I know a number of our readers have been enjoying the opportunities with which I have provided them to “sit in the CEO Chair”![1] In that light, here are a series of timely, real life, real world questions for you to reflect upon and answer as candidly as you are able:

1) Who are you (as CEO) and your Board of Directors legally obligated to serve?

a) Your customers

b) Your vendors

c) Your strategic partners

d) Your country or

e) Your shareholders

2) Assuming that you have created your corporate and production “systems” in a way that will (continuously) ensure that every employee, manager, supplier, sub-contractor, factory, etc. will make every effort humanly possible to ensure that all of your products, services, and reports comply with all applicable laws and regulations, what is your primary fiduciary obligation (as CEO)?

a) To maximize sustainable profits

b) To reward members of management through high compensation and generous bonuses

c) To offer employees the highest compensation (including benefit package) in your industry

d) To ensure that your company always pays taxes to the IRS and local tax entities at the full (current) statutory rate

3) If your company currently competes within the global market (or aspires soon to become an active participant within the global economy)… should your goal be to compete aggressively within the global market (always within the bounds of law) by seeking out and employing the “lowest cost capital and labor” or should you always restrict yourself to capital and labor that is “sourced” within the United States?

In the interest of full disclosure (or more appropriately: a “confession”), I am completely aware that none of the above questions have an absolute, rock solid, “always and for all time” single “correct” answer. Off the top of my head, I can quickly identify any number of folks who would offer one or more responses that are different from my response![2]

That being said, I do believe that an experienced corporate law attorney would suggest that there is just one correct answer for Question 1). I think that (for the great majority of folks) there are only two worthwhile responses to Question 2). However, even though Question 3) is (on the surface) a simple “Yes” or “No” question, the thoughts and feelings that will inevitably accompany any response to that question are certain to be heartfelt (and often complex… with many intertwined parts).

In the context of the above questions, let me ask you a “trivia” question that will be a lot more “fun”! What single current common theme links all of the following images:

Bermuda

Here is a map of Bermuda, located in the Atlantic Ocean east of the U.S.

Ireland

Here is a map of Ireland. The Republic of Ireland is in yellow.

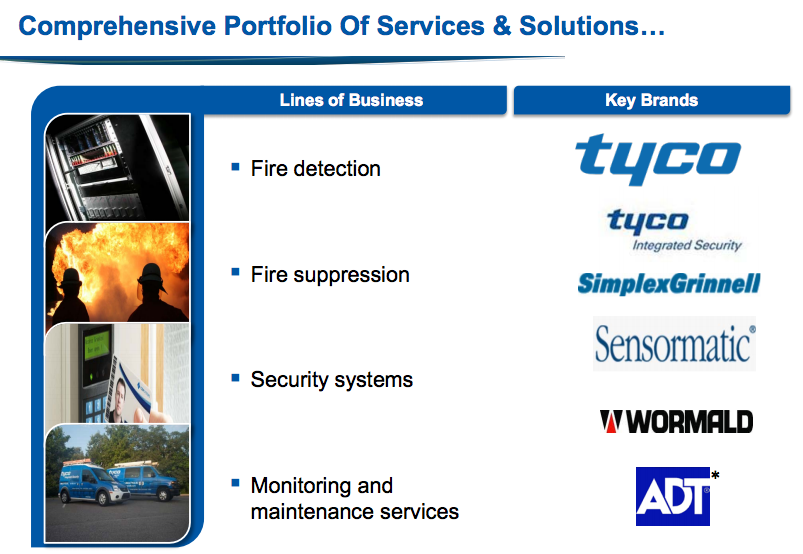

TYCO INTERNATIONAL (hint: note the ADT Logo)

Being a conglomerate corporation, here are a variety of Tyco's brands!

COVIDIEN PLC

This is the Covidien plc logo.

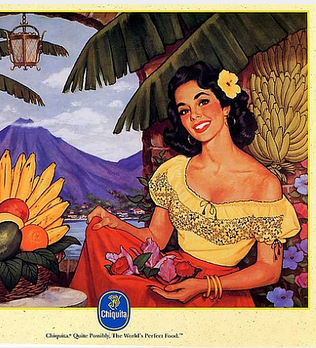

MISS CHIQUITA BANANA (this is a 2012 version of the brand’s “icon” that first appeared in public in the 1940’s and 1950’s, in movie theaters.[3]

This is an "updated" version of "Miss Chiquita Banana"... a long-standing commercial "personification" of the Chiquita Banana brand!

