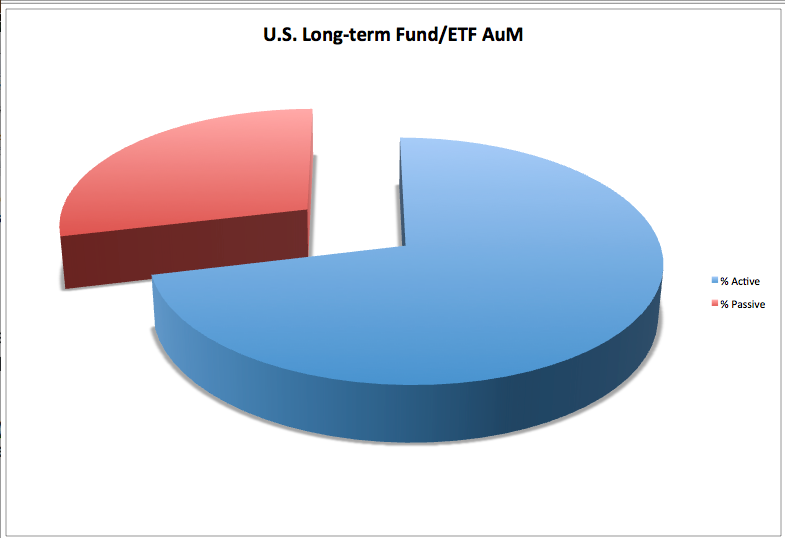

- At the end of August 2014, long-term U.S. mutual funds and ETFs held almost $14 trillion of investor assets (all data that follows comes from mutual fund and ETF analysts at Morningstar).

- At that point, the preponderance (71%) of those assets was invested in funds/ETFs identified as actively managed:

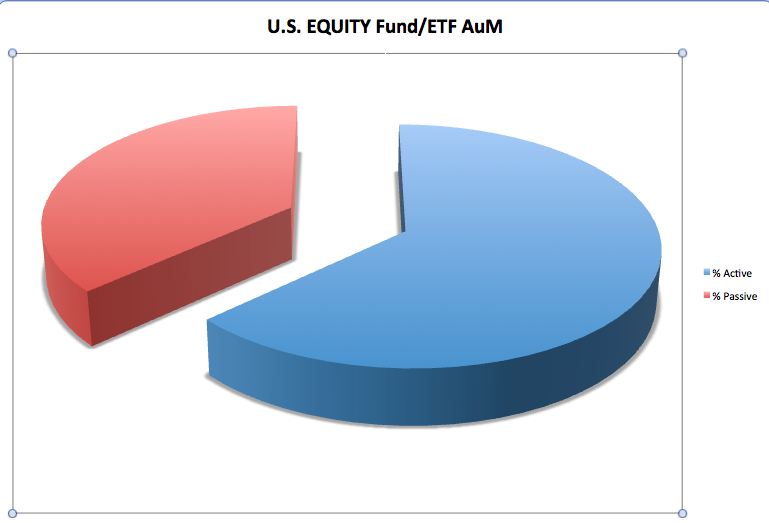

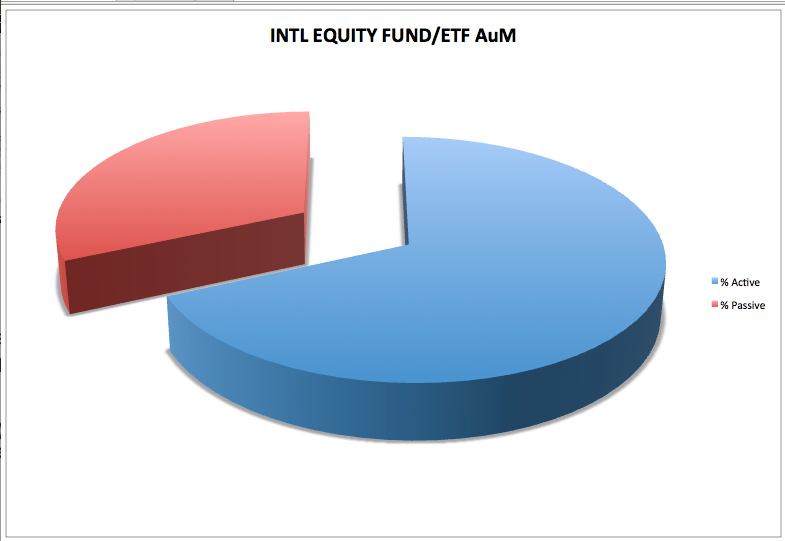

Drilling down a bit further, “active management ” has a commanding “Assets Under Management” (AuM) lead over “passive” in these categories:

1) U.S. Equity (63% vs. 37%)

2) International Equity (68% vs. 32%)

Chart created by Thomas R. Petty, CFP, based on Morningstar data.

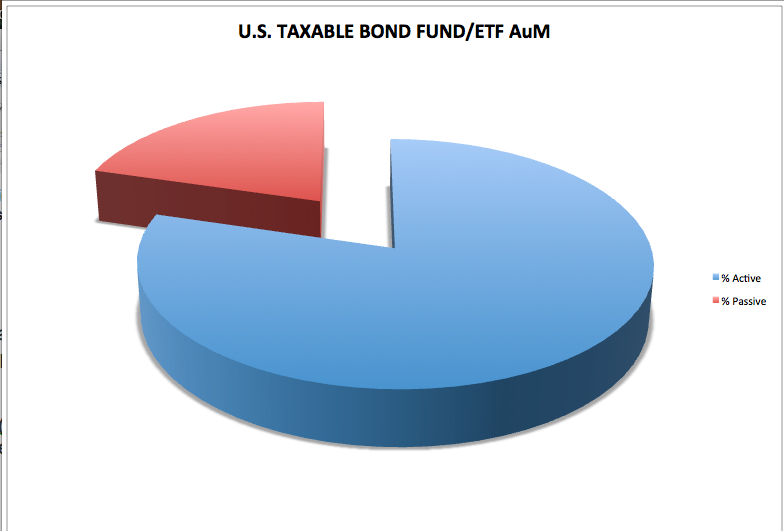

3) U.S. Taxable Bonds (80% vs. 20%)

Chart created by Thomas R. Petty, CFP, based on Morningstar data.

4) Asset Allocation (96% vs. 4%)

5) Alternative Investments (76% vs. 24%)

“Active“ also trumps “passive” within the U.S. Sector Equity space, but by a slimmer margin (54% vs. 46%), Interestingly, “passive” leads “active” in the “Commodities” space (64% vs. 36%).

So far, there is nothing particularly startling here – especially since the mutual fund industry has been dominated for years by actively managed funds[3]. It is also intuitively obvious that some of these categories will remain dominated by “active” management (at least until machines become even more capable of “A.I.”[4]):

- Almost by definition, “Asset Allocation” funds/ETFs will be dominated by “active” management, at least for the foreseeable future;

- Similarly, the same will hold true for “Alternative Investments”.