No, my dear readers, I have not gone crazy! There is one very strong common thread that ties all of the above together; and I suspect that when I tell you what it is, you’ll smack your forehead with the heel of your palm and think: ”Geez, I shoulda had that one!”

Here is the common thread:

1) Tyco International Ltd. (TYC) is widely considered to have “kicked off” an exodus of U.S. corporations that used M&A (Merger and Acquisition) activity to secure a non-U.S. tax domicile. In August of 1997, TYC signed a complex merger contract with ADT Ltd. (domiciled in Bermuda) that resulted in TYC being the surviving corporate entity, despite the fact that formally, ADT was the “acquirer”!![4] During that time frame, TYC’s effective tax rate was 40%, while ADT’s was 25%. TYC was subsequently (over time) able to reduce its own tax rate toward 25%! (I’d make that adjustment any day!)

2) In 1997, Covidien (a medical device manufacturer) was at that point a subsidiary business within the sprawling TYC corporate empire. Therefore, it’s “domicile” transferred to Bermuda with TYC! By 2007, Covidien Ltd. (COV) struck out on its own as an independent firm, domiciled in Bermuda.

3) However, by 2009, COV re-domiciled itself in Ireland!!![5]

4) Then this year, Medtronic (MDT) – a huge global manufacturer (fourth largest) of medical devices founded in a Minneapolis garage in 1949[6] — acquired COV to further diversify its business and secure much greater flexibility with regard to its global financial management through “Tax Inversion” (essentially the same goal that TYC employed 17 years earlier! The combined company will be domiciled in Ireland. Up until the Abbvie (ABBV) acquisition of Ireland-based Shire PLC (SHPG) last month (see: https://www.markettamer.com/blog/how-to-evaluate-a-business-like-a-ceo; https://www.markettamer.com/blog/how-a-ceo-performs-a-swot-analysis) , the MDT/COV deal was the largest such deal this year!

5) On March 10th of this year, Chiquita Brands International (CQB) announced a merger with Fyffes PLC (FYFFF)[7] in a “stock for stock” transaction. CQB shareholders will receive 50.7% of the new company’s shares, while FYFFF owners will receive the rest! Key details regarding this transaction (besides the fate of Miss Chiquita) include these two points: the new company will be domiciled in the same location as FYFFF (no surprise here: IRELAND!)… and the stock will be listed on the New York Stock Exchange!

I hope you didn’t hurt yourself when you hit your forehead … thinking: “I shoulda known that!”!!

Before launching into what I firmly believe to be the root cause of all this activity that has tied these five seemingly “unrelated” things together, let me highlight one of the most obvious and eye-catching trends that you surely noted while reading the past page above: IRELAND! It is hard to miss the seeming omnipresence of Ireland within business reports regarding mergers of U.S. corporations with an overseas company! What is going on there?

Allow me to put it simply: Irish political and business leaders know that we live in a global economy. They know that a company is not likely to domicile in Ireland merely because of sentiment, obligation, or the appeal of its tourist sites. Instead, it will domicile in Ireland if Irish tax and economic policy and the Irish labor supply are conducive to that firm’s business, and if such a move will materially increase that company’s access to global capital!

The result is that Irish leaders have made “planting” a business in Ireland about as easy and appealing as possible! It has a statutory corporate tax rate of just 12.5% (the U.S. is currently at 35%)… and it has demonstrated a record of working with companies to foster movement into Ireland![8] Let’s give it up for the officials in Ireland!!!

Consider these results:

The deal value of M&A activity among U.S. companies moving to Ireland (related to “Tax Inversion”) has increased 6-fold during the first six-months of 2014 (vis-à-vis 2013)![9] Just as impressively… take a quick look at your most convenient European map, and then consider that although Ireland was the target “domicile” for just 3.3% of these European mergers so far in 2014… it accounted for 17.7% of all of the “Deal Value” of such transactions! Very impressive! That is the mark of a country whose leaders do not make the mistake of taking anything for granted … leaders who understand that they must help their nation “make money the old-fashioned way… they earn it!”[10]

At this point, you might be thinking: “All of this is interesting, Petty, but what does it have do with US?!”