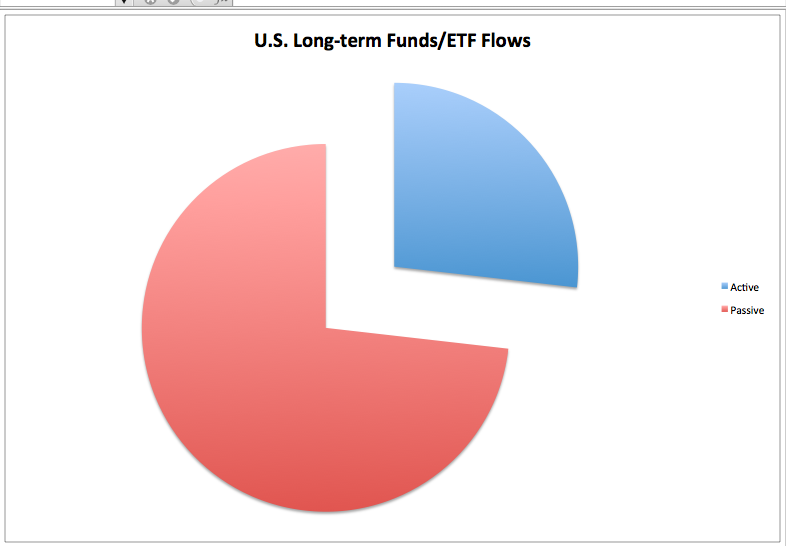

That being said, the sea change to which I referred to earlier is a remarkable shift in momentum! Take a look at these data points regarding the amount of new investment funds flowing into “passively managed” funds and ETFs versus “actively managed” funds and ETFs during the 12 months ended 8/31/14:[5]

- U.S. Long-Term funds/ETFs: “passive” instruments have hauled in 73% of all new funds

Chart created by Thomas R. Petty, CFP, based on Morningstar data

- U.S. Equity: investors have actually caused “active” funds in this space to experience a net OUT flow of funds totaling $55.31 billion. That means that “passive” has captured 173% of all the net inflow!

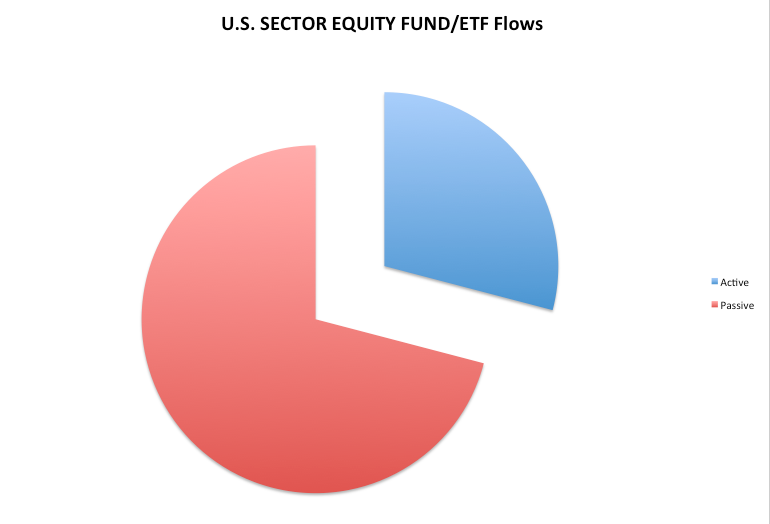

- U.S. Sector Equity: “passive” has garnered 71% of new inflows.

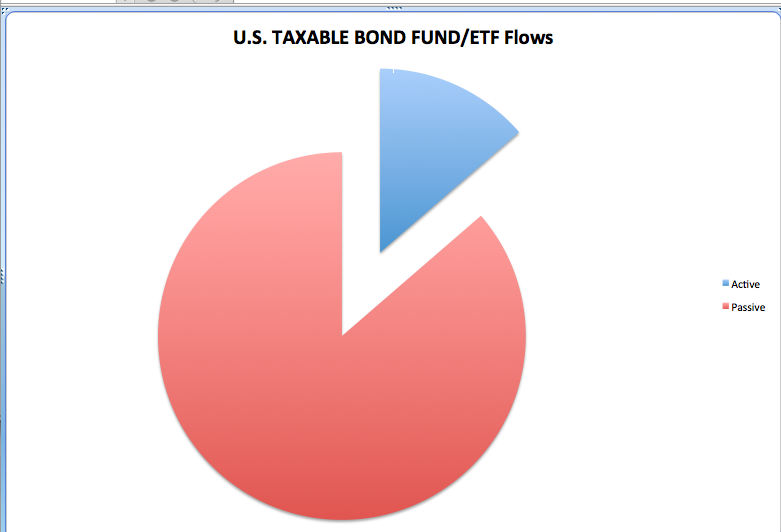

- U.S. Bonds: “passive” has drawn in just over 86% of all inflows.

As expected, “active” still dominated in the “funds flow” metric in the “Asset Allocation” (94%) and “Alternatives” (90%) spaces!