The answer is that this one single issue (“Tax Inversion”) illustrates countless ways in which the United States (and its leaders) fall far short within the increasingly global and interconnected economic marketplace of 2014!!

Here is a simple definition of “Tax Inversion”:

A globally active U.S. company that derives a significant portion of its income from non-U.S. sources will find that said income gets taxed at both the “foreign source” end and by the U.S. government!![11] Such a company can utilize a “Tax Inversion” strategy to facilitate re-domiciling within a lower-tax country[12] – thereby freeing itself from U.S. taxation on any income earned outside the U.S.!! Naturally, as the percentage of total foreign-source income rises relative to U.S.-based income, the greater the incentive any single company has to try an “Inversion”!!

What has the response been to this growing trend? Consider the outrage expressed by this Democratic Congressman from Massachusetts to the migration of a major U.S. corporation to a lower tax rate nation overseas: “[This company] has raised tax avoidance to an art!!” That Congressman subsequently introduced legislation to force that company to pay taxes as a U.S. corporation!

That Congressman is in no way alone! His outrage has been echoed by countless other Washington D.C. politicians:

President Barack H. Obama called any corporations that initiated an Inversion: “a corporate deserter”[13] The President went on to say: “My attitude is… I don’t care if it’s legal.”[14] Later the President said: “Even as corporate profits are higher than ever, there’s a small but growing group of big corporations that are fleeing the country to get out of paying taxes.”[15] That is not all. In an intriguing leap of logic, President Obama went on to say: “They’re technically renouncing their U.S. citizenship, they’re declaring their base someplace else even though most of their operations are here.”[16]

Not to be outdone, U.S. Treasury Secretary Jack Lew has stepped up to opine (in a letter to Senate Finance Committee Chairman Ron Wyden (D-Ore.))

U.S. Treasury Secretary, Jack Lew.

that the U.S. needs: “[a] new sense of economic patriotism” … describing that as a system within which U.S.-based companies are no longer allowed to do “inversion” transactions![17] And of course, Secretary Lew has a neatly wrapped “answer” to those who point out the inconvenient truth that the “Inversion problem” springs directly from a U.S. corporate tax system that is grotesquely complicated and pitifully non-competitive within the current global market… an axiom that would inevitably lead a clear-thinking person to conclude that the existing system needs to be comprehensively “fixed” first. In rebuttal, Lew posits these points:

1) Even if we completed comprehensive reform… “we would still need to enact anti-inversion provisions because companies always would find countries with near-zero rates to which they could relocate;”[18]

2) “Moreover, even the most optimistic know that the administration and Congress need more time to complete bipartisan comprehensive business tax reform;”[19]

3) “While the business-tax-reform process moves steadily forward[20], the pace of inversions is increasing at breakneck speed. We must confront this problem now, before our tax base is so eroded as to damage the prospects of comprehensive reform.”

And of course, reports appearing on TV, radio, and (in) newspapers during the past few months have included countless sound bites from Senators and Congresspersons practically falling over each other to express their outrage… including condemnation of the “inverting” corporations and demands that legislation be approved to retroactively nullify any “Tax Inversion” benefit!!

This is fascinating, isn’t it?!! I think you’ll find it even more interesting when you read and absorb the next sentence:

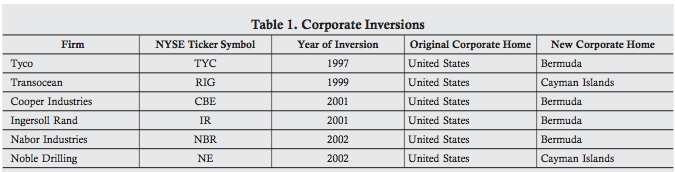

Congress already reformed corporate tax law back in 2002, at the (then) height of “Tax Inversions” that occurred between 1997 (TYC) and 2002, including the following list:

Here are the six "Tax Inversion" deals prior to the end of 2002!

Of course, despite their vociferously intoned sound bites of outrage, it took Congress until February of 2004 to actually produce and approve that reform legislation – but they did!! It can be found within the Internal Revenue Code Section 7874. And I am confident that (during the 2002 and 2004 elections) every last supporter of that legislative reform bill vowed that Section 7874 “solved” the pesky, ugly, annoying problem of “Tax Inversion!!!!