Are you startled by these graphs of recent “funds flow” metrics? There is certainly no doubt that momentum has dramatically shifted within the “active” versus “passive” management dichotomy! The U.S. investing public is storming into “passively managed” investments.

There has one particular beneficiary of this trend. Can you guess which fund provider has been dominating the fund space during the past year and one half?

It is the provider most often associated with “index investing” – in part because it is mammoth, but also because of its founder,

John Bogle, founder and retired CEO of the Vanguard Group.

John Bogle – who was strongly influenced by the academic work of Paul Samuelson (a Nobel Prize honoree), Burton Malkiel (author of A Random Walk Down Wall Street and a director within Bogle’s firm for almost 30 years), and Eugene Fama (another Nobel Prize recipient – as of 2013). Each of these three renowned financial experts have been a strong advocate of “passively managed” index funds. Influenced by these financial giants, Bogle created his own investment firm in 1974 and created the first publicly available index mutual fund just one year later:

![]()

That first (and therefore, innovative) fund was called: the Vanguard 500 Index Fund (VFINX). Of course, Bogle and Vanguard created many other funds in the decades that followed. Bogle’s book in 1999, Common Sense on Mutual Funds: New Imperatives for the Intelligent Investor (updated and reissued in 2009)

offered investors a simple, easily understood approach to successful investing that summarized his strongly held philosophy regarding how to be profitable. Sigma Investing has done a laudable job outlining a bullet point summary of Bogle’s essential thesis (http://www.sigmainvesting.com/reading-materials/common-sense):

offered investors a simple, easily understood approach to successful investing that summarized his strongly held philosophy regarding how to be profitable. Sigma Investing has done a laudable job outlining a bullet point summary of Bogle’s essential thesis (http://www.sigmainvesting.com/reading-materials/common-sense):

- Select low-cost funds

- Consider carefully the added costs of advice

- Do not overrate past fund performance

- Use past performance to determine consistency and risk

- Beware of stars (as in, star mutual fund managers)

- Beware of asset size

- Don’t own too many funds

- Buy your fund portfolio – and hold it

Given the financial events between 2000 and 2009 (including two equity crashes… that resulted in a decade yielding a return barely above 0%[6]) … I am uneasy about Bogle’s final point. However, Bogle is hardly alone in holding firmly to that point. In fact, there is another legendary investment figure from Bogle’s own generation who regularly preaches the same basic lesson … as often as not referring to John Bogle by name in the process!

Can you guess which legendary investment figure preaches “index investing” and (unofficially) helps promote Bogle’s passively managed funds?

Hmmmm…. You might initially think it is Warren Buffett, the wizened wizard from the western reaches of the U.S. Midwest. But no, that can’t be! After all, Buffett is a virtual incarnation of the classic “Active Manager”!

Consider this: in the most recent annual report from Berkshire Hathaway (BRK.A), the following metrics became crystallized for us:

- BRK.A’s 4th Quarter showed operating earnings totaling $3.7 billion for the fourth quarter of 2013 — 34% higher than the prior 4th quarter!!

- Including investment and derivative gains accrued during the 4th quarter, BRK.A enjoyed net income just a bit less than $5 billion … a new record!

- These figures overshot the projections of analysts.

- The book value of each share of BRK.A moved up to $134, 973 – an 18% increase vis-à-vis one year earlier!

- As a consequence, the six-year stock price performance of BRK.A between 2007 and 2013 outpaced the S&P 500 Index!!

Great active managers just don’t go around trumpeting “Index Investing”… right?!

Wrong!! Warren Buffett does!

Buffett has become so renowned that we can even recognize his familiar visage as it was 24 years ago... in 1980!!

Buffett’s letter to shareholders from that very same (February 28th) annual meeting was widely referenced (and excerpted) this past March. After prefacing his remarks by clarifying that, upon Buffet’s death, his personal BRK.A shares will be distributed to charitable institutions, Buffett offered this prospective “advice” to the trustee of his estate[7]:

“My advice to the trustee couldn't be more simple: Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard's.[8]) I believe the trust's long-term results from this policy will be superior to those attained by most investors — whether pension funds, institutions or individuals — who employ high-fee managers.

“Both individuals and institutions will constantly be urged to be active by those who profit from giving advice or effecting transactions. The resulting frictional costs can be huge and, for investors in aggregate, devoid of benefit. So ignore the chatter, keep your costs minimal, and invest in stocks ….”.

There is a wealth of fascinating insights packed into that letter. I urge you to take a few minutes to access the “pdf” of the document and at least skim Buffett’s commentary[9]. For your convenience, I have inserted (at the end, before the “Footnotes”) key excerpts that specifically address this “active vs. passive” debate. In light of this treatise by Buffett on passive indexing… I now refer to Mr. Bogle and Mr. Buffett as the “B&B Boys” –

The "B&B Boys"... powerhouses within the investment industry!

packing as much of a powerhouse passive investing punch in the investment arena as home run kings Mantle and Maris packed in Yankee Stadium.

For all of those too young to remember, here is Roger Maris on the left and Mickey Mantle on the right! It is well worth noting that they accomplished their joint achievement (115 home runs) without the aid of any steroids or human growth hormones!!

With the revered voice of Buffett holding forth on passive investment management, and garnering national (and international) media coverage — repeating (and even amplifying) Buffett’s most essential points, he was handed quite a “bully pulpit” through which to advocate for passive investing. Did Buffett’s advocacy have any significant impact?

Well, I refer you to all the data and graphs that I presented earlier. But in particular, consider these telling metrics:

- In first quarter of 2014… Vanguard added $13.1 billion of ETF assets… nearly 90% of all new capital flowing into any/all US ETFs during that period!

- Between January and October of this year… $163.4 billion flowed into Vanguard funds and ETFs combined … that was almost 16% higher than its prior full-year record set in 2012 (which was just $141 billion).

- Vanguard drew in $24.5 billion of assets during October… the second highest monthly total during the entire 40-year history of Vanguard.

- During the first nine months of 2014, consider the top ten U.S. ETF's with regard to asset inflows. Five of those ETFs come from Vanguard:

- Vanguard S&P 500 ETF (VOO)

- Vanguard FTSE Developed Markets ETF (VEA)

- Vanguard Total Stock Market ETF (VTI)

- Vanguard REIT ETF (VNQ)

- Vanguard Total Bond Market ETF (BND)

- In particular, the Vanguard 500 Index Fund (VFINX) raked in four times more new investment dollars than it did during the 2nd Q of 2013!

- During October (following the news regarding Bill Gross’ departure from PIMCO Funds (see: https://www.markettamer.com/blog/bond-king-gross-jumps-ship-to-janus), the Vanguard Total Bond Market Index Fund (VSMFX) saw $4.4 billion of new funds roll into the fund – fully three times greater than during October of 2013!

- October was not just a great month for VSMFX. The entire Vanguard “family of funds” took in a grand total of $24.5 billion of new assets during the month … its second highest monthly total in its 40-year history!

All during this past year, headlines frequently appeared within financial professional publications that trumpeted Vanguard’s success within the industry with regard to asset inflows within its mutual funds and/or ETFs.[10]

What has the result been? Vanguard has become an international investment management powerhouse, managing over $3 trillion of assets. You might not remember this, but Vanguard surpassed Fidelity Funds as the biggest U.S. mutual fund company about four years ago! Within the ETF space, Vanguard has very successfully scaled up to become the third largest provider of ETFs… growing so briskly that it has nearly overtaken the firm currently ranked number two!! Finally, on a global scale, Vanguard has become the second largest asset manager in the entire world![11]

BlackRock is the world's largest investment asset manager.

OK. We’ve established that the investing public as a whole has (at least for now) been spurning active managers and turning (instead) to passive (index) managers. Why have investors been swinging toward passive funds and ETFs during the past couple of years?