In fact, do you remember my reference to the Democratic Congressman from Massachusetts who decried the despicable firm that had “raised tax avoidance to an art!!” … the Congressman who introduced legislation to force that company to pay taxes as a U.S. corporation?? That was Congressman Richard E. Neal in 2002… referring to TYC!!

Congressman Richard Neal was outraged in 2002 by U.S. companies moving "offshore" and changing their tax domicile.

I am undoubtedly out-of-line, but I find it strange that Secretary Lew did not refer to Section 7874!! In the same vein, I find it disingenuous that President Obama (in the spirit of “transparency”) did not mention: “we’ve been here before”! On that’s right… Washington’s “solution” from the 2002-04 hearings/debates/negotiations and final vote (leading to Section 7874) evidently didn’t work![21]

Let me tell you how Washington dropped the ball on U.S. corporate tax policy (including Tax Inversion):

1) Most “Developed World” governments have been reducing corporate tax rates and making it easier for companies to “bring overseas cash home”… such as the United Kingdom (UK) and Japan… both of whom recognize the need to be competitive within a global economy. Based upon the fact that the U.S. carries the world’s highest corporate tax rate (35%)[22] and makes no effort to ease the barriers on bringing “foreign earned” cash back into the U.S., perhaps the U.S. feels it has no need to be globally competitive;

2) In that same vein, countries such as the U.K. and Canada only tax a company’s profits earned domestically (ie. in that country). The U.S. (in contrast) taxes a company’s worldwide income;

3) A provision of that “worldwide” U.S. corporate tax is that if a globally active U.S. multinational enterprise (MNE) retains profits earned overseas in one of more of its foreign subsidiaries, U.S. income tax on that profit does not need to be paid until it is brought back into the U.S. (“repatriated”). As pointed out in bullet 1) above, many other nations have made it easier to bring such cash home. In fact, in 2004 the U.S. offered a window of “tax amnesty” on repatriating foreign-held cash. However, there is no compelling will in the current Congress to offer such a window any time soon.[23]

4) A number of economic and tax policy experts indicate that there is a basic flaw within the very underpinnings of existing U.S. corporate tax law.

a) There are two general approaches in determining where a company’s headquarters are located (which would determine “tax domicile”):

i) “Place of Legal Incorporation”: this is the “quick and easy” method. No muss; no fuss.

ii) “Real Seat”: this method requires a degree of effort and insightful analysis because it is based upon discerning where a company’s real decisions are made and where the firm’s most substantial assets and employees are located.

b) These same experts suggest that the more logical approach to determining tax domicile is the second method, since (in the real world) “place of incorporation rules” currently enable a MNE to easily relocate the firm to a locale in which that MNE has minimal or no economic presence.

c) If you are not yet totally confused, you have likely recognized that by the very nature of U.S. corporate tax law… combining “Place of Legal Incorporation” with “tax on worldwide income”… the U.S. has ensured that its own MNEs will be inexorably drawn toward the irresistible allure of “Tax Inversion”.

i) For the CEO and corporate board of a globally successful U.S. MNE with a high percentage of foreign-sourced revenue, an “Inversion” would be a practically “no brainer” decision..

ii) An activist shareholder (Icahn, Ackman, Einhorn, etc.) would be justified in asserting that management members and the board have a fiduciary obligation to maximize earnings (and shareholder value) by minimizing net global tax paid.

5) Those of you familiar with tax law know that an indispensable part of any such law becoming effective are the published U.S. Treasury Regulations (“regs”) that incarnate legislative intent and provide practical guidelines for corporate CFOs, accountants, and auditors to follow. In the earliest versions of the published regs related to IRS Section 7874, the Treasury provided extremely helpful detailed examples that served to equip companies with the clarification necessary to understand and comply with the law. Those regs also included a “safe harbor” provision that assisted companies in accurately discerning “substantial business presence” overseas. However, by 2009, both these detailed examples and the “safe harbor” were removed from the regs … thereby substantially escalating the difficulties U.S. corporations experienced in trying to understand, much less comply with, the law![24]

6) And last, but certainly not least, despite Congressional vows in 2002 that it would make it impossible for any U.S. company (such as TYC, Transocean (RIG), Cooper Industries (CBE), etc.) to ever again legally turn its back on U.S. taxes, by the time all of the lobbying was completed, the negotiations concluded, the amendments finalized, and the standard “pork barrel” projects added, the completed legislation left enough “wiggle room”[25] for Valeant Pharamaceuticals (VRX) (2010), (Aon (AON) (2012), Jazz Pharmaceuticals (JAZZ) (2012), Tower Group Int’l (TWGP) (2013), Actavis (ACT) (2013), Applied Materials (AMAT) (2014), MDT, ABBV, and many other companies[26] to legally drive their “Inversion” strategy through this legislative hole toward completion!!