1) Because the majority of articles that have been written in the financial press during the past few years have touted statistics that show passive funds outperforming active funds:

a) Fewer active managers have outperformed the market during the past year than at any other time during the past decade.

b) Bank of America data indicates that less than one in five active managers have beaten the market for the year ending October 31, 2014.[12]

i) In particular, only 17.7% of active managers have outperformed beat the Russell 1000 index of large-cap stocks (through October) — down from 40.5% in 2013.

ii) The bank data indicates that the average fund lagged behind the Russell 1000 by about 2%.

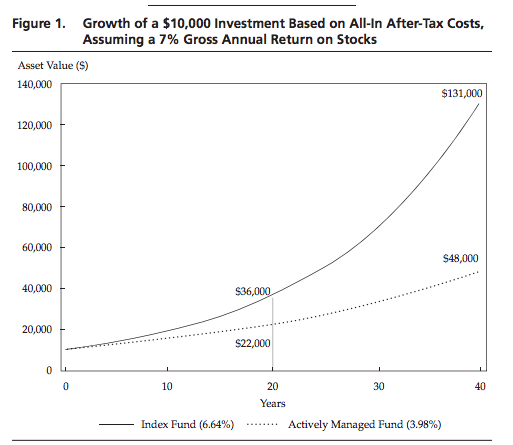

c) Here is a dramatic graph [from (http://www.cfapubs.org/doi/pdf/10.2469/faj.v70.n1.1 )[13] ]

This telling graph comes from an article by John Bogle that was published at the beginning of 2014.

2) With regard to actively managed funds under-performing in 2014, consider what we’ve been hearing from countless managers this year:

* “This is a very difficult market to trade.”

* “This market is like no other I’ve seen in decades.”

* Illustrating this reality is that a large number of hedge fund managers have had (figuratively) “their head handed to them” by the market this year.

* In addition, this market has baffled some of the best known educators and investors, illustrated by this simple story:

Regarding the recent “V bottom” in the S&P 500 Index, the author will never forget the skepticism of one authority (author of two widely read books). In each day’s commentary on the market, he expressed his mounting skepticism as we all watched the right side of the “V” move inexorably upward:

Each day he reminded us that: “the Market just doesn’t move so sharply down and then back up”

Nonetheless… it did!

3) There has been a recurring (and entirely accurate) theme that has run through countless investment articles each year since 2010… something along the lines of:

a) “It’s a pity that so many millions of investors sold toward the bottom of the 2007-09 market crash. If only they had hung on, they would now have made up a huge portion of their losses.” OR

b) “Pity the poor souls who sold on the way down in 2009 and have kept their funds in low yielding CD’s and Treasury Bills. All they have done is lost considerable ground to inflation.”

4) Then there are revered experts (such as Buffett and Bogle… whom I have dubbed the “B&B Boys”) who testify, authoritatively, that passive investing is the way to invest — hands down!

OK, so there are multiple compelling reasons for the public’s investing preference to change as it has! Why then, has Vanguard become such an preponderant attractor of investors’ funds?

1) Vanguard has an extraordinarily long record of quality management and regularly receives great reviews (helping enhance its very positive brand within the mind of the investing public).

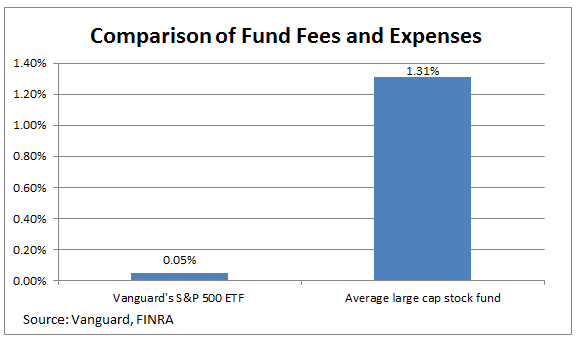

2) It is demonstrably (on an asset-weighted, fund family basis[14]) the “low cost provider” of funds (especially index funds).[15]

This graph comes from the "Motley Fool" website.

3) Most of Vanguard’s ETFs and funds provide exceptional liquidity![16]

Of course, the financial press prefers simpler story lines to more complex and involved story lines. So naturally, the bulk of the stories on this topic[17] as much as suggested that the reason Vanguard has thrived so gloriously during this past year is the unparalleled influence and persuasive powers of the “Wizard of Wall Street” – Warren Buffett – who (they write) virtually endorsed John Bogle and Vanguard in his February 28th letter!