Meanwhile, the big non-U.S. companies with whom these “newly-Inverted” U.S. companies must compete within the global economy for affordable capital, investors, market share, have been (for years now) reaping the benefit of being domiciled in nations with lower tax rates and more accommodating rules regarding repatriation of cash. Recall what Abbott (ABT) CEO, Miles White, said in an earlier article about “Tax Inversions”: “They make a lot of sense for a lot of companies. And I don’t think anyone needs to ‘apologize’ for making use of perfectly legal processes for shifting one’s corporate tax base.” He then went on to strongly advocate that Congress overhaul U.S. corporate tax law in a way that will ensure that “every company domiciled in the U.S. [will have a] level playing field in terms of access to capital overseas.” White is not alone regarding that conviction. Every CEO I have seen quoted on this issue has reiterated the same point – often phrasing her/his opinion even more strongly.

Before I wrap up this piece, I am certain that some of you are thinking: “How naïve can Petty be? These corporations are just greedy, ungrateful, money-grubbing manipulators that can’t be trusted! They’d run over management’s grandparents if they could make more money!”

I am among the first to acknowledge that the ranks of U.S. corporate management are replete with smooth talking, self-centered, less than scrupulous individuals[27]. A fitting example is the CEO of TYC at the time of the first well-known “Inversion” in 1997. His name was Dennis Kozlowski.

Would you buy a used car from this man? He is Dennis Kozlowski, the CEO of Tyco International (TYC) when it initiated an early “Tax Inversion” in 1997. He was later convicted (2005) of grand larceny and securities fraud and sent to jail for a long time (paroled at the end of 2013).

During his tenure at TYC during the heady days following its move to Bermuda, Kozlowski guided TYC into a virtual maze of organizational complexity – including launching more than 150 subsidiaries within the first two to three years following Inversion. One of the most intriguing (and most questionable) of the “Kozlowski approved” strategies was designating Tyco International Ltd. (based outside of the U.S.) as the “lender of choice” for all TYC subsidiaries! Can you guess why? Tyco International could find the lowest global interest rates, borrow those funds at a low rate, and then re-lend that money to subsidiaries as needed – at a higher rate certain to guarantee Tyco International a hefty profit. Obviously, the subsidiaries could deduct all interest paid as a business expense, thereby lowering taxable income. And Tyco International owed no U.S. income tax on its profits!! Now that’s a way to maximize net income!! But it was also questionable on ethical grounds, subjected the corporation to charges of tax evasion, and certainly bears the appearance of “double dealing”. However (thank heavens) Kozlowski is an exception within the ranks of U.S. CEOs… a fact publically established in 2005 when he was convicted of grand larceny, securities fraud and other charges. The detailed charges brought against him were quite jaw dropping; but in summary, Kozlowski stole $137 million from Tyco in unauthorized bonuses, abused company loan programs and sold more than $400 million in inflated stock.[28]

Therefore, if you will allow me to exclude the few Dennis Kozlowski-types from consideration on this issue, let’s try to assess the “Inversion” issue objectively.

What would you have done if you had been the CEO of MDT, ABBV, AON, ACAT, AMT, etc. and were presented with a legal way to significantly increase your company’s access to global funds, compete on a global level, and maximize shareholder value?[29]

Perhaps your opinion is: “I’d initiate an Inversion!” If so, consider the fact that Secretary Lew will be very cross with you!

If you are a U.S. Corporate CEO and initiate a "Tax Inversion", Jack Lew will be cross with you and call you "unpatriotic"!

Lew wants you to be an “economic patriot”. Does that sway your judgment at all?

If you are thinking: “But I don’t want to be a ‘deserter’… I don’t want to be thought of as ‘unpatriotic’!” Then imagine major stakeholders Carl Icahn and David Einhorn, who hold (between them) about 17% of your company stock (each just under the SEC-filing threshold), demanding a meeting with you later today in your office! When they arrive, they lecture you on “Corporate Fiduciary Duty”, which if I remember correctly makes no mention of being obligated to pay any government any income tax beyond the level that ensures compliance with existing corporate tax policy. That being said (they tell you), there is a compelling legal obligation shared by you and your board to maximize shareholder value while ensuring that the company’s accounting records comply with GAAP[30] and the daily operations are kept safe for employees, consumers, and the environment!!

What will you do?!!!

Yes, I know, I don’t pay you nearly enough to handle these real world corporate decisions!! I don’t disagree at all! But there is at least one benefit: I will never fire you!! And if you consider knowledge to be an asset – then another priceless benefit that I provide you is discovering facts and truths that you haven’t read anywhere else!

In our follow-up article, I will provide you with a small scale example of why and how “Inversion” has been a compelling corporate strategy for so many U.S. corporations, and I will provide you with data and charts that demonstrate the magnitude of the U.S. tax issue faced by countless U.S. global companies who have (despite U.S. corporate laws) thrived enough in the global marketplace to have multi-billions sitting idly in overseas accounts. Finally, I will provide you with real world observations from CFOs and national tax experts regarding why “Inversions” have seemingly reached epidemic proportions.

At the end I will offer my own opinion as to where true accountability for “Inversions” lies. I imagine most of you can already guess what my opinion will be!

INVESTOR TAKEAWAY:

I don’t think there is much doubt that companies that have successfully built a “brand” within the U.S. consumer market have received “blessing upon blessing” from being an active participant within that market. When you read that, I imagine you are thinking of corporate names such as Apple (AAPL), Google (GOOGL), Amazon (AMZN), Microsoft (MSFT), Intel (INTC), General Electric (GE), Proctor & Gamble (PG), Johnson & Johnson (JNJ), Abbott (ABT), Walmart (WMT), Medtronic (MDT), Walgreens (WAG), etc. Yes, those names have become trusted “icons” within the United States, and those firms should be eternally grateful.

If we were living back in the mid-19th century, when PG got its start (1860, in Cincinnati, as a supplier of soap and other supplies to the Union Army), the U.S. market would have been sufficient to fulfill a company’s vision and ambitions… and a country’s dream for optimum corporate development! However, the age of “national economic aspiration” is over, my friends! The era of Lew’s “economic patriotism” was at its peak during both World Wars…. when U.S. industrial might was totally focused upon winning a war overseas!

In today’s world, no nation can any longer afford to have an economic vision that is anything less than global. Unless the United States government (and its people) wants to continue burdening its global corporations (MNEs) with an unfair and unnecessary disadvantage with regard to full access to global capital and the freedom to maximize shareholder value, it needs to put politics aside[31] and perform a “special interest free”, full blown overhaul of U.S. corporate tax law. It needs to catch up with the rest of the “Developed World”… lower corporate rates[32], make it less egregiously burdensome to repatriate cash that has already been taxed overseas, and actually empower U.S. corporations to grow globally! If anyone in Washington is capable of thinking long-term, such policy will inevitability grow the U.S. economy and (eventually) tax revenue.

If instead, inertia and “Blarney Politics” continue to hold sway in Washington (absolutely no offense intended toward leaders in the Emerald Isle; I believe I have established my respect for them earlier!) what we will continue to see is more of the following:

Here is the logo for Volkswagen (VLKAY).

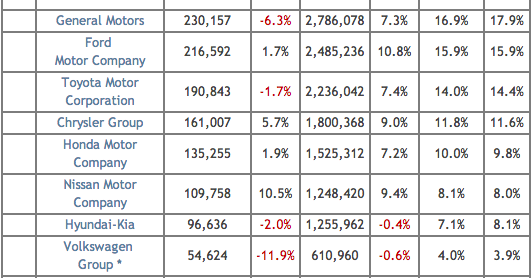

1) It was just announced that Volkswagen (VLKAY) (has surpassed General Motors (GM) in global auto sales—capturing 2nd Place (just behind Toyota Motor (TM)… and that despite an abysmal showing by VW in strictly US sales during 2013:

Note here how poorly VLKAY (Volkswagen) sales within the U.S. were in 2013... and yet (despite that) Volkswagen just surpassed GM to become the world's second biggest seller of autos!!