I hate to break it to the powers and principalities that are the “financial press”… but the fact is that, although Buffett is quite prominent within all-time pantheon[18] of “Investing Geniuses”, Buffet is decidedly not a god! Nor does Buffett have such direct power over the minds of investors that they would act in such unanimity merely because Buffett wrote a commentary in his firm’s shareholder letter!

Indeed, if Buffett exercised such investor “mind control”[19], the shift to “passive” investing would have happened long ago. After all, Buffett has been actively touting index investing, Bogle, and Vanguard for many, many years:

* In 2004, at the annual meeting of BRK.A, one shareholder asked Buffett if that person should hire a broker, invest within an index fund, or simply buy BRK.A shares[20]

Ever the wily one, Buffett replied:

“We never recommend buying or selling Berkshire. Among the various propositions offered to you, if you invested in a very low-cost index fund – where you don’t put the money in at one time, but average in over 10 years – you’ll do better than 90% of people who start investing at the same time.”

* During another occasion, Buffett was asked a question that prompted this reply:

“If you like spending 6 to 8 hours per week working on investments, do it. If you don’t, then dollar cost average into index funds. This accomplishes diversification across assets and time, two very important things.”

* And Buffett has previously identified a name (and a therefore a “brand”):

“Just pick a broad index like in the S&P 500. Don’t put your money in all at once; do it over a period of time. I recommend John Bogle’s books –

This is another of John Bogle's books on investing.

any investor in funds should read them. They have all you need to know.”

So if the “Oracle of Omaha” really commanded powers similar to those of the mythological gods on Mount Olympus, then Vanguard would long ago have surpassed BlackRock as the largest asset manager in the world!

No my friends. Although Bogle and Vanguard might (rhetorically) owe a marketing fee to Buffett for being such a strong advocate of passive investing (and Vanguard-style passive investing)… the true impetus for this sea change has been a synergy among all of the factors I identified above.

However you want to identify attribution for this sea change… performance, cost, and or the “B&B Boys”… the fact is that it is startling and worth long and serious reflection!

INVESTOR TAKEAWAY:

There is no denying the metrics regarding fund flows detailed above.

There is no denying the multiple factors that are currently pulling investors toward (and into) passively managed funds and ETFs.

There is, however, an intriguing (and potentially controversial) topic worthy of our time and attention in our next article:

Here is Warren Buffet, decked out in his formal dinner finest, accompanied by his wife, Astrid Menks.

“Will Buffett’s wife (Astrid Menks) be better off with a 90/10 Asset Allocation[21] …. or with a more diversified portfolio designated for her by a Robo-Advisor?”

Keep your eye out for it, folks. I can assure you it will be interesting!

DISCLOSURE:

The author has been invested in various Vanguard funds since at least the 1980’s. He is currently invested in both Vanguard funds and ETFs. The author has also owned BRK.B shares and options at various points in the past, but does not currently hold any BRK.B. The author is not affiliated with the Vanguard Group and pays the same annual fees that all other Vanguard investors do.

APPENDIX

Here is the excerpt I promised from Buffett’s February 28th shareholder letter. Below, I pick up the text just after Buffett has counseled everyone (he uses the term “these non-professionals”) to resist the (persistent) advice from brokers (and other investment “experts”) to buy active funds (and/or try to time the market):

“I have good news for these non-professionals: The typical investor doesn’t need this skill. In aggregate, American business has done wonderfully over time and will continue to do so (though, most assuredly, in unpredictable fits and starts). In the 20th Century, the Dow Jones Industrials index advanced from 66 to 11,497, paying a rising stream of dividends to boot. The 21st Century will witness further gains, almost certain to be substantial. The goal of the non-professional should not be to pick winners – neither he nor his “helpers” can do that – but should rather be to own a cross-section of businesses that in aggregate are bound to do well. A low-cost S&P 500 index fund will achieve this goal.