2) Swiss MNE firm Nestle (NSRGY) taking over Purina (founded in US in 1894)

3) Frigidaire (US-founded in 1918) taken over by Swedish Electrolux AB (ELUXY)

4) Anglo-Dutch MNE Unilever plc (UL) assuming control of Popsicle (a 1923 founded American “classic” product)

5) 7-Eleven (“O Thank Heaven for 7-Eleven!”) being taken over by a Japanese MNE.

6) UL buying out Hellmann’s condiments (including my sacred Hellmann’s Mayonaise!)

7) In the biggest “hurt” of all…. Brazilian-Belgian company A-B InBev (BUD)[33] purchased a veritable U.S. institution…. the “King of Beer”… the steward of the “Clydesdale Horses”… practically ripping the heart out of Mid America… when it bought Anheuser-Busch Companies, Inc. (for $52 billion).

Trust me, friends, I bear no ill will toward any of these buy-outs. I am a realistic. What these examples powerfully illustrate is that our economy is no longer “our grandfather’s economy”… or even “our father’s economy”. Instead it is a truly global economy, and becoming more interconnected all the time! Washington must fully awaken to that reality!

In fact, my friends, here is a thought for our leaders in Washington to consider:

Since “junkets” are a perennial favorite of members in Congress, send every last one of them to Ireland to learn first hand why and how Ireland has been luring a disproportionate number of U.S. firms to domicile there. Just make sure that not one single one of those Congressional politicians is allowed anywhere near Blarney Castle! Congress has already demonstrated an excessive natural gift of “Blarney”… no member of Congress needs any more of it![34]

At any rate, learning from other nations actually successful in luring companies to its shores will surely be more productive than what is currently going on in the offices and conference rooms (and press briefing rooms) of Washington – ie. blaming U.S. corporations; throwing around accusations of “unpatriotic behavior”; and trying like mad to hide the “truth” behind IRS Section 7874 (Washington’s failed effort to “solve” the problem in 2002!).

DISCLOSURE: The author does currently own options on ABBV. He has traded (in the past) MDT, as well as a plethora of other stocks mentioned above. The author celebrates that he never owned TYC and always suspect Kozlowski was a jerk. Nothing in this article is intended as a recommendation to buy or sell anything. Always consult with your financial advisor regarding changes in your portfolio – either subtractions or additions.

FOR MORE DETAILS:

“Escaping the U.S. Tax System: From Corporate Inversions to Re-Domiciling”

by Stuart Webber (a college professor)

http://corit-academic.org/wp-content/uploads/2011/12/Escaping-the-U.S.-Tax-System-Webber.pdf

FOOTNOTES:

[1] Of course, the less grateful among you have suggested that I am an extremely stingy employer… and/or that I don’t pay you enough to make the responsibility of being a CEO worth your while. But key readers (and my fearless editor) have indicated that as long as I don’t “fire” them from continuing to be a reader, they’ll be happy to “stay on”!! Thank you, faithful readers!

[2] Including, I might add, one of my adult children.

[3] I grew up watching Miss Chiquita and listening to her sing her song … one I can still vividly recall decades later!

Here is a streaming video of the song: https://www.youtube.com/watch?v=RFDOI24RRAE

(To all of you who are too young to have enjoyed the original version –

“eat your heart out!”

And of course, just as you’d expect, when Alessandra Ambrosio learned that I carry a soft spot in my heart for Miss Chiquita, she just had to post this image on social media:

This is a social media posting by Ms. Ambrosia, impersonating "Miss Chiquita".

[4] Here is an explanation from the 1997 Wall Street Journal: “Under terms of the transaction, Tyco would combine with a unit of ADT; the ADT parent would rename itself Tyco International Ltd. For each of their shares, Tyco shareholders would receive one share in the new company, while ADT holders would receive 0.48133 share of the new company. The new Tyco would be headed by current Tyco Chief Executive Dennis Kozlowski and continue to be headquartered in Exeter, N.H., while its board would be controlled by Tyco's current directors.” I note that the then ADT Chairman, Sir Michael Ashcroft, ended up with a cozy seat on the Tyco board!

[5] Note for the record that, since its start, COV has been managed from its HQ in Mansfield, Massachusetts!

[6] A year proven to be a vintage year for “births”!!

[7] FYFFF’s brand is the oldest fruit brand in the world!!

[8] Because Ireland has the Eurozone’s lowest corporate rate, officials in Ireland are not the object of great favor among “high-tax” European leaders!