“That’s the “what” of investing for the non-professional. The “when” is also important. The main danger is that the timid or beginning investor will enter the market at a time of extreme exuberance and then become disillusioned when paper losses occur. (Remember the late Barton Biggs’ observation: “A bull market is like sex. It feels best just before it ends.”) The antidote to that kind of mistiming is for an investor to accumulate shares over a long period and never to sell when the news is bad and stocks are well off their highs.

“Following those rules, the “know-nothing” investor who both diversifies and keeps his costs minimal is virtually certain to get satisfactory results. Indeed, the unsophisticated investor who is realistic about his shortcomings is likely to obtain better long term results than the knowledgeable professional who is blind to even a single weakness.”

FOOTNOTES:

[1] From Wikipedia.com: the 1961 New York Yankees’ was the 59th season for the team in New York, and its 61st season overall. The team finished with a record of 109-53, eight games ahead of the Detroit Tigers, and won their 26th American League pennant. … In the World Series, they defeated the Cincinnati Reds in 5 games.

The 1961 Yankees are often mentioned as a candidate for the unofficial title of greatest baseball team in history.

[2] That was the highest total of homers Mantle ever hit in a season. Ironic that it came the year Maris hit 61 (or maybe not ironic, since teams could not “pitch around” Mantle that year).

[3] The reasons for this are many. But you know what a cynic I am, so my take is that this is explained because: 1) vendors can charge more for actively managed funds; 2) actively managed funds are more easily differentiated from other funds for marketing purposes (those huge ads you see in financial publications touting a great annual performance or an eye-catching strategy); 3) a financial adviser/broker can be provided with enticing “stories” about active funds, through which she/he can “sell, sell, sell” (and increase commissions).

[4] Artificial Intelligence

[5] Note that, be of the regulatory requirements (especially daily portfolio disclosure) pertaining to ETFs, that space has been significantly dominated by passively managed index-related funds.

[6] Therefore, it is often referred to as “the Lost Decade”

[7] This excerpt comes from page 20 of Buffett’s letter, which can be accessed at: http://www.berkshirehathaway.com/letters/2013ltr.pdf

[8] Remember this part, friends!!

[9] I note that the letter is also entertaining, including this reference that one might not expect to come from the venerable Buffett: “Remember the late Barton Biggs’ observation: ‘A bull market is like sex. It feels best just before it ends.’”)

[10] As you surely have gathered by now, Vanguard was frequently the asset inflow monthly/quarterly leader

[11] BlackRock is #1, with $4.5 trillion of AuM.

[13] The Financial Analysts Journal from the most recent January/February issue contains an article by Mr. Bogle that made an engaging case for passive investing. Bogle suggested that even if an active fund manager was able to track the S&P 500 Index, an investor in her/his fund would be greatly penalized by higher fees! More to the point, in a study he had performed over a 40-year period, Bogle asserted that the passive investor would garner an average annual return of 6.6% while the poor person who invested in an active fund would have received just 3.9%!

[14] Morningstar data suggests that Vanguard charges 15 cents on each $100 of funds invested, compared with the “average” mutual fund that charges 70 cents (over 3.5 times Vanguard)

[15] And everyone loves a “good deal” and lower costs!!

[16] And of course, the financial backing and enduring credibility of the huge Vanguard organization (with its mammoth capital base).

[17] At least among the many that I read.

[18] “Pantheon” is (of course) an historic structure from Ancient Rome… but much more significantly, “pantheon” is a word derived from Ancient Greek (“Pantheion”) that means: “of, relating to, or common to all the gods”

[19] Think Obi Wan Kenobi and Jedi Knights here

[20] Actually, the investor could choose between BRK.A at $94,000/share on March 1st of that year, or BRK.B at $62.42/share!!

[21] That is industry shorthand for 90% equity and 10% fixed income… in Buffett’s case: 90% S&P 500 Index Fund and 10% Short Term Government Bond Fund (or the bonds themselves).

Related Posts

Is IonQ Stock a Buy?

Is IonQ Stock a Buy?

Also on Market Tamer…

Follow Us on Facebook