[9] Jan-June 2013: 14.8 billion Euros vs Jan-June 2014: 97.4 billion Euros (since we are “Dollar-centric”… 97.4 billion Euros equal $132.8 billion!)

[10] An adaptation of the old Smith Barney commercial tagline (spoken by actor icon, John Houseman!).

John Houseman was one of the most distinctive actors and spokesmen of his day! He is still remembered for playing "Professor Kingsfield" ("Paperchase") and handiling commercials for Smith-Barney!

[11] Unlike nations that are more enlightened on corporate tax policy (such as the United Kingdom and Canada, that only tax corporate income earned within that country!) the U.S. taxes “worldwide income” reported by U.S. incorporated firms).

[12] It is not impossible, but definitely very challenging, to find a country that does NOT have a lower corporate tax rate than in the U.S.! (The U.S. has the highest rate among developed countries!).

[13] Calling to mind, of course, Corporal Bowe Bergdahl (now Sgt. Bergdahl) – whose parents the President invited to (and celebrated at) the White House. The President has not yet invited executives from MDT or ABBV to the White House.

[14] He finished his thought by adding: “It’s wrong.”

[15] With all due respect to the President, no company can go to any developed country without paying taxes. What they will be doing is (eventually) paying lower taxes!

[16] Liberals were outraged in June when the Supreme Court overturned a Montana law that prohibited corporate contributions to a political campaign, suggesting that for some purposes, a corporation is like a person. Perhaps the President felt that the Court needed for him to offer the benefit of his personal support for that stance… despite the fact that I know of absolutely no federal class, ceremony, or oath through which a corporation can officially be declared “a citizen”!

[17] With all due respect to Secretary Lew, as I recall a few of the root causes for the American Revolutionary War, I recall avid opposition to “government” interfering with the free and legal exercise by (what would be now) U.S. based firms of profitable trade here and overseas. I believe Thomas Jefferson, John Adams, Patrick Henry, etc. would have called that “economic patriotism”.

[18] I believe that CEOs around the country would love for Lew to give them a list of all the countries with “near zero” rates!

[19] The most recent comprehensive reform was almost 30 years ago. Surely a need for “reform” should have been recognized long before 2014!

[20] I’m not sure the Wall Street Journal, Barrons, CNBC, Bloomberg, Fox Business News, or any other competent, informed authority has sensed that business-tax-reform process has been “moving steadily forward”.

[21] It should be no surprise to any of us that no one in Congress has accepted responsibility for that legislative failure from 12 years ago. “Accountability” is not to be found in D.C…. if the finger must be pointed at Congress!

[22] Highest within the “Developed World”.

[23] It is worth noting that EBay (EBAY) recently repatriated about $9 billion, on which it paid approximately $3.3 billion in U.S. income tax. If YOU were a shareholder, would you think that was an effective strategy to maximize shareholder value?!

[24] Folks, I assure you that I am not making this stuff up!

[25] Call them “loopholes”, “exceptions”, “exclusions”, or whatever you prefer

[26] Over 40 U.S. companies have “Inverted” since TYC in 1997, with 15 of these occurring since January of 2012!

[27] Some of them qualifying as “scoundrels”.

[28] While in prison, Kozlowski offered this explanation to the parole board: “I was living in a CEO-type bubble. I had a strong sense of entitlement at that time … and I stole a lot of money.”

[29] Keep in mind that the CEO (Greg Wasson) at Walgreens (WAG) has been under fire in recent months for not sooner (and more smoothly) locked up an “Inversion” with Alliance-Boots. Just this week (the same week it had indicated an announcement about the Boots deal) it replaced its CFO/Executive Vice President – hardly something a major company would do at such a crucial time unless there were serious underlying issues at play! Obviously major WAG shareholders expect (read that “demand”) an Inversion!

[30] And Sarbanes-Oxley

[31] Yes, I know. That will happen when (proverbially) “Hell freezes over!”

[32] At least to a less prohibitive level!

[33] Adding insult to injury, InBev stole the classic stock symbol: BUD J

[34] Take a minute to watch this 1949 video about Blarney and the famed “Blarney Stone”! http://www.britishpathe.com/video/blarney-stone/query/blarney+castle Remember that 1949 was a very good year!

Related Posts

Should You Buy Tractor Supply Stock Right Now?

Should You Buy Tractor Supply Stock Right Now?

Also on Market Tamer…

Follow Us on Facebook